Personal Wealth Management / Market Analysis

Happy Birthday, QE

What has five years of quantitative easing accomplished?

Five years ago, on Black Friday 2008, quantitative easing (QE) was born. In its quest to battle the deflationary effects of the financial panic, the Fed launched the "extraordinary" policy of buying long-term assets from banks. In exchange, the Fed credited banks' reserve accounts, believing the banks would lend off these reserves many times over-a big money supply increase to boost growth.

To date, through multiple rounds of (now infinite) QE, the monetary base (M0) has swelled by nearly $3 trillion. Yet this economic expansion has been the slowest in post-war history.

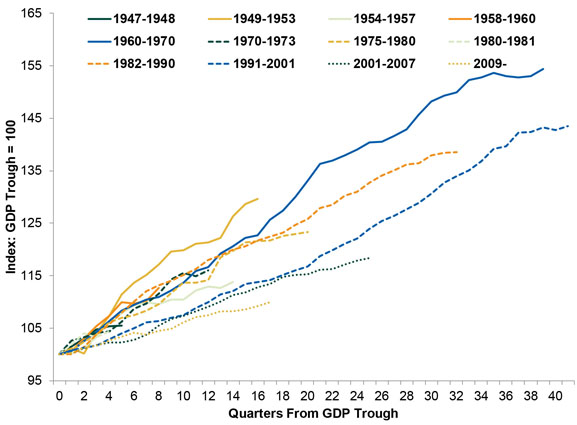

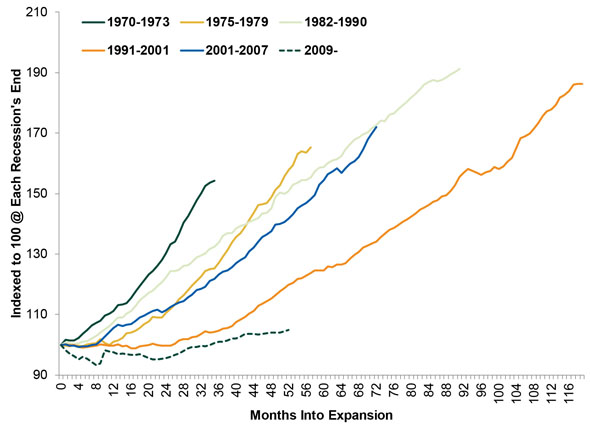

Exhibit 1: Cumulative GDP Growth

Source: Federal Reserve Bank of St. Louis, as of 11/27/2013.

Granted, falling government spending has been a drag. But even excluding government spending, this expansion's growth rate is in the bottom three.

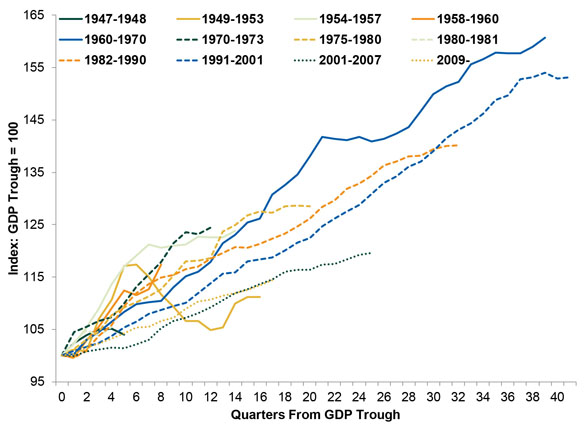

Exhibit 2: Cumulative Growth in GDP ex-Government

Source: Federal Reserve Bank of St. Louis, as of 11/27/2013.

