Personal Wealth Management / Market Analysis

The Early Bird Scares the Worm

New Fed Head Janet Yellen has the whole media crowing about when the next Fed Funds rate hike will be—will her announcement ruffle markets’ feathers, too?

Janet Yellen led her first Fed meeting as Chair March 19 and, according to many, promptly laid an egg. As expected, she reduced quantitative easing (QE) asset purchases some more—from $65 billion to $55 billion a month. No surprise there. But she also vaguely hinted the Fed will hike interest rates “a considerable time” after QE ends—when pressed for specifics, she chirped, “about six months or that type of thing.” And thus, Fed Funds rate hike fears were hatched: Is the Fed giving markets enough information? Correct information? Has it lost touch with the economy? When will the hike happen? Will it cause a correction ... or worse? In our view, folks’ first question should actually be: When rate hike cycles begin, how have stocks reacted? The answer: They tend not to derail bull markets. For investors, all other questions about the Fed should check back to that.

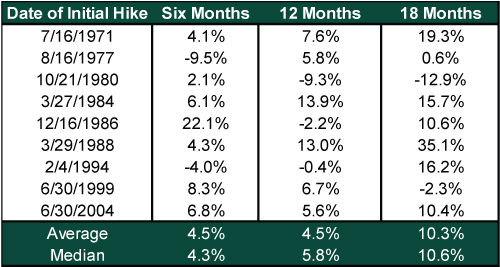

Many cling to the theory loose monetary policy—i.e., lower rates—is good for the economy because it boosts liquidity. Positive for stocks, too! And if that’s true, many assume the opposite—rising rates—must be bad, and knowing when exactly the hike will happen gives us a chance to brace for economic and market malaise before it sets in. But history tells a different story: Rate hikes aren’t inherently bad. Just consider the 6-, 12- and 18-month returns after the last several Fed Funds hikes, shown in Exhibit 1.

Exhibit 1: S&P 500 Returns After Fed Funds Rate Hikes

Source: Federal Reserve, Factset, as of 12/31/2013.

Stock returns are overwhelmingly positive! We’d see very different data if rising rates were an automatic negative. Of course, this doesn’t mean a rate hike is necessarily good for stocks, either. It just shows stocks are up much more often than they’re down, even after a rate hike cycle starts.

Still, since the press conference, everyone is trying to peg down when rates will rise. Some are worried it will happen too soon. Or not soon enough. Or it’ll definitely come next spring. A few even scolded Yellen for taking away their rate-hike measuring stick, having abandoned the unemployment rate as the key metric in her “forward guidance” for policy. (Not a foolish move in our eyes: Creating false expectations with one faulty data point is just bird-brained.) With all of these conflicting projections, how are investors to know when the hike will happen?

What matters more than the date is whether it’s an appropriate move when it happens. No monetary policy is inherently good or evil, and hiking the Fed Funds rate is no exception. Consider QE: When it began in 2008, QE seemed like a fine policy aiming to loosen liquidity for an economy in crisis. But the crisis ended early 2009, and QE kept going well after things recovered and low liquidity wasn’t an issue. It went on so long, QE flattened the yield curve and eventually became tight monetary policy—disincentivizing bank lending since a flat yield curve weighs on loan profitability. As a result, we’ve seen slow money supply growth—tight money—a factor we believe is a drag on economic activity. In our view, it’s a testament to their underlying strength that the bull market and economic expansion have taken flight despite contractionary policy.

But with hikes likely a year away or more—or less, but not anytime soon—handicapping what will happen when and if a rate hike comes is folly. And all this assumes the Fed even sticks with their squawking ... jawboning ... errr ... forward guidance. They might pull something else out of their nest if conditions don’t warrant a hike six months after QE expires. Rate hikes are a tool the Fed uses to dampen inflation, and they usually wait to see sign of it. To date, inflationary pressures are largely absent. The likelihood they spot-on forecast a time when inflation ticks up gives the Fed way too much credit for their historical accuracy—after all, this is a flock still twittering that QE is stimulus, despite ample evidence to the contrary. Many things can impact inflation, but a timeline, no matter how rough or specific, is largely moot. Talk is cheap, and Fed jawboning is equally inexpensive. There is nothing about changing the name of Fedspeak from jawboning to forward guidance that causes its importance to inflate. Actions and the economic environment matter more.

So, difficult as it sounds, try to block out the heated debate over when the hike will happen. That doesn’t mean ignore the Fed—it’s entirely possible what they do down the road may not match what they say today, and that’s always worth keeping an eye on. But knowing rising rates aren’t necessarily a headwind for markets likely puts you ahead of most other investors who are too skeptical to appreciate the fact this bull market should keep marching on. It makes those Fed hike fears easier to swallow.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today