Personal Wealth Management / Economics

Looking Past Small Shifts in Numbers

The sentiment reaction to tiny data shifts is often more telling than the data.

How many angels can dance on a pin? Maybe we ought to pose this classic medieval question to economic commentators. In recent weeks, a minute inversion of the US yield curve spawned a biblical flood of recession-fearing headlines. Similarly, in recent months the prophets at the IMF, World Trade Organization and OECD all downgraded 2019 growth forecasts—by fractions of a percentage point. Media saw all these as signs trouble loomed over stocks and the economy. But like debating the number of toe-tapping halos, fretting over microscopic movements—and forecasts—is time wasted, in my view. This is a case where the reaction to the alleged news tells you far more than the actual news itself.

Consider, first, late March’s yield curve inversion. The yield curve compares the interest rates of different maturity bonds from the same issuer. Usually, long rates top short rates, largely because borrowers extending funds for long periods have to account for more exposure to risk—and the potential they could have done better deploying the money elsewhere (the time value of money, in finance geekspeak). This is a positively sloped yield curve. Economically, it is beneficial as banks borrow short term to fund long-term loans, with the spread their profit.

Inverted yield curves—when short rates top long—mean lending may be unprofitable. It has historically been a fair indicator of troubled credit markets and a decent predictor of recession as a result. Media are well aware of this last point and have hyperventilated for months over various less-telling parts of America’s yield curve inverting. So it was no surprise that, when the 10-year US Treasury yield fell below the 3-month yield on March 22—inverting perhaps the most commonly watched curve—headlines shrieked of impending weakness.

But while the yield curve is useful, it isn’t an automatic indicator of recession or a stock-market downturn. There are false reads. Even when the read isn’t false, there is usually a lag between inversion and a bear or recession starting. Further, as MarketMinder Senior Editor Elisabeth Dellinger wrote recently, the global yield curve matters more than any individual nations’, in our view, as banks can fund lending globally quite easily.

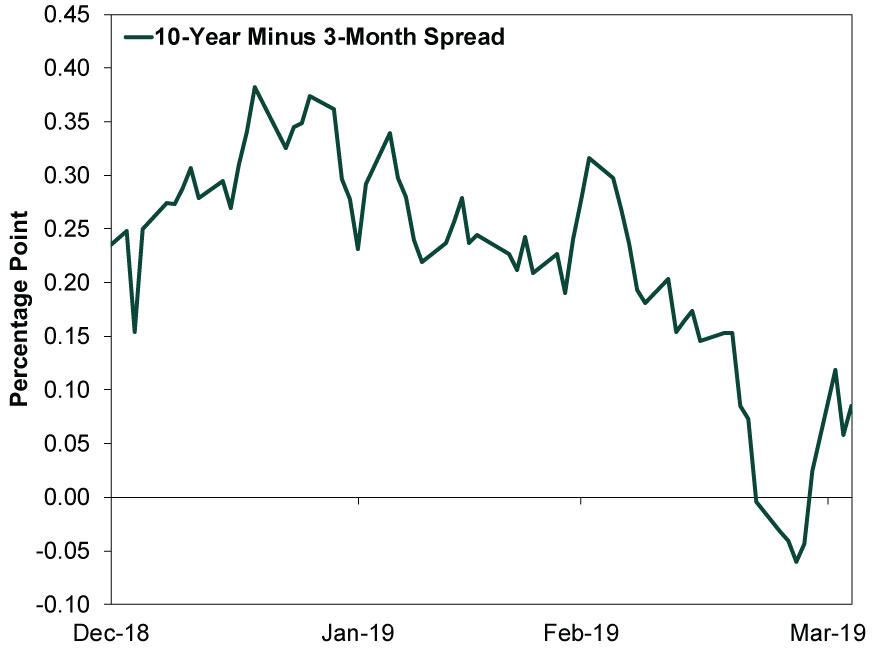

But there is another reason to question media’s alarm bells: the shallowness of the inversion. The deepest inversion thus far this year is just -0.06 percentage point.[i] To summarize something my colleague Pete Michel and I discussed: If you weren’t worried about a yield curve that was positive by 0.06 percentage point, you shouldn’t be worried about this inversion. Why? Banks base pricing on government yields, but they don’t match them—they add a spread. Further, an inversion this teensy could revert fast. Just like it did by March’s close.[ii] (Exhibit 1)

Exhibit 1: The Miniscule Inversion

Source: FactSet, as of 4/4/2019. US 10-year Treasury yield minus 3-Month Treasury yield, 12/31/2018 – 4/3/2019.

Of course, it could head south once more. But unless and until it heads far lower—alongside the global yield curve—don’t overthink it. No economic indicator or forecasting tool is that precise, in my view.

Similarly, consider supranational bodies’ economic forecasts. In January, the IMF cut its 2019 global GDP growth forecast to 3.5% from 3.7%.[iii] (They may update this again in the semi-annual revision to the IMF’s World Economic Outlook, due any day.) In March, the OECD followed suit, cutting its outlook from 3.5% world GDP growth in 2019 to 3.3%.[iv] Tuesday, the World Trade Organization said it projects a slowdown from 2.9% GDP growth last year to 2.6% in 2019.[v]

Think what you will of these various forecasts and their rationales, which cite a variety of factors including Brexit, tariffs, Chinese slowing and more. But a key for stocks is that all of them show growth with revisions so small they are a rounding error. Economists, as many have documented, struggle to forecast recessions. But for some reason, media and many economic commentators seemingly think these supranational bodies’ economists can determine the slightest change in growth trajectory. This seems a skosh dubious.

Economic growth is the result of billions, if not trillions or quadrillions, of interactions between business people, consumers, investors, borrowers and lenders. To me, it is the height of hubris to think anyone can measure this with precision. Yet each time a supranational body slashes its growth outlook, media treats it as gospel, flooding websites globally with fearful headlines.

That is what is actually seems important about minor, teensy shifts: how folks commonly react. To stocks, it likely doesn’t even matter if the IMF pinpoints 2019 GDP. It likely matters if investors, en masse, fear their forecast—or chalk it up as wrongheaded. It is a way to see where sentiment is—the same way media’s big freakout over the small US yield curve inversion sets up a potential positive surprise if/when recession doesn’t follow.

Typically, the time to worry isn’t when every headline shrieks of inversion and downgraded forecasts. Those fears get baked into markets. The time to worry, generally, is when everyone decides those things are as irrelevant as counting angels dancing on pinpoints.

[i] Source: FactSet, as of 4/4/2019. 10-year minus 3-month US Treasury yield, 12/31/2018 – 4/3/2019.

[ii] Ironically, this means that some data providers like the St. Louis Fed won’t capture the inversion, as their series consist of monthly data.

[iii] “IMF Says the Global Economic Expansion Is Losing Momentum as It Cuts Growth Forecasts,” Silvia Amaro, CNBC, 1/21/2019. https://www.cnbc.com/2019/01/21/imf--cuts-global-growth-outlook-2019-2020.html

[iv] “Global Economic Growth Forecasts Cut Again by OECD,” Sudip Kar-Gupta, Reuters, March 6, 2019. https://www.reuters.com/article/us-oecd-economy/global-economic-growth-forecasts-cut-again-by-oecd-idUSKCN1QN13N

[v] “Global Trade Growth Loses Momentum as Trade Tensions Persist,” Staff, World Trade Organization, April 2, 2019. https://www.wto.org/english/news_e/pres19_e/pr837_e.htm

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today