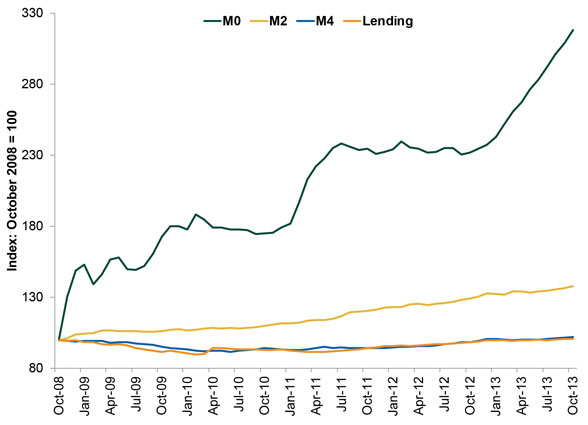

So what's the real culprit? Slow money supply growth! As shown in Exhibit 3, while M0 is over 200% higher today than when QE began, broader measures of money haven't grown at nearly the same rate. M2, the Fed's preferred gauge, has grown only 37%. The broadest measure, M4 (calculated by the Center for Financial Stability), has grown less than 3% and spent a year and a half in contraction. Loan growth, too, has been anemic.

Exhibit 3: US Monetary Aggregates and Loan Growth Since QE Began

Source: Federal Reserve Bank of St. Louis and Center for Financial Stability, as of 11/27/2013.

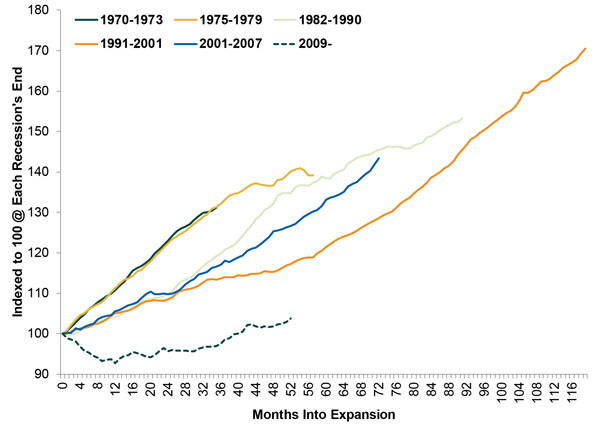

This isn't the norm. As shown in Exhibits 4 and 5, this is the weakest loan and M4 growth of any expansion since 1970 (since M4 data are available).

Exhibit 4: Cumulative M4 Growth

Source: Center for Financial Stability, US National Bureau of Economic Research, as of 11/27/2013.

Exhibit 5: Cumulative Loan Growth

Source: Federal Reserve Bank of St. Louis and US National Bureau of Economic Research, as of 11/27/2013.

M2 growth is more in the middle of the pack, but M2 isn't the best reflection of all capital circulating throughout the real economy. As the Center for Financial Stability Explains: "Narrow aggregates, such as M1 and M2, give no weight to many highly liquid substitutes for money. That truncation is hard to justify." M2 includes only currency, checkable deposits, household savings deposits, small time deposits and money market funds. M4 includes all these plus all other highly liquid instruments that substitute for money: institutional money market funds, large time deposits, repurchase agreements, commercial paper and Treasury bills. Together, M4 and lending give us the best view of how much money is really being put to work.

This expansion's lending data are a bit skewed by an accounting rule change, which caused the abrupt increase between months 9 and 10. SFAS Rules 166 and 167 essentially required banks to move off-balance sheet loans onto their balance sheets. Even including this change, loan growth during the previous six expansions outpaced current loan growth by a significant margin-and this loan growth comes off a pretty low base.

M4 and loan growth are anemic because of QE. As your friendly MarketMinder staff have written here, here, here and here, by buying long-term assets from banks, the Fed has reduced long-term interest rates. Short-term rates are fixed near zero, so the spread between the two has shrunk. This is a problem for banks, whose core business is borrowing at short-term rates and lending at long-term rates-the spread is their potential operating profit. They depend on it as compensation for the risk of making a new loan. When the spread is small, they lend less and create less money, robbing the economy of its fuel.

In this environment, banks have incentive to lend to only the most creditworthy. Iffier borrowers-small businesses, entrepreneurs, firms with below investment-grade ratings and consumers without gold-plated credit ratings-get shut out. That robs a big swath of the economy of the capital it needs to invest and grow. Hence why QE celebrates its fifth birthday with many lackluster economic returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today