Personal Wealth Management / Market Analysis

Inside the Global Energy Price Spike

Prices also signal ramping supply—and substitution—we are starting to see.

In the energy crunch heard ’round the world, households and businesses reliant on oil and gas are scrambling, driving headline fear from the UK to China as oil hits a seven-year high. Pundits warn the shortages and price spikes will hurt households, raise businesses’ costs and compound global supply-chain dysfunction as factories slash output. We don’t doubt many will feel a pinch, yet we also think a little perspective is in order. While it may take time to iron out production wrinkles and shortages, in the 3 to 30 month timeframe we believe forward-looking markets evaluate, the winter fuel “chaos” pundits hype isn’t likely to tank global growth—or stocks.

What is behind the global energy crunch? Regional factors. As we wrote last Tuesday, China implicitly banned Australian coal imports over a geopolitical spat, while it has also been trying to cut its coal dependence generally. Last year, China became the world’s largest liquid natural gas (LNG) importer, and its appetite has only grown since. But switching to gas-fired electrical generation hasn’t been smooth. China’s government caps electricity prices, so utilities can’t pass their rising costs to consumers. Spiking wholesale power prices force them to operate at a loss, so many cut output, sparking blackouts.

In the UK and much of Europe, weak wind power generation has also driven up demand for gas, which smaller utilities struggled to manage, leading to outages. Adding to the crunch: low reserves, as Russian gas export curbs have depleted inventories to decade-low levels. Dutch near-term gas futures, the European benchmark, quintupled to a record-high €100 per megawatt hour last Thursday from €20 in April.[i] This is having knock-on effects globally. In the US, natural gas prices more than doubled from $2.43 per million British thermal units in April to $5.94.[ii] Except for intermittent spikes associated with brief supply disruptions, like this February’s winter cold snap that literally froze natural gas production amid surging demand, prices are at their highest in more than a decade.

In response to gas shortages, utilities globally are ramping up oil-fired power plants where they can, driving demand for crude higher. Brent oil prices jumped from $65 a barrel in August to $83 today, flirting with new highs last seen before crude’s late-2014 collapse.[iii] There is also the UK’s gasoline shortage, which is more accurately a shortage of truck drivers, but the result—panic buying and gas lines—is the same, and it triggered a sentiment plunge.

With global energy prices spiking, analysts warn of demand destruction and factory closures, while some economists suggest stagflation akin to the 1970s’ energy shocks awaits. Many pundits suggest this could cause markets to crash. Take a step back, though, and let us put such dire prognostications in context.

Efforts to alleviate energy shortages: From a high level, prices are a signal for production, consumption and distribution. Global markets function as a coordinating mechanism to direct resources where needed, allowing households and businesses to adapt. It isn’t immediate, as this year’s port backups and supply-chain issues attest. But markets are usually pretty efficient at organizing global production—and longer-term growth.

In the meantime, it seems producers and consumers are starting to respond to the higher prices. While Russia’s gas flows to Europe have reportedly dwindled along some pipelines—through Poland and Ukraine—alarming many, they seem to be picking up in pipelines through Turkey and Hungary. Some think Russia is rerouting supplies to pressure German authorities into opening the just-completed Nord Stream 2 pipeline running from Russia to Germany under the Baltic Sea, which could double gas flows to Europe.

