Personal Wealth Management / Market Analysis

The Wealth After-Effect

All-time-high household net worth doesn't mean much for stocks.

Rising Leading Economic Index. Positive yield curve. Swift loan growth. Broad money supply growth. Widespread new business growth in manufacturing and services. Those are but a few reasons we think America's economic outlook is bright. Here is something we deliberately left off that list: All-time-high-and-rising household net worth, which the Fed just revealed hit another high in Q4. For years, pundits have argued rising net worth creates a "wealth effect," driving consumer spending (and economic growth) higher. Fun as this would be, it's sheer myth-not a reason to be bullish today (or fret a Fed rate hike).

For those who don't pore over financial blogs daily, the wealth effect theory goes like this: Rising household net worth (HNW) makes folks spend more-partly because they "feel" richer, partly because they tap their homes and stock investments as ATMs. Now, if you've ever owned a home, you are probably scratching your head, because you likely didn't track your home's value real-time and plan trips to the mall based on its alleged appreciation.[i] Instead, you likely weighed your disposable income against all your expenses, including your mortgage. Plus, data overwhelmingly show feelings don't drive spending. If they did, consumer spending would track consumer sentiment surveys-up when folks say they're feeling sunny, and vice versa. But people often say they feel one way and do the opposite.

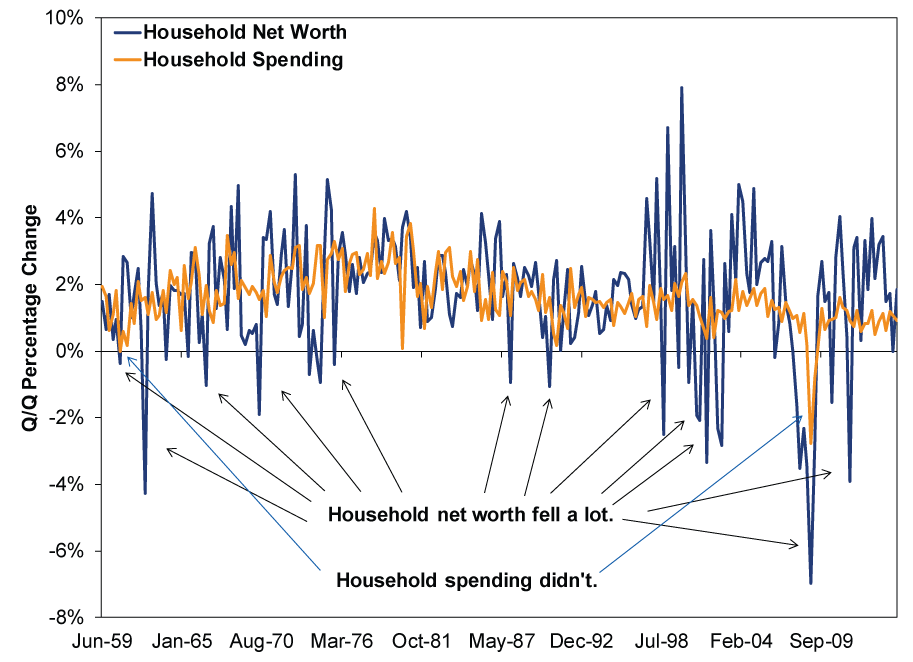

History doesn't support wealth-effect theory, either. HNW has dropped plenty without a corresponding drop in consumer spending. In the last downturn, HNW peaked a year before spending did. Folks spent that year buying more even though, according to the theory, they would have felt poorer.

Exhibit 1: Household Net Worth and Consumer Spending

Source: FactSet, as of 3/16/2015. Household Net Worth and Real Household Consumption (in 2009 USD), quarterly percentage change, Q2 1959 - Q4 2014.

