Personal Wealth Management / Market Analysis

Household Debt: In Depth

Americans are borrowing more than ever-but that doesn't mean another financial crisis looms.

Nearly a decade after the Financial Crisis's onset, many pundits accuse American consumers of amnesia-forgetting 2008's lessons and once again racking up excessive debt. A New York Fed report released last week showed US household debt reached $12.8 trillion in Q2-above Q4 2008's record of $12.7 trillion. But despite widespread warnings about Americans' forgetfulness, there is nothing troubling about US household debt now. In our view, household debt isn't at problematic levels today-and it didn't cause 2008 anyway.

Let's start by putting household debt in context. Without it, record highs mean nothing-and with it, today's worries don't stand up to scrutiny. Mortgage debt balances-the vast majority of household debt-remain below their Q3 2008 peak and aren't in the limelight right now. Recent fears center on auto loans, credit cards and student debt. Let's consider each in turn.

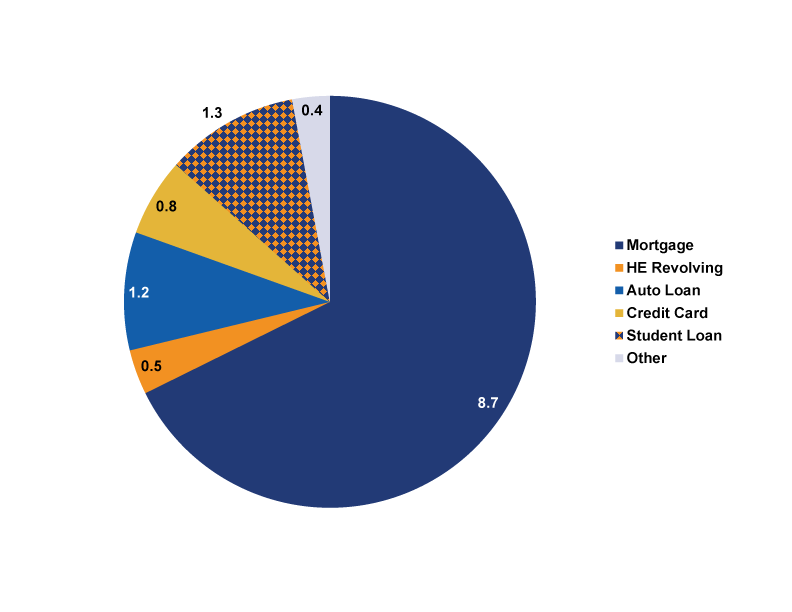

Exhibit 1: Q2 2017 US Household Debt Breakdown, in Trillions of Dollars

Source: Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit for Q2 2017, as of 8/18/2017.

Student Loans

While folks often lament impoverished graduates shackled by six-figure loan balances rendering them unable to buy a house, raise a family or afford the occasional avocado toast, in our view, such worries are a bit overwrought. Roughly two-thirds of borrowers owe $25,000 or less. Heavy borrowers with debts of at least $100,000-largely those with the highest education level-make up just 30% of student debt. Not coincidentally, higher-balance loans have lower delinquency rates than small-balance loans, which implies investing in extra education may be worth it. Besides, over 90% of issuance comes from the Federal Government-banks have little exposure. A 2008 redux stemming from student debt seems beyond unlikely.

