Personal Wealth Management / Market Analysis

June’s Global Flash PMIs Still Look Ok

With more businesses reporting growth than not, recession still doesn’t look like a foregone conclusion.

Another month, another round of flash purchasing managers’ indexes (PMIs) giving an early read into major economies’ business activity. Though they mostly ticked down in June, prompting more recessionary chatter, their levels still indicate overall expansion. It may not be gangbusters, but stocks don’t need perfection to mount a recovery from this year’s downturn—just for reality to beat dreary expectations.

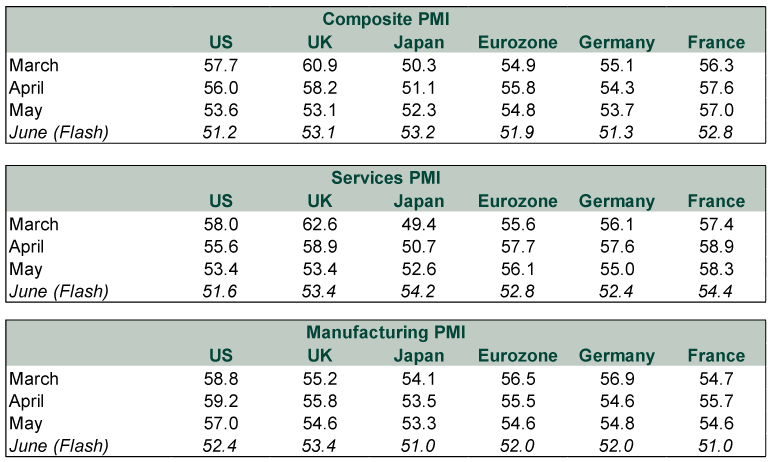

PMIs are surveys that aim to measure growth’s breadth. Readings above 50 indicate the majority of surveyed firms reported expanding business activity, with growth (and contraction) theoretically accelerating the further readings drift from that marker. PMIs don’t say anything about how much their businesses grew (or shrank), only that they did, so they are a timely but loose estimate of economic activity at best. Among the various readings, the composite PMI combines services and manufacturing, but it is a narrower measure of their “output” that focuses only on production. The services and manufacturing PMIs are broader, including new orders, backlogs, suppliers’ delivery times and employment. That is why, for example, the composites for June’s US, UK and eurozone PMIs can be below each of their services and manufacturing PMIs.

Exhibit 1 shows major economies’ PMIs remain above 50—though they are down from the spring, implying deceleration (Japan excepted). The US and eurozone’s June flash composites, released with only 85% – 90% of responses in, fell to the low 50s, continuing a generally slower trend. This includes both services, which comprise the bulk of developed market economies, and manufacturing. But while low-50s PMIs aren’t historically robust, they generally coincide with pedestrian growth.

Exhibit 1: Major Economy PMIs

Source: FactSet and S&P Global, as of 6/23/2022. Flash PMIs are preliminary estimates based on 85% – 90% of responses.

Also note, the downward trend isn’t global—Japan’s composite PMI rose and the UK’s was flat. Japan’s lift was services-based as COVID restrictions eased there. Reopening-related boosts helped buoy UK services, too, as more workers returned to the office and patronized surrounding businesses. However, Japanese and UK manufacturing weakened alongside the rest of the developed world as Chinese lockdowns hit global supply chains.

As a whole, the picture here appears mixed. Business activity growth is less broad-based. But through mid-June at least, the pockets of strength seemingly outnumbered the pockets of weakness. Whether that translates to actual economic growth, we will see when output data roll in.

For many, this isn’t exactly consoling. As we wrote in early June for the eurozone, there are some discrepancies between “soft” survey data and “hard” sales and volume data, with some signs of contraction in the latter. In the US and UK, May retail sales fell -0.3% m/m (nominal) and -0.5% (real), respectively.[i] But we don’t think this is conclusive, as it may reflect a continuing shift back to services spending from goods—a return to normal, not necessarily weakness. Hard services data tend to lag, which is why timelier PMIs are helpful and looking at both provides a fuller picture, if only in broad brushstrokes.