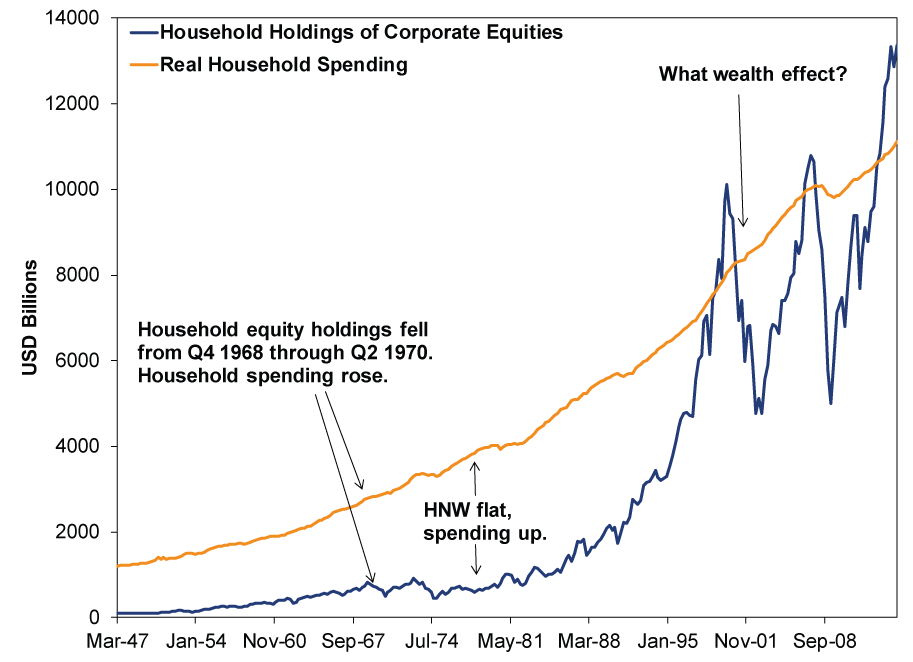

The most often-cited components don't much track spending, either. Like HNW, the value of household equity investments (ex. mutual funds[ii]) often falls without household spending going down the tubes. Both fell in the last downturn, but the timing doesn't sync-this simply shows markets tend to lead overall economic activity, of which consumer spending is a hefty chunk.

Exhibit 2: Household Equity Holdings and Consumer Spending

Source: FactSet, as of 3/16/2015. Household Corporate Equity Holdings and Real Household Consumption (in 2009 USD), quarterly percentage change, Q1 1947 - Q4 2014.