Auto Loans

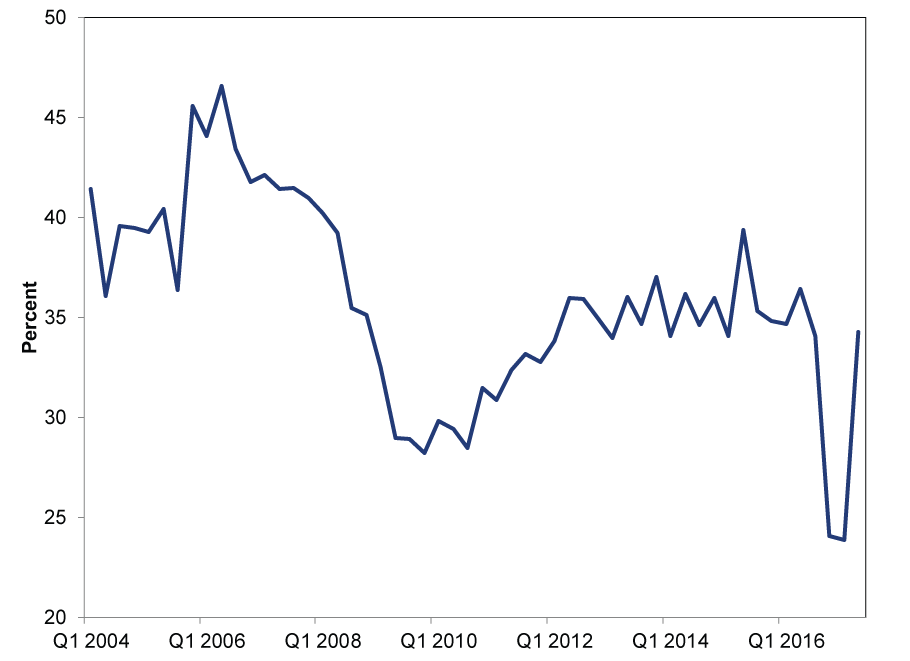

Fears over rising auto loans have their own misperceived 2008 tie-in. Many point to "subprime" auto loans, reminding investors of low-quality mortgage fears commonplace in 2008. But subprime auto loans aren't surging. As Exhibit 2 shows, they make up 34% of the total-a level they have bounced around for years. In addition, subprime auto loans are only about 3% of overall household debt[i]-tiny!

Exhibit 2: Subprime Share of Auto Loan Originations

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax, as of 8/18/2017. Subprime auto loans as a percentage of all auto loan originations, Q1 2004 - Q2 2017. Auto Loan Originations by Credit Score, Q1 2004 - Q2 2017. *Credit Score is Equifax Riskscore 3.0

There is another crucial difference between cars and houses-the former depreciates near instantly. While we think it is off target to argue the housing bubble caused 2008 (more on that shortly), if you buy that, you'll readily see why this theory makes little sense. The housing bubble mentality hinged on folks (and, to an extent, banks) taking big risks on the notion home prices would rise ad infinitum. That logic makes zero sense as applied to car loans. No one expects their new car to gain value when they resell it. Housing bubble comparisons are off.