Based on our read of all the data so far, it is premature to declare a recession is underway. Some quantitative efforts to derive GDP from monthly indicators—like the Atlanta Fed’s GDPNow—might seem to disagree, but these models aren’t air-tight. GDPNow currently predicts 0.3% annualized Q2 growth given available data.[ii] But the most telling component, personal consumption expenditures—71% of GDP—won’t be released until month end, and that is just May’s number.[iii] More broadly, these nowcast models are young, with a spotty record of accuracy. The New York Fed’s proved so inaccurate that they have temporarily ceased publication, pending methodological improvements. The St. Louis Fed’s attempt currently estimates 3.9% annualized growth in Q2, but neither it nor the Atlanta Fed’s model predicted Q1’s inventory-fueled GDP contraction.[iv] Absent a foolproof tool, investors must survey the entire landscape and make their best judgments. For now, we are inclined to interpret PMIs as more evidence economies aren’t uniformly weak despite well-documented struggles.

Notably, though, even survey data have some weak points worth monitoring. Deteriorating new orders may suggest demand is faltering—but it is too early to tell. Relative services strength may be fading, but whether that is normalization following the initial reopening boom or something worse—e.g., cost of living pressures taking a more lasting toll—remains to be seen. Meanwhile, manufacturing’s downtrend, beset by component shortages, could reverse as supply chains recover. Some businesses, particularly in the consumer world, apparently overstocked trying to compensate amid surging goods demand. They may just have inventory overhangs they need to work through—a more temporary hiccup than needing to get lean to correct prior excess.

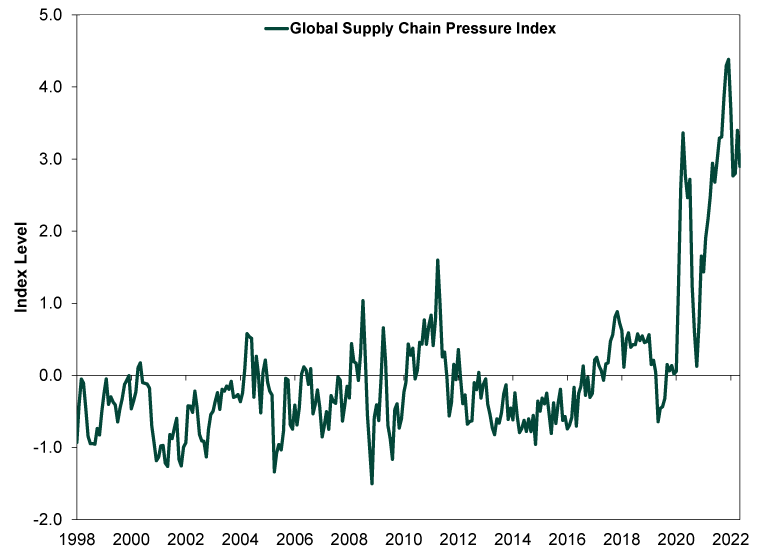

We also see some other encouraging nuggets. The PMI surveys indicate falling backorders, which could be signaling easing supply chain and price pressures. This may be occurring as headwinds from China’s choppy reopening fade. One hint: The New York Fed’s Global Supply Chain Pressure Index, which aggregates transportation costs, input-output prices and other measures—like PMIs’ delivery times, backlogs and inventories—to gauge the overall intensity of bottlenecks’ disruption on world trade. (Exhibit 2) While still at lofty levels, it has started subsiding and may be past its peak.

Exhibit 2: Global Supply Chain Pressures Elevated, but Easing

Source: Federal Reserve Bank of New York, as of 5/18/2022. Global Supply Chain Pressure Index, January 1998 – May 2022.

For investors, the most salient aspect of the latest PMI releases may be their accompanying bearish sentiment. Given the market environment, it isn’t surprising. But we still think it is notable that PMI coverage widely extrapolates imminent recession—which the data don’t confirm, at least yet. The evidence, as we have explored, is more mixed. While recession is possible, we think the global economy’s resilience is just as remarkable given the challenges it has faced year to date. This is an underappreciated positive to us.

Recession uncertainty has undoubtedly weighed on markets lately. But by the same token, it lowers the expectations bar reality needs to clear to surprise stocks positively. In our view, increasing economic clarity in the second half—even if it just muddles through—will likely provide relief.

[i] Source: FactSet, as of 6/24/2022. US and UK retail sales, May 2022.

[ii] Source: Federal Reserve Bank of Atlanta, as of 6/27/2022. GDPNow, Q2 2022.

[iii] Source: BEA, as of 5/26/2022. PCE percentage of real GDP, Q1 2022.

[iv] Source: Federal Reserve Bank of St. Louis, as of 6/24/2022. Real GDP Nowcast, Q2 2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today