Personal Wealth Management / Market Analysis

Keep COVID Relief Payment Expectations in Check

What chatter about COVID relief checks’ economic impact says about sentiment today.

In one sign of today’s widespread optimism, February’s bigger-than-expected consumer spending dip—reported late last week—didn’t trigger the usual handwringing and grousing over American consumers’ health. Most coverage rationally noted the weakness was likely temporary. However, the brighter outlooks didn’t stop there, as many turned their gaze forward to a coming spending surge, buoyed by federal COVID relief. Many pundits suspect that will push economic growth to a higher plateau. While a short-term bounce wouldn’t shock us, we don’t think a lasting boom is likely—worth keeping in mind, especially when it comes to monitoring how expectations align with reality.

February personal consumption expenditures (PCE)—a broad gauge of US consumer spending—fell -1.0% m/m, slightly worse than expectations for -0.6%.[i] As many economists observed, the month’s severe weather likely knocked spending. Winter storms forced many retailers and restaurants to temporarily close and kept many Americans home, particularly in the Northwest, Midwest and South. But as many financial outlets sensibly noted, it is now spring. Winter storms probably aren’t a future headwind. Less rational, in our view: the broad anticipation of a stimulus-fueled spending surge forward.

We have seen many extrapolate COVID relief payments now rolling out to many nationwide into huuuuuuuge new consumer spending, but these projections have some holes. For one, it is tough to peg how exactly recipients will use their payments, as survey data reveal. A National Bureau of Economic Research (NBER) survey found nearly 60% of the first direct payments were either saved or went to pay off debt.[ii] A Federal Reserve Bank of Philadelphia survey reported a similar development: COVID relief checks had multiple uses, including going to savings or debt payments.[iii] That trend didn’t abate with the second round of checks, either. According to the Census Bureau’s Household Pulse Survey, which aims to track the pandemic’s impact on American households, about half of recipients reported using their second check to reduce debt.[iv] Now, surveys can’t provide exact breakdowns, but these findings throw cold water on the notion relief payments turned immediately into new spending.

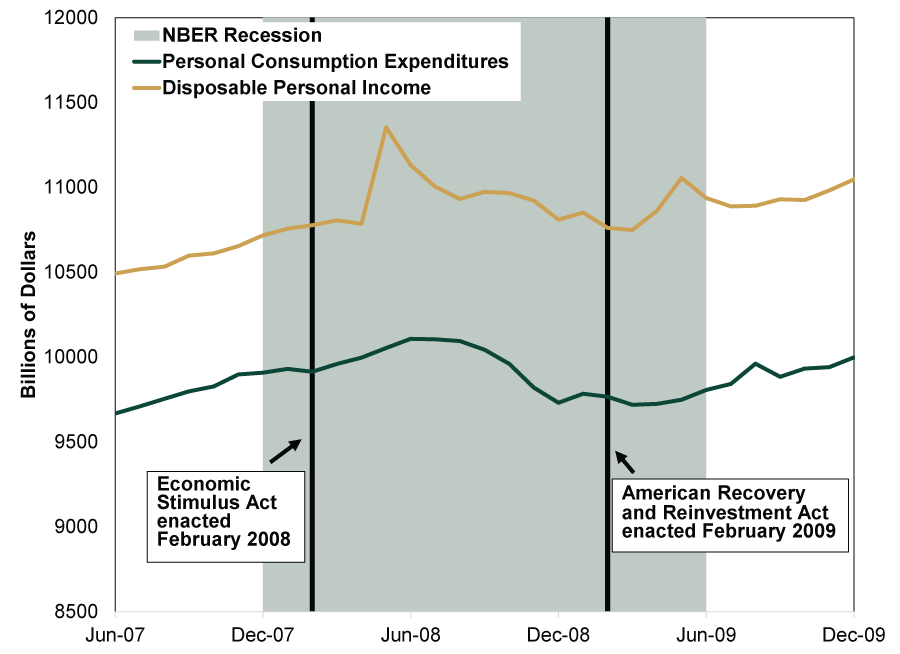

This isn’t a unique development, as past one-time direct payments haven’t proven to meaningfully lift consumer spending. The Economic Stimulus Act of 2008 and the American Recovery Reinvestment Act of 2009—signed by Presidents George W. Bush and Barack Obama, respectively—both included one-time cash payments. The short-term boosts to disposable income didn’t yield a long-lasting surge in consumer spending. (Exhibit 1) Earlier one-time cash payments during and after the 2001 recession had a similar small effect.

Exhibit 1: More Cash Doesn’t Necessarily Mean More Spending

Source: St. Louis Federal Reserve, as of 3/30/2021. Personal consumption expenditures and disposable personal income, billions of dollars, monthly, June 2007 – December 2009. NBER recession dating used.

In our view, it is premature to pencil in a $400 billion economic shot in the arm this year thanks to COVID relief checks—to the extent it would even be possible to quantify. While consumer spending likely will pick up in the near future, we think that will have more to do with COVID restrictions easing—similar to last year’s economic data rebound after states relaxed their springtime lockdown measures. Moreover, neither a reopening surge nor any spending boost due to relief checks is likely to prove lasting, undercutting the notion of fiscal policy-driven, Roaring Twenties-style economic growth. Expectations for a stimulus-driven boom strike us as a this time is different argument—as dangerous a line of thinking when it takes an optimistic slant as when it takes a negative one. Those anticipating gangbusters, government-aided growth are likely to be disappointed.

In our view, the reaction to the latest consumer spending data is further evidence of sentiment’s evolution to widespread optimism—rational, in our view, but also a reminder that euphoria is probably on the horizon. To us, this isn’t reason to act right now, though. Even when it arrives, euphoria’s presence alone doesn’t signal the start of a bear market. Rather, euphoria typically contributes to ending bull markets by blinding investors to nearby, huge negatives. We don’t think we are there yet. While we disagree COVID relief checks will spur consumer spending to lasting, lofty heights, the economic recovery will likely continue as states continue loosening COVID restrictions and vaccine distribution becomes more widespread. That is a good thing. However, extrapolating a boom far beyond reopening driving a return toward normality is likely an error. Monitoring the reaction to economic data in the coming months will provide more clues of sentiment’s ongoing development—and whether expectations are getting ahead of reality.

[i] Source: FactSet, as of 3/30/2021.

[ii] “Most Stimulus Payments Were Saved or Applied to Debt,” Laurent Belsie, NBER, October 2020.

[iii] “CFI COVID-19 Survey of Consumers – Wave 2 Updates, Impact by Race/Ethnicity, and Early Use of Economic Impact Payments,” Tom Akana, Consumer Finance Institute: Federal Reserve Bank of Philadelphia, June 2020.

[iv] “Household Pulse Survey Shows Stimulus Payments Have Eased Financial Hardship,” Daniel J. Perez-Lopez and Lindsay M. Monte, Census Bureau, 3/24/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today