Credit Cards

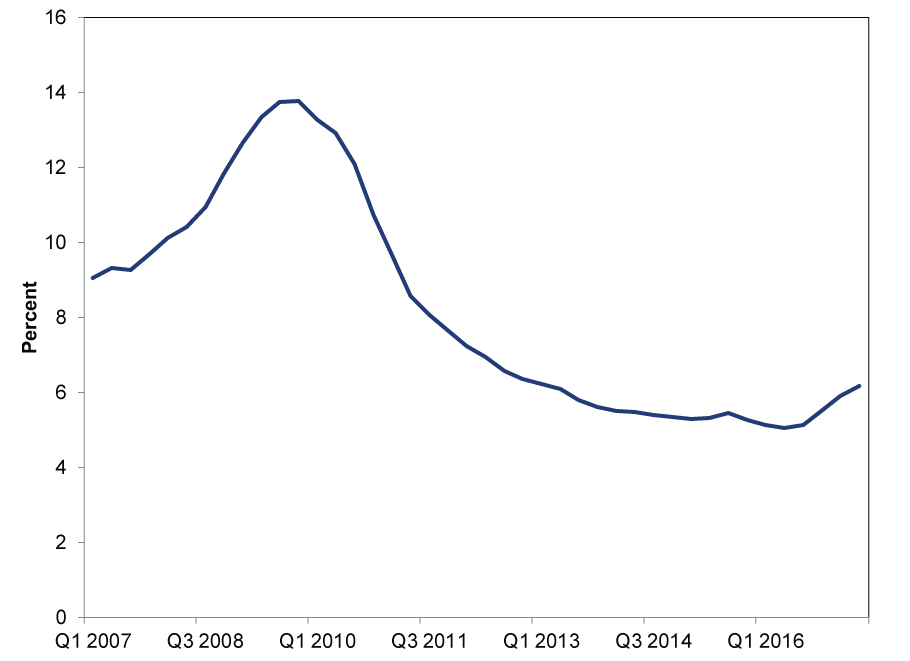

Credit cards caused jitters after balances ticked up to their highest levels since 2009 and, of those, about 6.2% of balances were 30-days delinquent, up from 5.1% a year ago.[ii] But both remain far below the record highs of a decade ago, suggesting consumers aren't overextended.

Exhibit 3: 30-Day Credit Card Delinquencies

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax, as of 8/18/2017. 30-day credit card delinquency rate, Q1 2007 - Q2 2017.

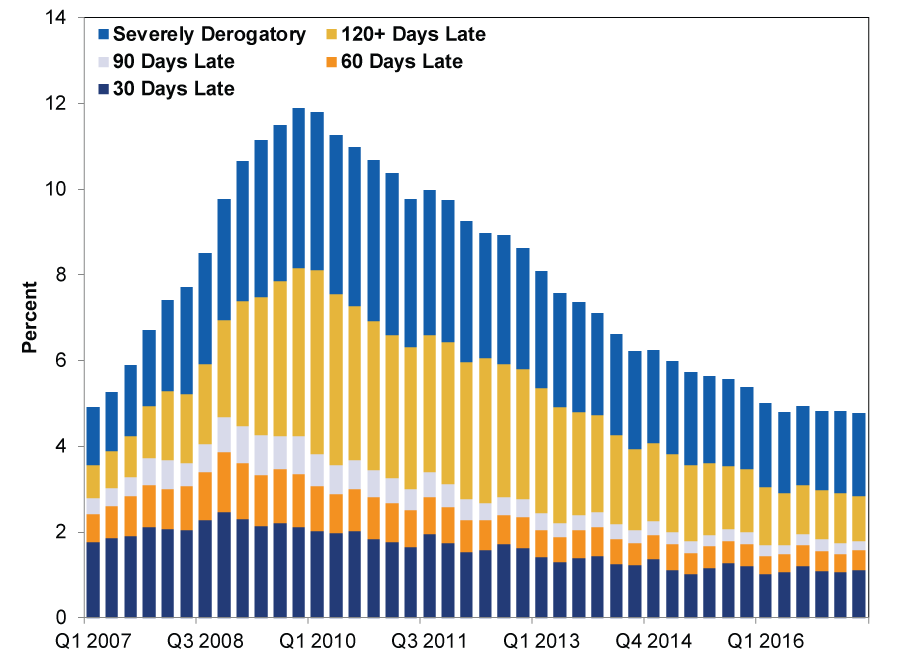

Low delinquency rates aren't unique to credit cards: Across all categories, delinquency rates are sub-5%-far below levels seen in the wake of 2008.

Exhibit 4: Household Debt Delinquency Rates

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax, as of 8/18/2018. Delinquent household debt as a percentage of total household debt, by delinquency status, Q1 2007 - Q2 2017.