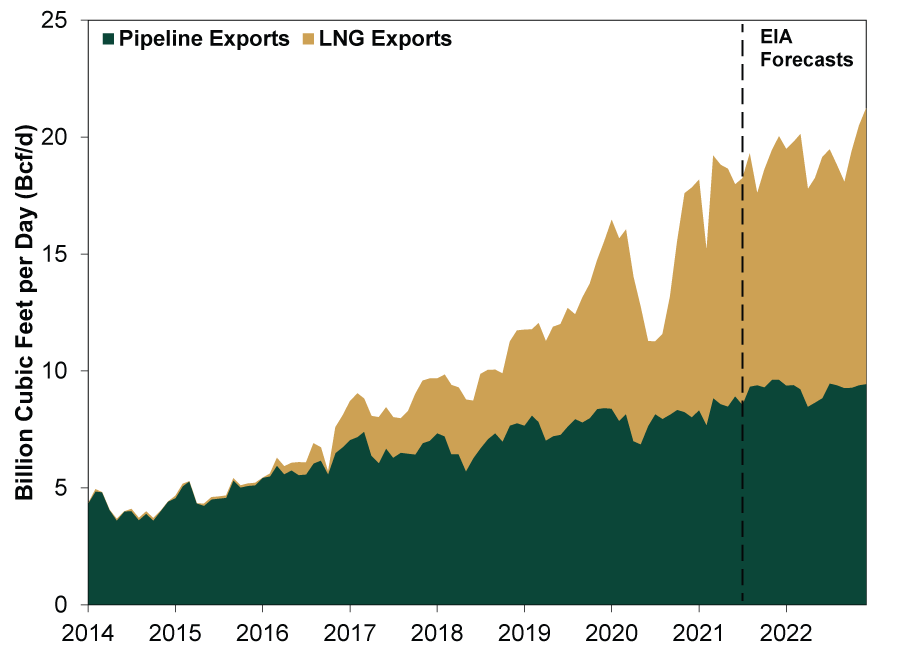

Qatar, a world LNG export leader, is lining up contracts and boosting production accordingly—with longer-term plans to expand capacity greatly. However, like with container shipping generally, it is seeing long tanker backups, too. Algeria, a key supplier to Southern Europe, is also ramping up production, although a spat with Morocco is complicating matters presently. Last, but not least, American gas exports—second after Russia’s—are hovering near record highs. (Exhibit 1) The US Energy Information Administration (EIA) expects natural gas exports to smash 2020’s record by 27% this year.[iv]

Exhibit 1: US Natural Gas Exports

Source: EIA, as of 9/30/2021. US natural gas pipeline and LNG exports, January 2014 – July 2021, and EIA forecasts, August 2021 – December 2022.

Meanwhile, China has ordered its coal miners to produce as much as possible, even if it exceeds their annual quotas, and directed its banks to fund the expansion—all to keep power plants operating. China is also securing oil contracts to meet its energy needs—which America’s shale producers and OPEC+ stand ready to supply. Yesterday, OPEC+ confirmed its plan to raise its oil supplies by 400,000 barrels per day in November. Then too, in Europe, data from WindEurope suggest stronger wind generation is starting to alleviate pressure. Hence, on Monday, European wholesale spot power prices fell more than -11% as rising wind supply forecasts swept the Continent.[v] It is a short-term trend thus far, but it could help price pressures abate if it persists. Longer range, Germany has plans to shutter existing coal and nuclear capacity, but it could delay them. As for the UK, it is hiring drivers, raising pay packages and luring people from other industries (e.g., the army) and countries like Romania, where tax levies there are driving truckers away.

Still, on top of existing worldwide transportation bottlenecks, the energy situation isn’t great. To the extent policymakers enact subsidies for households, they will lessen normal demand destruction. There are positive and negative aspects to that. While it may make winter heating more affordable, by itself, it does nothing to address shortages—and could exacerbate supply problems. Overall though, while production issues will take time to work out, they usually resolve before too long given the strong incentives to fix them. In short, yes, a severe energy crunch is cause for concern, but we don’t think it rises to an insurmountable crisis as producers and consumers alike respond and adjust to circumstances. Besides, how long it lasts is vital. If short lived, any economic impact would be quite small.

Markets are well aware of the situation. For investors, oil and gas price spikes don’t appear to be sneaking up on stocks, which we think are pricing in events and expectations swiftly. The MSCI World Energy sector surged 10.2% in September, while all other sectors fell.[vi] More adjustment may be in store, and volatility can strike for any or no reason. But by the same token, we caution against reacting to short-term moves—volatility can end just as swiftly.

Now, energy price spikes have preceded recessions and bear markets (typically a lasting decline exceeding -20% with an identifiable cause) before, so we aren’t dismissing their economic and financial effects out of hand. Although most companies have been able to work—and expand—through supply-chain troubles thus far this year, chronic power outages may be another matter. However, for this to sink stocks, it would have to be longer lasting and more widespread than anyone currently thinks or fears, particularly with developed nations getting more energy-efficient over time. While we are keenly on the lookout for this potential, we don’t see it as likely at this point.

[i] “European Gas Hit Record 100 Euros as Energy Crunch Worsens,” Anna Shiryaevskaya, Vanessa Dezem and Elena Mazneva, Bloomberg, 9/30/2021.

[ii] Source: FactSet, as of 10/5/2021. Natural gas price per metric million British thermal unit, 4/5/2021 – 9/28/2021.

[iii] Ibid. Brent crude oil price per barrel, 8/20/2021 – 10/5/2021.

[iv] “U.S. Natural Gas Net Trade Is Growing as Annual LNG Exports Exceed Pipeline Exports,” Kristin Tsai, EIA, 8/16/2021.

[v] “Rising Wind Weighs on Spot Prices,” Forrest Crellin, Reuters, 10/4/2021.

[vi] Source: FactSet, as of 10/5/2021. MSCI World Energy return with net dividends, 8/31/2021 – 9/30/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today