Personal Wealth Management / Economics

Will Rising Rates Ding Demand?

Will rising long-term interest rates choke the US economy?

Will rising long-term interest rates spell the end of the US’s economic expansion?

Many folks fear they will—that credit demand will dry up without ultra-low borrowing costs. Yet interest rates have risen irregularly over the past year-plus, and lending is up! In our view, this is no coincidence. Evidence has long suggested higher long-term rates boost credit supply without equivalently docking demand (if at all), and in our view, this seems the most likely scenario moving forward. As quantitative easing (QE) winds down and long-term rates rise further, lending should pick up and give the economy a highly unexpected tailwind.

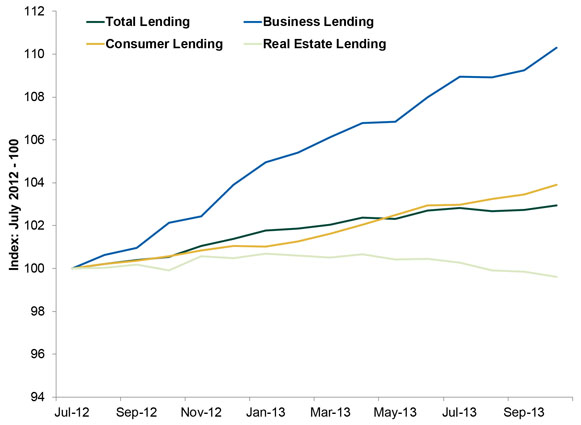

Consider: US 10-year Treasury rates reached their low in July 2012, touching 1.53% at month’s end. At October 2013’s close, they were up to 2.63%. Over this period, business lending is up 10.3%, consumer lending is up 3.9% and real estate lending is down about -0.4%—adding up to a 2.9% rise in total lending. (Exhibit 1) This isn’t a robust increase, but it’s hardly the freefall most expected.

Exhibit 1: US Lending by Category

Source: Federal Reserve Bank of St. Louis, Federal Reserve Board of Governors, as of 11/18/2013.

This isn’t terribly surprising—higher long-term rates have caused the US’s rate spread to widen, which has historically fueled higher loan growth. As we’ve written in more detail here and here, since banks’ core business is borrowing from depositors at short rates and lending at higher long rates, the spread between the two represents their potential operating profit. QE flattened the spread, shrinking the supply of credit. Banks aren’t in the non-profit business. To stay alive and provide value to shareholders, they need compensation for risk taken. When potential profits are slim, banks have incentive to lend to only the most creditworthy borrowers. When profits are higher, banks are typically comfortable taking more risk, which opens credit to swaths of borrowers who were shut out at lower rates. Rising spreads mean higher credit availability—a supply increase.

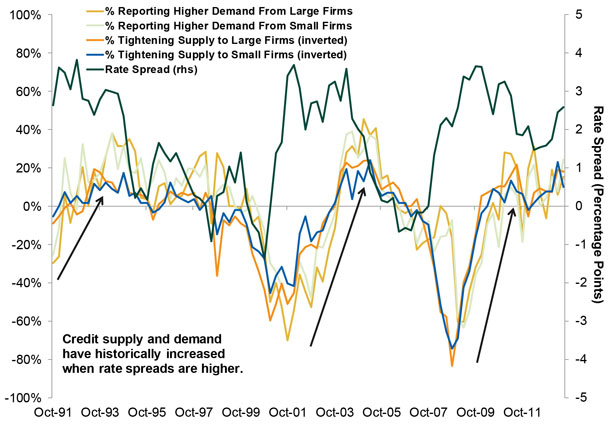

Since the Fed’s Senior Loan Officer Opinion Survey (SLOOS) started tracking small- and large-business credit trends in 1991, wider yield spreads have corresponded with higher credit supply and higher demand. To measure supply, SLOOS tracks the percentage of banks tightening standards—tighter standards mean shrinking supply. Theinverse of this line, therefore, shows banks’ eagerness to lend—loan supply. Exhibit 2 shows this for small and large firms, the percentage of banks reporting higher demand and the rate spread (10-yr US Treasurys minus Fed Funds—the same spread used in LEI).

Exhibit 2: US Rate Spread and Credit Supply & Demand

Source: Federal Reserve Bank of St. Louis, Federal Reserve Senior Loan Officer Opinion Survey, as of 11/18/2013.

To most readers, this probably seems counter-intuitive—shouldn’t businesses be less apt to borrow at higher rates? Isn’t this why the Fed has spent the past five years reducing borrowing costs?

To answer this, pretend you’re a business owner with good credit standing, which means you can borrow at about 5%—or 3% post tax. Your return on investment is about 7%. If your borrowing costs rise half a percentage point, your margin is still 50%. If rates rise a full point, your potential profit is still over 40%—a bit less, but still well worth pursuing. For most businesses, this mentality reigns—the long-term profit potential of a sound business plan can easily weather a small increase in borrowing costs. If a plan can’t weather an incremental rate hike, it probably wasn’t worth pursuing in the first place.

The latest borrowing data from the US and Japan illustrate this well. In the US, total household debt—mortgages, credit cards, student loans and auto loans—rose for the first time this year in Q3. Yes, interest rates are up. But so are incomes, net worth, employment and other factors that might impact a person’s eagerness to take on a new loan. Japan, by contrast, has seen the opposite. Borrowing costs are ultra low, but borrowers aren’t eager—anecdotally, business owners say they lack confidence in the recovery’s long-term prospects, and they aren’t comfortable taking on a long-term obligation for now. Japan’s borrowing costs are lower than the US’s, but because our economy is in better fundamental shape, our firms and households are readier to borrow.

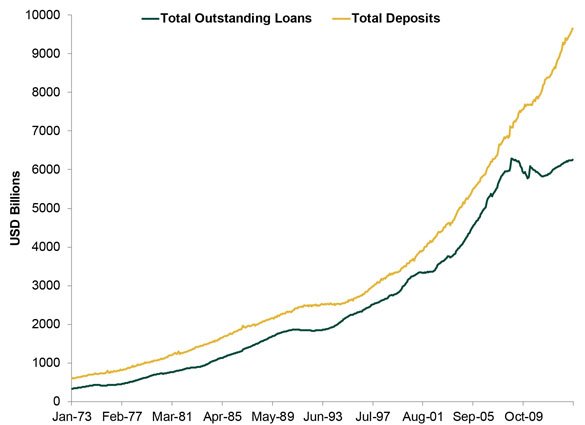

Looking ahead, higher loan growth could be a powerful economic tailwind. Total lending has been anemic since 2008, and it has plenty of room to catch up. As shown in Exhibit 3, since the Fed started publishing this data in 1973 and until October 2008, total bank loans and deposits largely tracked each other. Then, in November 2008—coincidentally, when QE began—a divergence formed.

Exhibit 3: Total Outstanding US Loans and Deposits

Source: St. Louis Federal Reserve, Federal Reserve Board of Governors, as of 11/18/2013.

If loan growth simply matched the rate of deposit growth again, money supply growth would get closer to the expansionary norm. Businesses would have more capital for growth-oriented endeavors. The rising tide of investment would lift the entire country.

Since few expect this outcome, it would be a massive surprise for stocks. As we often write, false fears are typically bullish, and the biggest, most backward fears tend to give stocks the most oomph over time. Most folks see QE’s eventual end backward, fearing higher rates when they should cheer instead. In our view, this is a big reason this bull should have plenty of room to run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today