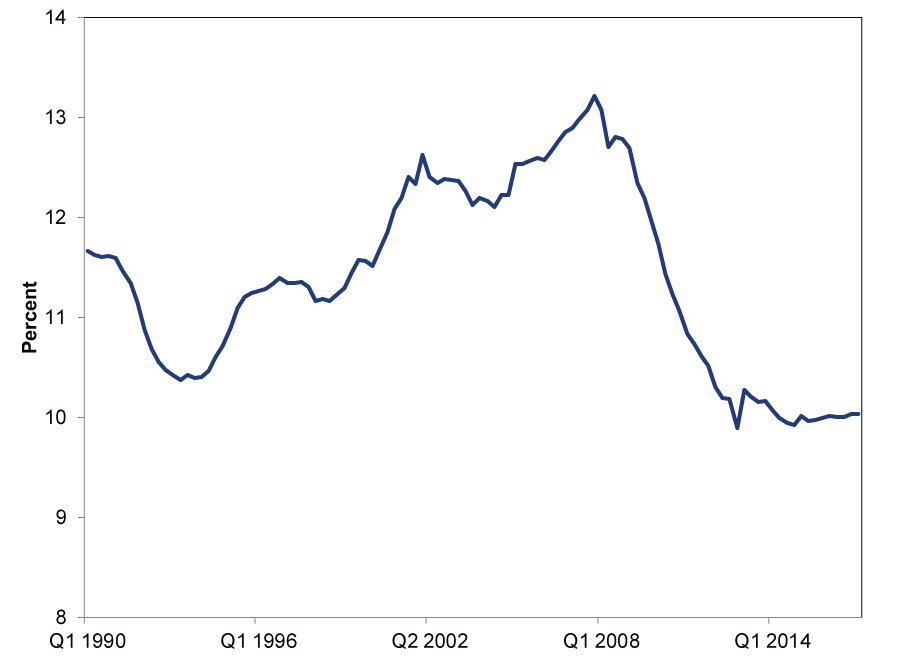

But those are all pieces. If we look at the bigger picture, there are further reasons not to fear high household debt. For one, that $12.8 trillion, record-high number isn't adjusted for population or economic growth. The greater the national wealth (and probably population), the more people can borrow in total-and overall and on average, America is getting wealthier. US households net worth keeps notching new highs-nearly doubling since the recession's end. Disposable personal income is rising as well, reaching $14.4 trillion in June. As a result, it's no surprise debt service as a percentage of disposable income is near multi-decade lows. (Exhibit 5) While we aren't suggesting consumers go on a debt-fueled spending binge, it is hard to see present levels of debt-service payments as problematic.

Exhibit 5: Household Debt Service Payments Quite Manageable

Source: Federal Reserve Bank of St. Louis, as of 8/18/2017. Household debt service payments as a percentage of disposable income, Q1 1990 - Q1 2017.

So the facts on the ground suggest we aren't near 2008-era levels. But even then, household debt wasn't behind 2008's crash. For many, 2008 evokes images of overleveraged banks foreclosing on strapped families' underwater homes. That's part of the story-and a key to understanding sentiment wasn't euphoric in 2007. However, it doesn't come close to fully explaining the downturn. Consumer spending held up far better than other major GDP components like net trade and business investment-as it typically does in recessions. Most consumption is on services and necessities-relatively stable.

Hence, although housing began collapsing before the bear market[iii] and subprime lending dominated headlines throughout, coincidence isn't causation. In our view, the real culprit was FAS 157, a well-intended but disastrous accounting rule that forced banks to value illiquid securitized mortgages at market prices. Because these illiquid assets had no market, every fire sale by a cash-strapped bank or hedge fund set a new reference price-requiring banks to mark similar assets to it en masse, in turn forcing sales to raise capital. Coupled with the government's haphazard response, this negativity escalated into a full-fledged panic. When the dust cleared, trillions in unneeded balance sheet writedowns had crippled lenders. This despite the fact subsequent developments have proven the offending assets weren't as toxic as widely presumed.

Today, no such rule threatens illiquid bank loans-undermining 2008 redux warnings. Still, all the popular narratives about 2008 lead to heavy coverage of anything debt- and bank-related. While it is possible the next bear begins in Financials, we'd suggest the hyper-focus likely means it will be elsewhere. Investors have a strong tendency to fight the last war-and debt fixation may be characteristic of that now.

[i] Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax, as of 8/18/2017. Subprime auto loans as a percentage of all household debt, as of Q2 2017.

[ii] Though credit card balances are up, they remain 9.5% below Q4 2008's peak-a point curiously omitted from the media coverage we linked to.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today