Personal Wealth Management / Market Analysis

Junk Bonds’ Funk Does Not Mean Stocks Are Sunk

Recent weakness in high-yield bonds doesn't necessarily mean stocks are destined for a fall.

Do junk bonds know something stocks don't? High-yield bonds have taken it on the chin, and since they tend to closely track stocks at times, some suggest this is a harbinger of looming trouble for the stock market. But this oversimplifies the connections between stocks and junk and overlooks why junk bonds are having a rough time. No similarly liquid asset class can inherently predict another, and junk bonds' recent weakness doesn't necessarily signal trouble for stocks.

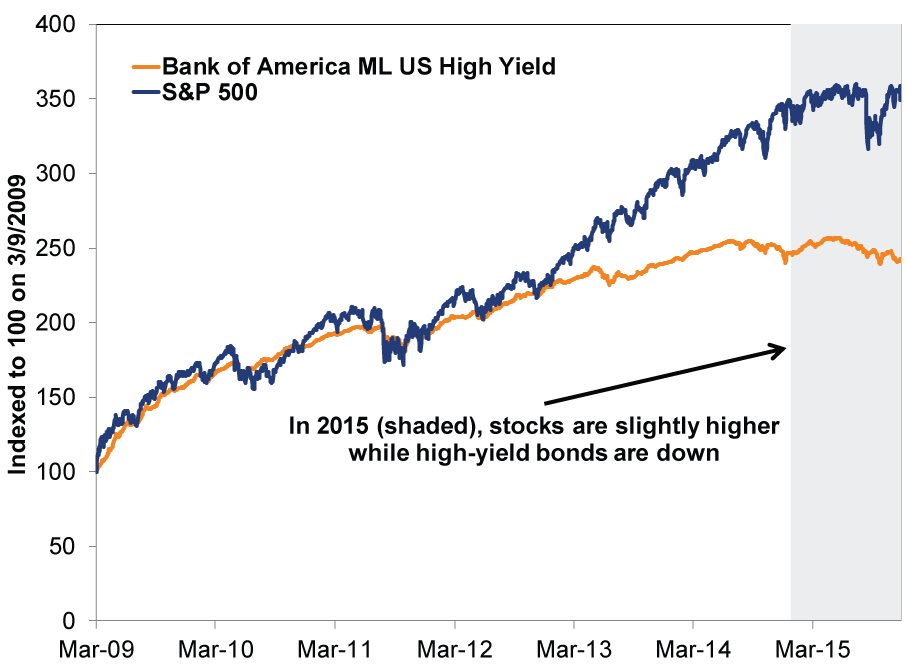

Both stocks and junk bonds rose nicely (to varying degrees) from 2009 until about a year ago, when junk bonds slid as stocks rose. After a brief bounce back earlier this year, junk bonds have fallen while stocks are up slightly.

Exhibit 1: Stocks vs. High-Yield Bonds

Source: Factset, as of 12/8/2015. S&P 500 and Bank of America Merrill Lynch US High Yield Index total returns, 3/9/2009 - 12/4/2015.

This divergence has prompted some to suggest junk bonds are sending a warning signal for stocks, given the two are directionally correlated most of the time. Fueling the fire, high-yield defaults are up. So are yields relative to Treasurys. This suggests the high-yield market sees some kind of risk; the question is whether that risk applies to stocks broadly.

High-yield bonds and stocks are heavily influenced by broad economic conditions. This is why they often track each other and why many suggest weak high-yield bonds mean trouble for stocks. They presume falling high-yield bonds reflect a weakening economy, while stocks are sleepwalking towards an inevitable drop. But this is a hasty conclusion. Economic conditions are one input into both stocks and high-yield bonds movements, but they aren't the be-all, end-all. Issuer health is the kicker. Broad stock markets reflect profit trends of a diverse group of industries and are weighted heavily to the largest companies, which tend to be highly creditworthy. High-yield bonds, on the other hand, are issued by less-creditworthy firms.

Sector and industry-specific factors play a large role in that. Currently, the broad economy is growing, a tailwind for stocks and junk bonds. But the commodity sectors (Energy and Materials) are struggling because oil and other resource prices have cratered, pressuring producers' revenues. Many smaller, capital-intensive commodity producers raised money by issuing bonds (which are frequently high yielding because these firms are less creditworthy than larger companies), and plunging revenues make it difficult to pay interest and principal due to creditors. Some have defaulted already; others are on the brink.

