Personal Wealth Management / Economics

The Bizarro World of QE Taper Fears

As folks realize their QE tapering fears are false, their relief should propel stocks higher.

Like this bunny at the Rommerz Rabbit Hopping Competition, the US economy and stock markets should clear the hurdle of QE tapering. Photo by Ralph Orlowski/Getty Images.

This week, solidly expansionary US economic data have been met with a thud. Why, you ask? Headlines warn the data increases the likelihood of the Fed’s dreaded quantitative easing (QE) taper. Yes, in this bizzaro world, lower unemployment and higher output aren’t positive—they’re bad because they presume the Fed is yanking away the punchbowl too soon. While this thesis may or may not explain recent volatility, it’s crucial to recall nearly anything can cause near-term market wiggles. But those wiggles aren’t necessarily indicative of the future. In our view, tapering is a likely positive for the economy—and when investors realize this, their false QE reduction fears turn into bullish sentiment—providing a boost for stocks.

First, let’s step back and look at the recent data underpinning the taper talk:

- Jobless claims declined to the lowest level since 2007—dropping by 15,000 to a total of 320,000 during the week ending August 10.

- CPI increased by 0.2% from June to July—matching estimates.

- Intermodal rail freight shipments rose 4% in the four weeks ending August 10.

- New home construction rose nearly 6% in July.

- While industrial output was flat last month, retail sales rose 0.2%—the fourth straight monthly increase.

The first two—jobless claims and inflation data—comprise components of the Fed’s stated “key QE taper” criteria, which seems to have led to all these bizarre positive-is-negative headlines.

So, why are overly positive data interpreted as such negatives for markets? We have asked the same question for months. It really all boils down to a misunderstanding about what QE has and hasn’t done. Many fear slowing QE will reduce the money supply and remove liquidity from markets. We think the data suggest otherwise.

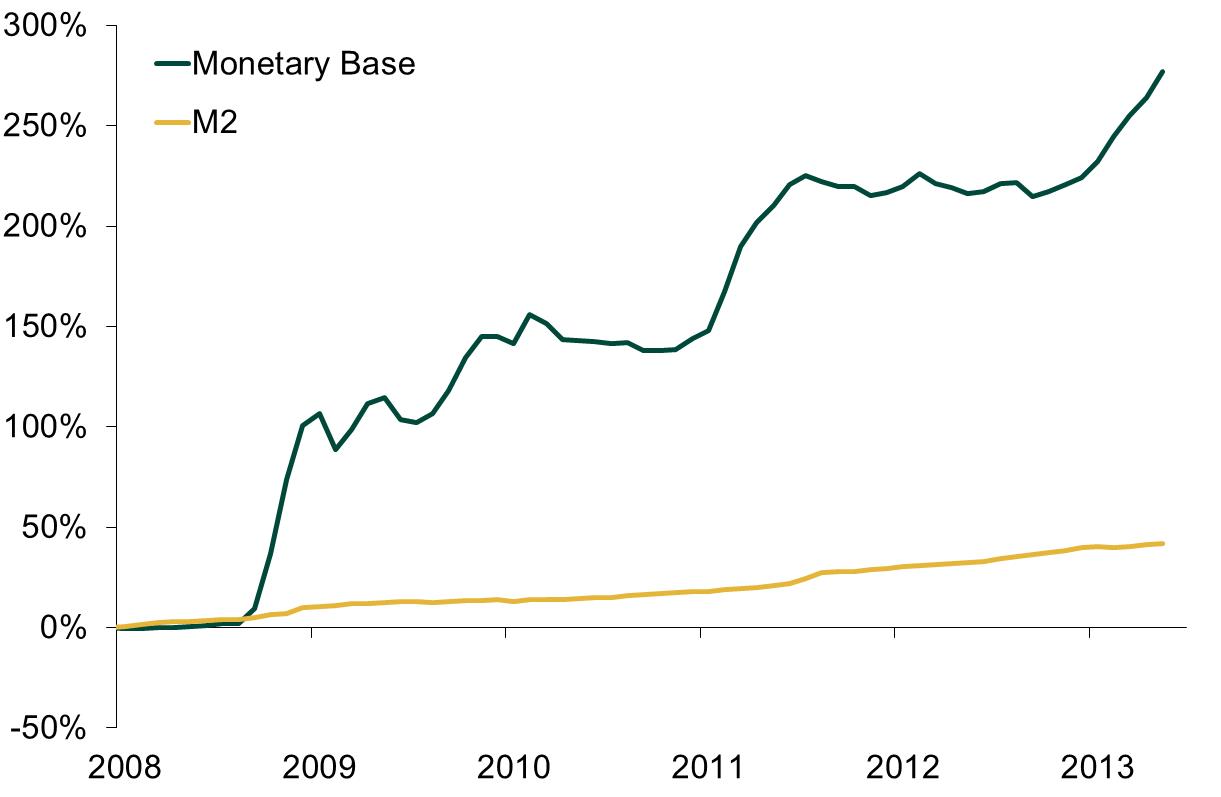

For starters, QE’s real effects haven’t been on the broader US or global economy. There is, in fact, no punchbowl for the Fed to yank. While the Fed has purchased long-term securities (Treasurys and mortgage-backed bonds) at a rate of $85 billion a month, the money has largely accumulated on banks’ balance sheets instead of being lent out. (Exhibit 1) The Fed can boost the monetary base all they want (which they do when they buy bonds with QE). But ultimately banks have to lend before the money supply grows (M2, which reflects the amount of money circulating throughout the economy).

