Personal Wealth Management /

How Investors Should Think About Recently Placid Stocks

Volatility isn’t gone forever. Despite our expectation for a good year, investors should prepare now for its eventual return.

While last year’s fund outflows and sour sentiment surveys suggest many investors may have missed it, stocks had just the kind of 2019 most investors would love. Not only was the S&P 500 up a whopping 31.5% (gains stocks have added to this year thus far), the ride was pretty smooth, too.[i] Neither US nor global stocks have had a 1% up or down day since mid-October—a roughly 3-month stretch of relatively placid markets. Even financial news headlines seem fairly sanguine of late, touting real or alleged positives like the US/China “phase one” trade deal signing, accommodative monetary policy and the prospect of rebounding corporate earnings this year.[ii] Our advice to investors: While sunnier sentiment seems rational, you should expect more chop ahead. In our view, this is a good time to remember market turbulence will eventually return—and mentally prepare for it.

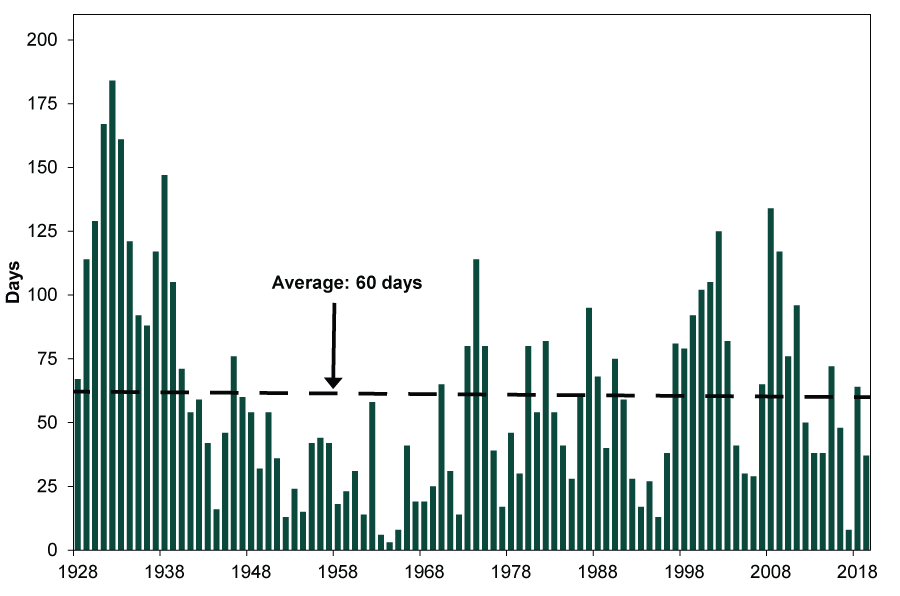

As investing jargon, “volatility” typically refers either to big daily market moves or short-term pullbacks. Both forms come and go without warning and are normal in bull markets. The reason: In the short term, sentiment heavily influences stocks—and it can shift rapidly, for any or no reason. One way to see this is by tallying the days US stocks close up or down more than 1% in a given year. Exhibit 1 shows this, using the S&P 500 for its long history of daily index data.

Exhibit 1: Daily S&P 500 Moves of Greater Than 1% in Either Direction, Annual Total

Source: FactSet, as of 1/22/2020. S&P 500, number of daily price moves exceeding 1% (absolute value), 1/3/1928 – 12/31/2019.

Higher-volatility years are common in bulls and don’t necessarily coincide with negativity. For example, in this bull market, S&P 500 daily volatility exceeded the historical average in 2009, 2010, 2011, 2015 and 2018. Notably, 2009 began with stocks in a bear market (which ended March 9), and the latter four years contained corrections (short, sharp, sentiment-driven moves exceeding -10%). Corrections are a common source of big daily moves as stocks dip sharply and rebound about as fast. Yet, to varying degrees, stocks rose in each year but 2018. The lesson, in our view: Conflating volatile periods with bad times to own stocks is a mistake, as volatility can be up or down.

As for quiet periods—multi-month stretches of 1% or smaller daily moves—these last until they don’t. Investors don’t get advance warning of their ending, and their end says nothing about what movement follows. Some low-volatility periods end with a bang. The two three-month long quiet stretches that ended in January and October 2018 both represented the start of corrections. While neither represented a bear market, they did see a prolonged bout of increased short-term volatility. Others, though, end with little fanfare. For example, after a near-three month low-volatility stretch ended on March 1, 2017, the S&P 500 gained 12.8% through yearend.[iii] Only 4 of the 218 trading days in this span saw stocks swing more than 1%.

Pullbacks, too, strike at random. While not every stock market dip reaches correction territory, studying corrections gives a sense of volatility’s unpredictable timing. US stocks have experienced six corrections in this bull market. The gaps between them have varied from as many as 746 trading days to as few as 125.[iv] Corrections don’t operate on schedules, and one is never “due.”

Since volatility is inevitable even in overall rising markets, we think investors needn’t fear its return. But this can be easier said than done. It is a natural human tendency to extrapolate the recent past into the future. Consistent gains and small daily moves may start to seem normal, making it hard to remember how volatility feels. In our view, this raises the risk of overreaction once a period of bigger swings returns. For example, we wouldn’t be shocked if campaign trail chatter spurred some volatility in the coming months—like last May, when Medicare for All proposals briefly jolted markets. We aren’t saying a correction is assured—again, they aren’t predictable—but we wouldn’t rule it (or bigger daily moves) out, either.

In our view, mentally preparing now can help reduce volatility’s sting. To help you do so, here are a few questions we think investors should ask when markets inevitably gyrate and headlines trumpet dire warnings.

- Does the dip stem from huge, previously unnoticed fundamental dangers? Or are stocks merely rehashing old fears?

- Are headlines fretting something that is actually benign or lacks the size and scope to derail the global expansion?

- If the feared developments are indeed substantial and negative, are they likely to occur or just a possibility?

In our view, these questions can help you rationally assess market jitters and avoid succumbing to their emotional pull.

Finally, focus on your long-term goals. If they require holding stocks, a bout of volatility doesn’t change this. Enduring bigger swings can be trying. But reacting to them can be disastrous, as it might mean missing out on substantial gains afterwards. So whenever volatility strikes again, start by accepting it as a normal part of bull markets—it doesn’t necessarily signal a landmark shift.

[i] Source: FactSet, as of 1/23/2020. S&P 500 Index total return, 12/31/2018 – 12/31/2019.

[ii] Aside from rising earnings, we don’t think these are positive fundamental drivers. But since many investors see them as such, they likely contribute to warming sentiment.

[iii] Source: FactSet, as of 1/22/2020. S&P 500 Index total return, 3/1/2017 – 12/31/2017.

[iv] Ibid., as of 1/24/2020. S&P 500 Price Index, 6/1/2012 – 5/21/2015 and 10/3/2011 – 4/2/2012.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today