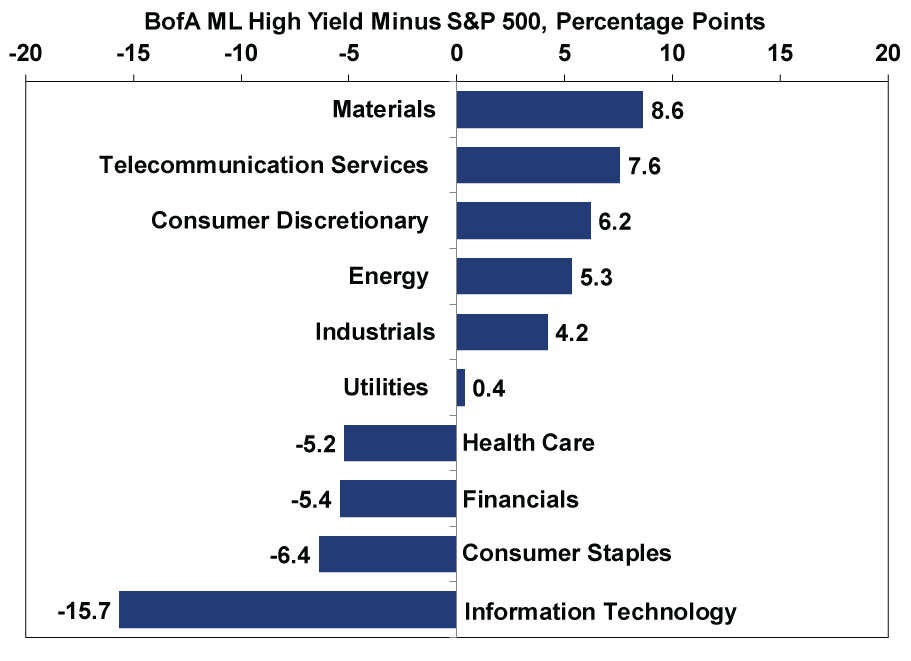

These companies are a small slice of the stock market, but they represent a disproportionate amount of the high-yield bond market. At the same time, sectors doing just fine these days, such as Technology, Health Care, Financials and Consumer Staples, are a tiny slice of the junk bond market. These sectoral differences, shown in Exhibit 2, go a long way toward explaining the divergence between broad stock and high-yield bond markets over the last year.

Exhibit 2: S&P 500 vs. High Yield Bond Sector Weightings

Source: Factset, as of 12/7/2015. Bank of America Merrill Lynch High Yield Master II Index sector weight minus the S&P 500.

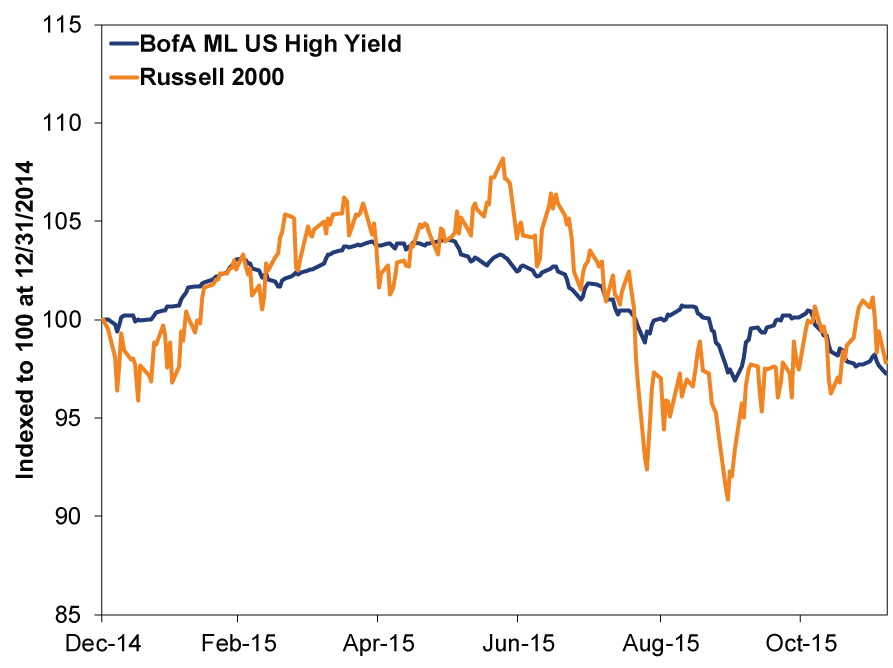

Though the S&P 500's moves don't much resemble junk bonds', that doesn't mean stocks are blissfully unaware of what's afoot in the high-yield market. Strip away the bigger firms, and gauges of small cap stocks-often less creditworthy-are down similarly to high-yield bonds this year. This likely reflects investors shunning companies that are less creditworthy and instead embracing higher quality firms.

Exhibit 3: Small Cap Stocks vs. High Yield Bonds

Source: Factset, as of 12/8/2015. Bank of America ML High Yield Index, Russell 2000, 12/31/2014 - 12/7/2015.

