Personal Wealth Management / Economics

One Weird—and Simple—Trick to Thinking Differently About Stocks

Identifying false fears might sound weird, but it’s a handy way for investors to gauge the market’s future direction.

Shoppers enjoy a grand day out. Photo by Jeff J. Mitchell/Getty Images.

Retail sales rose for the fourth straight month in August—hooray! But they also slowed to 0.2%, missing expectations and prompting the usual round of slow-growth fears. In our view, this is one more sign investors underappreciate the US economy’s underlying strength—bullish for stocks.

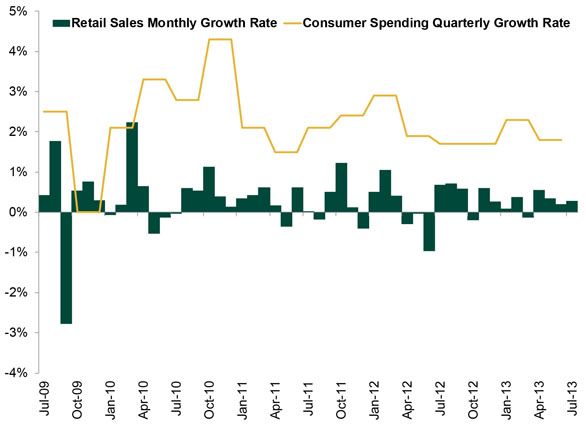

Retail sales can be a handy near-immediate indicator of whether consumers are spending or not—they’re reported soon after the preceding month, while total consumer spending is reported one month after quarter-end. However, monthly results don’t necessarily predict total consumer spending, which includes a host of services not captured in the retail figures. Exhibit 1 overlays quarterly consumer spending growth (seasonally adjusted annual rate) on monthly retail sales growth since this expansion began—there isn’t a discernible relationship. Retail sales were positive all of Q4 2009, but consumer spending was flat. Retail sales were ho-hum in Q2 2010, yet consumer spending topped 3%. Both grew fine in Q1 2012. No pattern—just coincidence.

Exhibit 1: Retail Sales and Consumer Spending

Source: St. Louis Federal Reserve, Bureau of Economic Analysis, as of 9/13/2013.

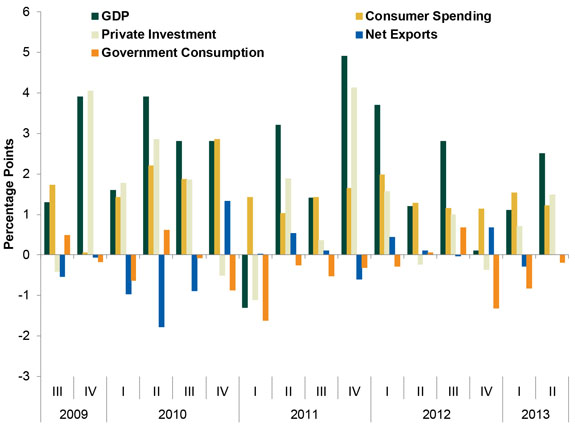

Then again, the heightened focus on consumer spending seems a touch unwarranted. Sure, it’s about 70% of GDP, but it isn’t the sole or even biggest determinant of growth—most consumer spending tends to be pretty stable stuff. Private investment is pretty darned important—and quite volatile. So important, GDP’s two worst quarters of this expansion happened when it fell. Consumer spending, meanwhile, was positive—the broader economy doesn’t always move in the same direction as consumers. (Exhibit 2)

Exhibit 2: Quarterly GDP Growth and Contributions

Source: Bureau of Economic Analysis, as of 9/13/2013.

So investors today needn’t automatically fret slowing growth just because retail sales slowed. But they do!

This isn’t the only false fear alive today. China jitters persist, QE taper terror reigns supreme and rising bond yields still give investors the willies. So does recently slower earnings growth. On all fronts, though, reality should beat. China, though slowing some, is moving further and further away from the dreaded hard landing—2013’s growth target appears within reach, which would keep China’s total dollar contribution to global GDP high. As we explain further here, the Fed’s quantitative easing is contractionary—it flattens the yield spread, making lending less profitable and sapping bank incentive to lend, which makes money supply grow at an anemic rate. Pulling the Fed’s proverbial punchbowl won’t end the party—it’ll get things started! The wider yield spread should boost lending, giving firms more investment capital. That augurs well for earnings, too—which, by the way, grew just fine in less cyclical sectors in Q2, with revenues growing as well. And as for interest rates, well, decades of data show rising rates aren’t inherently bad for stocks. Rates have risen—and fallen—during periods of rising stocks. And periods of falling stocks. Many other fundamentals besides rates influence stocks—today, those fundamentals are overwhelmingly positive.

Overall, expectations are just too dour, in our view—false fears are abundant. That means the potential for happy surprises is high. Markets like happy surprises—over time, they tend to force investors to adjust their bets as their perception of reality improves. The more folks rationally recognize the strength around them, the more confidence they gain in companies’ future profitability, and the more they’re typically willing to pay for those future earnings. The more false fears exist today, the greater the potential for shifting sentiment to lift prices looking ahead. Just one more (perhaps weird) reason this bull market has room to run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today