Personal Wealth Management / Economics

Listen to Markets' Signals

Markets often send distress signals long before the bad outcomes materialize.

Legendary value investor Benjamin Graham once, famously, said: "In the short run, the market is a voting machine but in the long run, it is a weighing machine."

While markets can, in the very short term, send confusing signals heavily skewed by sentiment's whims, more often than not they are efficient and rational. They are weighing the evidence and showing you the verdict. Yet all too often, investors and pundits disregard the signals markets send. In the last week, two articles illustrate plainly the power correctly heeding the market's signals can bring. You ignore these signals at your own peril.

One lesson these signals consistently send: There is no such thing as a free lunch. The idea that you can get high yield with low risk is a consistent investor error, one many are likely making while we type this sentence. Let's be clear: High yields are a signal markets require more compensation for risk taken. It's intuitive-the bigger the risk, the bigger the reward. Yet again and again, investors flock to high-yielding securities, perceiving them as stable alternatives in a world of otherwise low yields. But they are anything but, and investors eventually re-learn this timeless truth the hard way.

The latest example comes courtesy of a relatively new type of convertible bank bond. These bonds-which are subordinate debt and carry the risk of either missing payments or being converted to equity when banks get in trouble and needs capital in a pinch-yielded over 7% on average as of year-end 2015. While most of the owners of these securities are institutions who should (and probably did) know better, some individual investors reportedly bought them for their rich yields and presumed them as safe as a savings account. But high-yielding bonds provide a greater fixed payment for a reason: They carry greater risk. In this case, the risk is that if the bank becomes under-capitalized, the bonds may not pay interest or principal due. They may even convert into equity when the bank is stressed, which is the opposite of safe. This is what these bonds are designed to do. When investors began fearing big European banks may be (or will soon become) under-capitalized, these bonds plummeted as investors feared they may be used to "bail in" the bank. As Bloomberg's Matt Levine recently wrote:

"Here's the thing. If you are buying something with an 8 percent coupon in a world of zero interest rates, and you somehow think it's a risk-free bank deposit, I don't want to hear about it. That's not a thing. The coupon tells you the risk. If you bought it for the 8 percent coupon, you ipso facto knew it was risky ..."

While this commentary specifically targets a rather arcane corner of the bond market, the mistake of ignoring the risk signal high yields send is common elsewhere. Investors flock to assets they presumed were "bond alternatives" like Real Estate Investment Trusts (REITs), Master Limited Partnerships (MLPs), Business Development Companies (BDCs) and high-yielding stocks, eschewing asset allocation, diversification and the simple fact you won't get high yield without taking on higher risk. These investors, in many cases, have been taught a harsh lesson.

MLPs are a fine thing, but the presumption they were a "safe" alternative to bonds with higher yields was never correct. MLPs are, for all intents and purposes, stocks. And they are stocks in energy-infrastructure firms! Many investors believed MLPs were immune to big swings in oil prices because they aren't actually selling oil, just collecting tolls for transporting it. But as prices fall, MLP's customers come under pressure. And prices themselves send a signal to Energy firms: Make less crude oil. Eventually production will fall, and as less oil flows through pipelines MLPs will suffer. Investors who didn't heed MLPs' higher yields have been hard hit. The Alerian MLP Index has fallen -48.5% from its August 29, 2014 peak, including reinvested dividends![i] (Another valuable lesson for yield-hungry investors: Consider an asset's total expected returns, not just its yield.)

REITs are also a typically high-dividend yielding asset class that enticed investors desperately searching for yield. But these, too, trade like stocks-not bond replacements. From its February 7, 2007 high to its March 6, 2009 low, the FTSE NAREIT All REITs index fell -72.7%--again, including reinvested dividends--more than the S&P 500.[ii]

BDCs are yet another, though less well known, asset class that lures investors with high yields but are even more volatile than stocks. Heck, right now the median BDC yields more than 12%! Rich! But BDCs are in the financing business, and their prices move like small-cap banks. As such, if Financials aren't in favor, BDCs likely get punched hard. Since its pre-Financial Crisis high on July 6, 2007, the Market Vectors US Business Development Company Index is up 6.0%, cumulatively, through 2/29/2016.[iii]Meanwhile, the S&P 500 is up 52.3% over the same period.[iv] And BDCs achieved that muted return despite bigger-than-equity volatility! Chasing yield could have cost you far more in total return-and heartache-than investing in a more diverse manner. The market gave you a hint with their lofty yields.