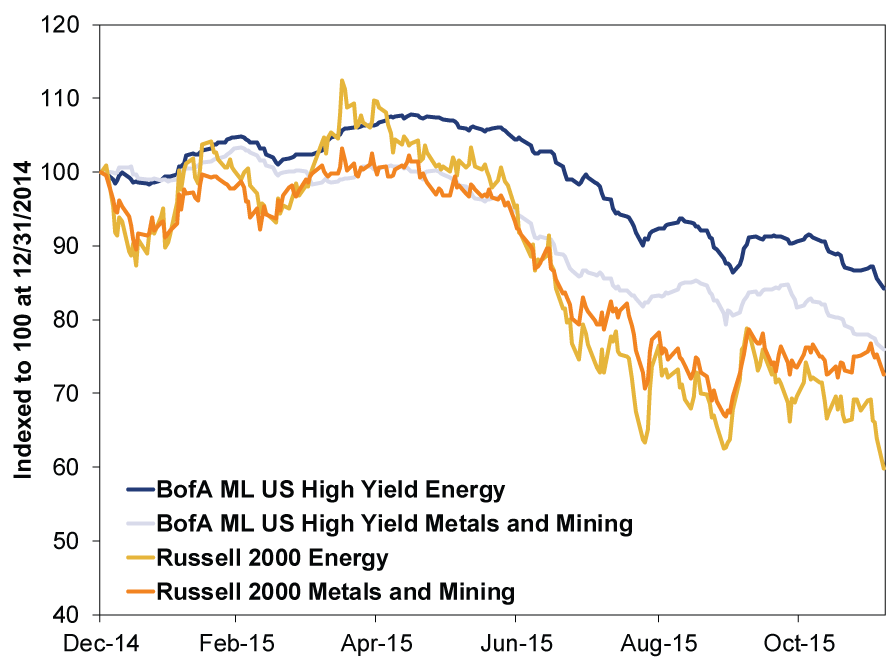

Also, Energy and Materials stocks-especially smaller firms whose debt tends to be non-investment grade- have declined sharply, mirroring these sectors' high-yield bond drops.

Exhibit 4: Small Cap Energy and Metals and Mining vs. High Yield Bonds Energy and Metals and Mining

Source: Factset, as of 12/8/2015. Bank of America Merrill Lynch US High Yield Energy and Metals and Mining and Russell 2000 Energy and Metals and Mining, 12/31/2014 - 12/7/2015.

Bond markets aren't a leading indicator for stocks. They can't be. Sufficiently liquid markets discount all widely known information near-simultaneously. Stock markets are just as aware of everything the high-yield bond market knows, and it's very unlikely one is more insightful than the other. That stocks of distressed resource companies are down sharply along with their bonds is evidence of this. As is the fact other sectors, for whom lower Energy prices are a positive, are doing much better.

Some claim junk bonds' troubles are evidence the credit cycle is shifting, imperiling all corporate borrowers and putting stocks at risk as funding dries up. While this will likely eventually come true-it is more or less a typical part of a downturn-we don't think it is a problem in the here and now. High-yield credit spreads over Treasurys are up in recent months, but they are still much lower than during past recessions (and here, too, Energy and Materials skew the average higher). Today's spreads look most like 2011, when no recession or bear market came. While some claim a Fed hike could further pressure high-yield issuers, long-term rates-which are set mostly by free market forces-don't necessarily move in lock-step with short rates (set by central banks). Presently, about 73% of junk bond debt has a maturity of over four years, suggesting market forces are a much bigger influence than the Fed.

Similarly, while high-yield bond default rates have spiked lately, Energy and Materials firms bear most of the blame. This likely means a wave of consolidation in the field looms, but it doesn't necessarily signal broad weakness. It doesn't even mean high-yield firms outside these sectors have been shut out of credit markets. Through November, issuance is down -15% versus 2014 through 11 months. But this pales in comparison to 2008's -68% decline (when there was a bear). It's far lower than 2005's -30% issuance decline, a perfectly fine year of expansion and bull market.

In our view, the troubled issuers today are too small a slice of the broad stock market to drive a broad decline. Energy and Materials companies-the most troubled sectors of the high-yield bond market-represent about 20% of the $1.1 trillion US junk bond market. And it is highly unlikely those issuers all default. After all, during 2008's financial crisis-when the entire market was under pressure-the high-yield default rate peaked just over 10%. If we're generous, a similar default rate now implies about $30 billion in defaults. That's a drop in the bucket relative to total debt outstanding-according to the Federal Reserve, non-financial US corporations have over $7.8 trillion in debt outstanding. Banks also aren't holding material amounts of high yield, so the potential for them to act as a transmission mechanism to stocks (a la 2008's securitized debt) is low.

As we've noted, it takes a negative with the power to wipe trillions from global economic activity to wallop a bull market. We just don't see a negative on that scale here. High-yield bonds may be in for more rough sledding as commodities industries face a shake out, but this would likely be a sector-specific event, not a broad-based bear market.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today