Exhibit 1: Cumulative Monetary Base Vs. Money Supply Growth

Source: Thomson Reuters, US Federal Reserve as of 7/2/2013. M2 Money Supply and Monetary Base from 12/15/2007-5/15/2013.

So what might make banks lend more? A return to more normal monetary policy and a steeper yield curve. The yield curve is the gap between short-term (think: Fed funds) rates and long-term rates like mortgages, car loans and business loans. Banks benefit from a steeper curve because the difference between their major funding sources (short rates) and loans they extend (long rates) is bigger. That boosts profitability—creating an incentive for banks to lend. The aforementioned Fed bond buying depresses long rates—discouraging lending.

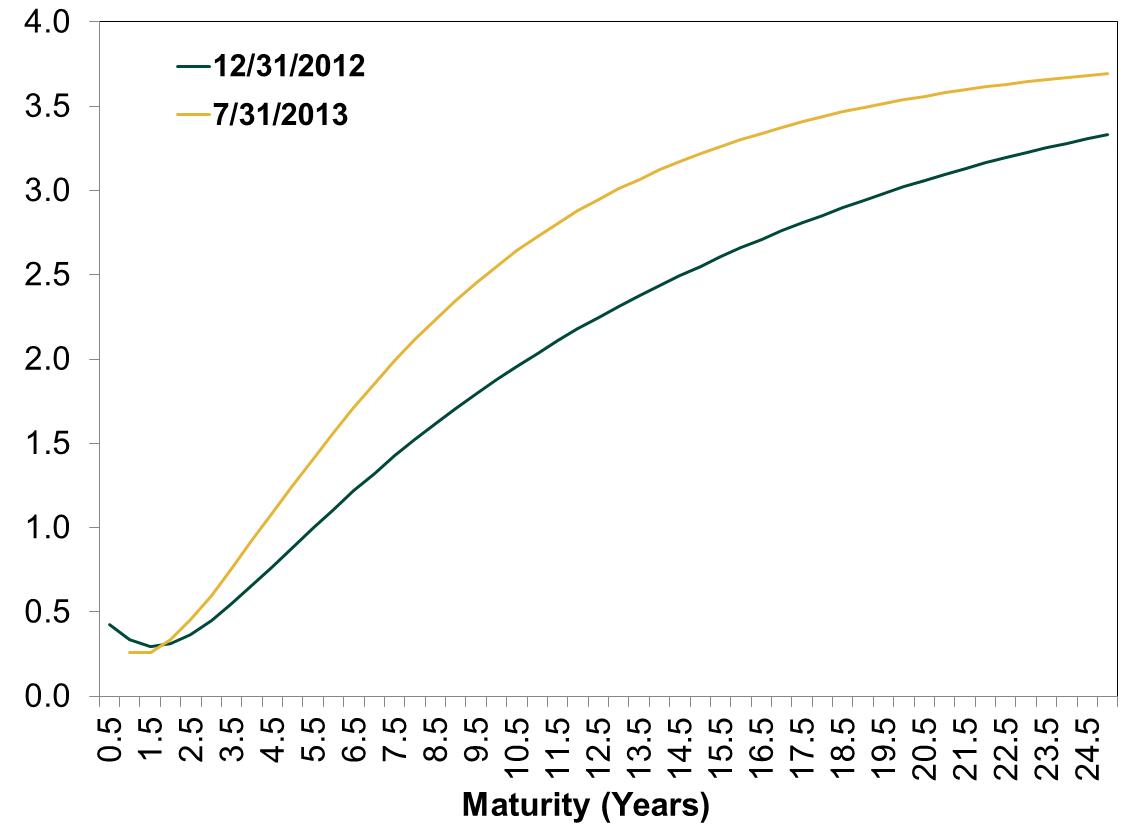

One prime example can be gleaned from across the pond. The UK put an end to its asset purchase program in November 2012. Since then the UK’s government yield curve has steepened, as shown in Exhibit 2, and most economic indicators have accelerated.

Exhibit 2: UK Yield Curve Steepening

Source: Bank of England, as of 7/31/2013.UK government yield curves as of 12/31/2012 and 7/31/2013.

While some market participants fret over the end of QE, we remain bullish. We believe the bigger QE-related economic surprise is it could stimulate growth. And as folks gradually realize their fears were false—as they’ve done with the sequester and fiscal cliff before the taper—their increasing relief and bullishness likely propel stocks higher.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today