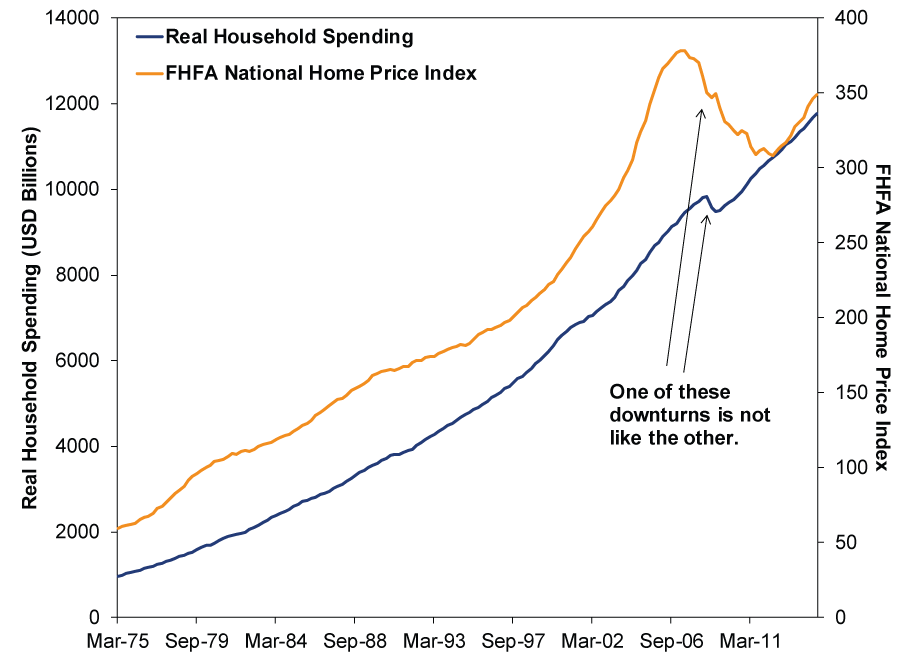

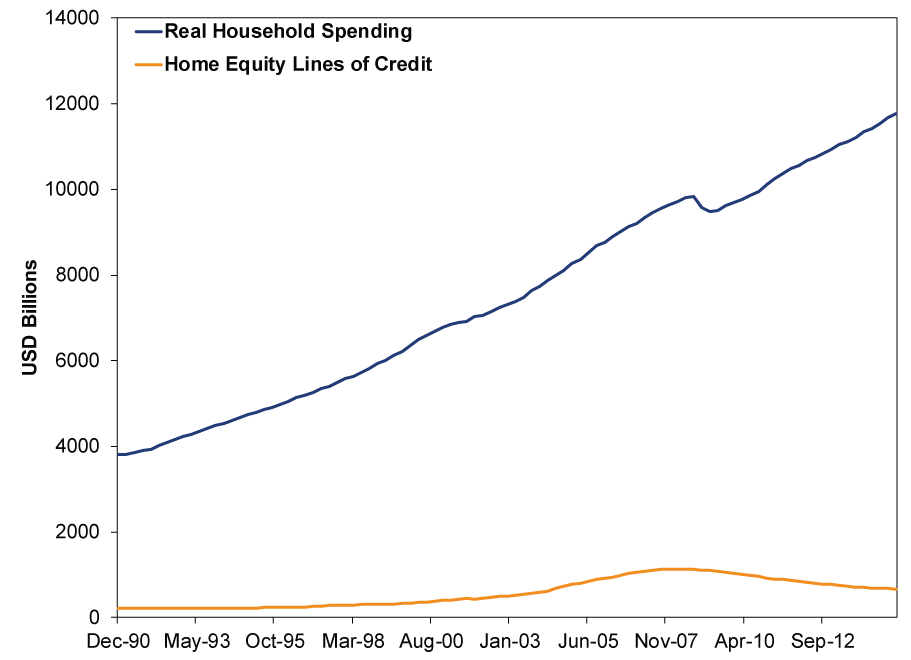

As for real estate, home prices peaked over a year before spending did in 2007/2008-and bottomed three years after spending did (Exhibit 3). Plus, unless you sell, using your home as an ATM generally requires a home equity loan. Those have dropped steadily since 2008, while spending keeps clocking new highs (Exhibit 4). Home equity loans are often credited for the 2002-2007 bull market's spending boom, but we are fairly sure the roughly $500 billion rise in home equity loans doesn't explain the roughly $2.5 trillion rise in household spending. Home renovations, sure, but home-related expenses are about 20% of total spending. Ours is not an HGTV economy.

Exhibit 3: Home Prices and Consumer Spending

Source: FactSet, as of 3/16/2015. FHFA Quarterly Home Price Index and Real Household Consumption (in 2009 USD), Q1 1975 - Q4 2014.

Exhibit 4: Home Equity Loans and Consumer Spending

Source: FactSet, as of 3/16/2015. Home Equity Loans outstanding and Real Household Consumption (in 2009 USD), Q4 1990 - Q4 2014.

The rising wealth is an after-effect, not a leading indicator-a function of rising markets and a growing economy. The wealth effect theory seeks causality where none exists, overthinking coincidence. Now, there are no absolutes here-people who live off their savings often do fund spending with stock investments. This is why retirement accounts exist! But the wealth effect theory overstates how much these individuals alter spending as the market cycle moves. Many do cut discretionary spending during downturns, but that's a slice of the total. Essential spending is much harder to cut, for retired and working folks alike. Hence why total consumer spending wobbles less during recessions than most believe. On the flipside, retired folks' discretionary spending might rise some during a bull, but many keep a longer perspective, knowing bull markets don't last forever (and always wary of the risk of outliving their savings). Plus, economic expansions aren't made or broken by people taking vacations and eating out.