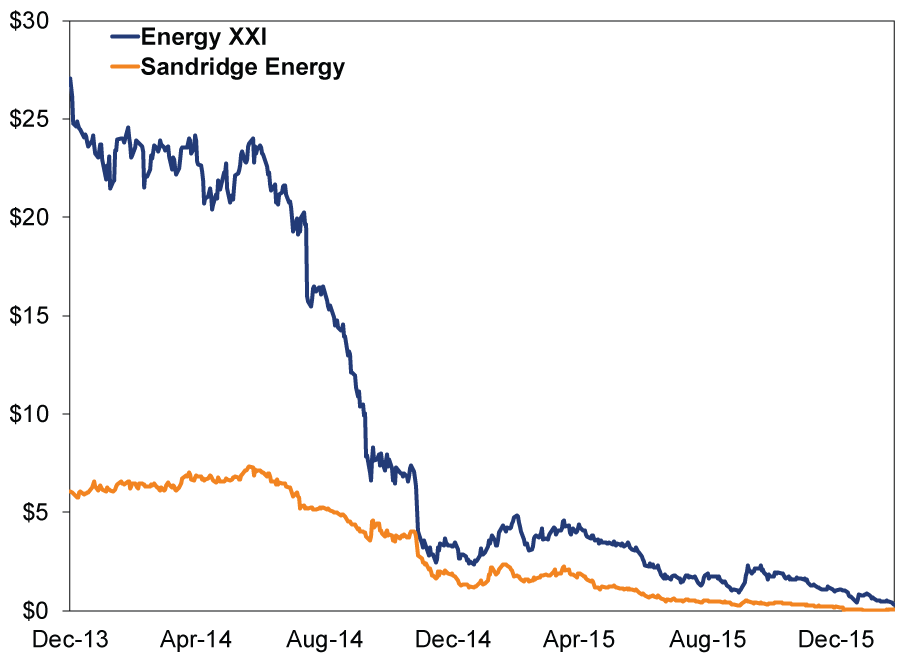

It isn't just yields that send signals-stock prices can too. Consider the much-ballyhooed fear of Energy defaults, which some believe is the trigger that causes Energy firm's woes to mushroom. Last week, news broke that two Energy firms-Energy XXI and SandRidge Energy-were threatening creditors with nonpayment of interest due. One report on the issue noted that, "If the two companies fail in March, it would be the biggest cluster of oil and gas defaults in a month since energy prices plunged in early 2015." But the thing is, it isn't as if markets were blissfully unaware this scenario may develop. Markets have long been signaling that problems have been mounting in the Energy bond universe, as the Bank of American/Merrill Lynch US High-Yield Energy Bond Index is down more than -40% since August 29, 2014.[v]. Debt markets often price in defaults well before they materialize.

So do stock prices. Energy XXI's and SandRidge Energy's stocks each fell about 99% from 12/31/2013 through 2/24/2016, as the firms bled through cash reserves and revenues cratered along with oil prices. When stocks fall this much, the market is saying bankruptcy is a very real possibility. Markets long ago reflected the risk the media thinks is "news."

Exhibit 1: Two Energy Stocks' Big Falls

Source: FactSet, as of 2/24/2016. Energy XXI and SandRidge Energy common stocks, 12/31/2013 through 2/24/2016.

And this isn't sneaking up on lenders, either. While most Energy exposure is in the bond market-not at banks-those that do have exposure took heed of markets' signals. Banks from JPMorgan to Wells Fargo and oil patch banks have greatly boosted their loan-loss reserves to account for the increased risk Energy borrowers default. Thinking that these defaults are a lurking wallop just waiting to squash stocks misses the fact stocks are already aware-an omission that could increase the risk you erroneously exit stocks.

While markets can be irrational in the near term, they're quite rational and efficient in the medium to longer term. The challenge for investors, as always, is to heed the markets' signals, verify them against underlying fundamentals and project where developments go from here. All too often, though, folks ignore step one.

[i] Source: FactSet, as of 3/1/2016.

[ii] Source: FactSet, as of 3/1/2016.

[iii] Source: FactSet, as of 3/1/2016. Market Vectors Business Development Companies Index with reinvested dividends, 7/6/2007 - 2/29/2016.

[iv] Source: FactSet, as of 3/16/2016. S&P 500 Total Return, 7/6/2007 - 2/29/2016.

[v] Source: FactSet, as of 3/1/2016. 8/29/2014 - 2/29/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today