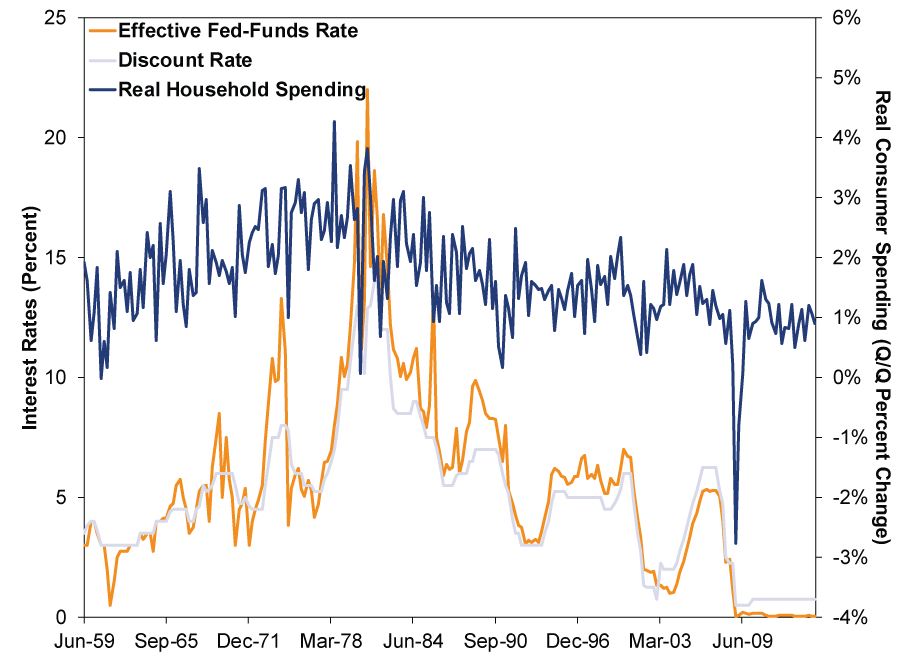

That all might sound sad if you've enjoyed reading how rising HNW is über bullish, and we don't want to rain on your parade-this is actually good news! It means corresponding fears a Fed rate hike will kill consumer spending are off-target. Some claim high interest rates sink stocks and home prices, creating a "negative wealth effect," but if the wealth effect is fake, the argument implodes. Heck, higher interest rates boost bank deposit rates-last we checked, this makes bank accounts a tad bigger, technically promoting spending. But don't take our word for it: As Exhibit 5 shows, strong (and weak) consumer spending growth has accompanied high and low rates.

Exhibit 5: Consumer Spending and Interest Rates

Source: FactSet and Federal Reserve Bank of St. Louis, as of 3/16/2015. Discount and Effective Fed-Funds Rates and quarterly percentage change in Real Household Consumption, Q2 1959 - Q4 2014. Until the early 1990s, the discount rate was the Fed's primary policy rate.

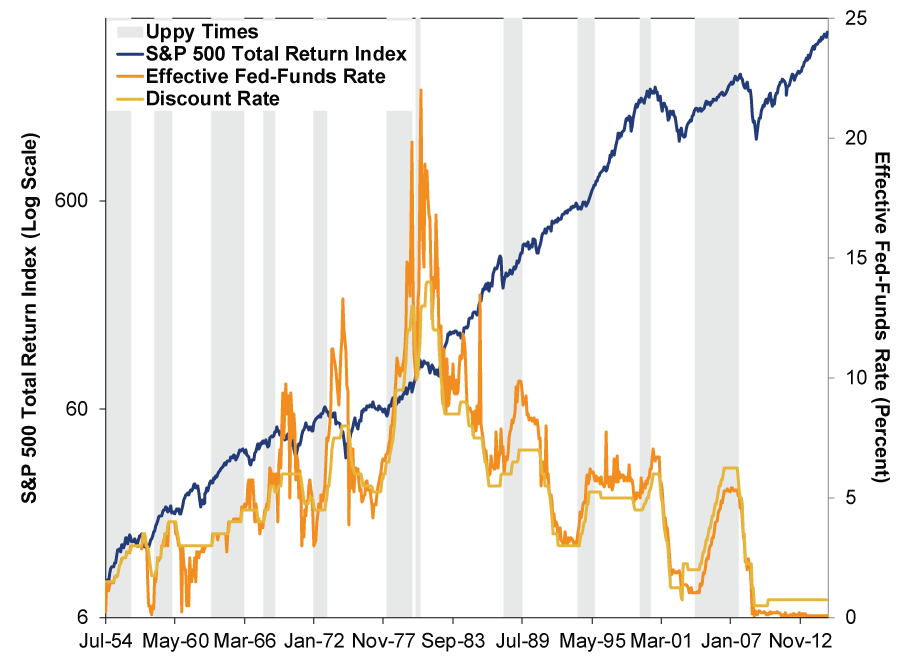

Also! As we wrote here, here and here, rising rates don't sink stocks. Ours is a rare viewpoint today, with reports alleging a link repeated across the Internet, but there is little history of the first rate hike in a tightening cycle ending a bull. Stocks have risen for long stretches alongside rising rates.

Exhibit 6: Searching for Meaning in Bouncy Rates

Source: Source: Global Financial Data, FactSet and Federal Reserve Bank of St. Louis, as of 3/16/2015. Discount and Effective Fed-Funds Rates and S&P 500 Total Return Index, July 1954 - February 2015.

Rising HNW is a fun fact, but nothing more. Not a reason to be bullish or bearish today-just what you get with years of rising stocks, home prices and overall growth.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Alleged being the keyword. We get that online real estate sites offer real-time home prices, but really, this is their guesstimate at best-they apply averages to the most recent sale price and can't account for any remodeling you might have done. We guess you could track regional price-per-square foot and apply that to your own home, but again, home improvements have an influence here. And anyway, a home is an illiquid asset.

[ii] The Fed doesn't break out equity/fixed income/blended mutual funds, so including them would skew this. Hence the exclusion.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today