Personal Wealth Management / Economics

Markets Respond to Price Signals

Rising prices aren’t fun, but more and more companies are responding to price signals and ramping up production.

We have noted before that when markets are allowed to work, high prices are often self-correcting because they invite greater production—raising supply—and limit demand, which stabilizes or tugs prices back down. For example, after lumber prices hit record highs in May, sawmills ripped more boards, while some buyers balked, sending prices down -72.8% through the summer.[i] Though up a bit lately, they remain -53.8% off their May peak.[ii] We see this same dynamic playing out in myriad other areas. Let us take a tour.

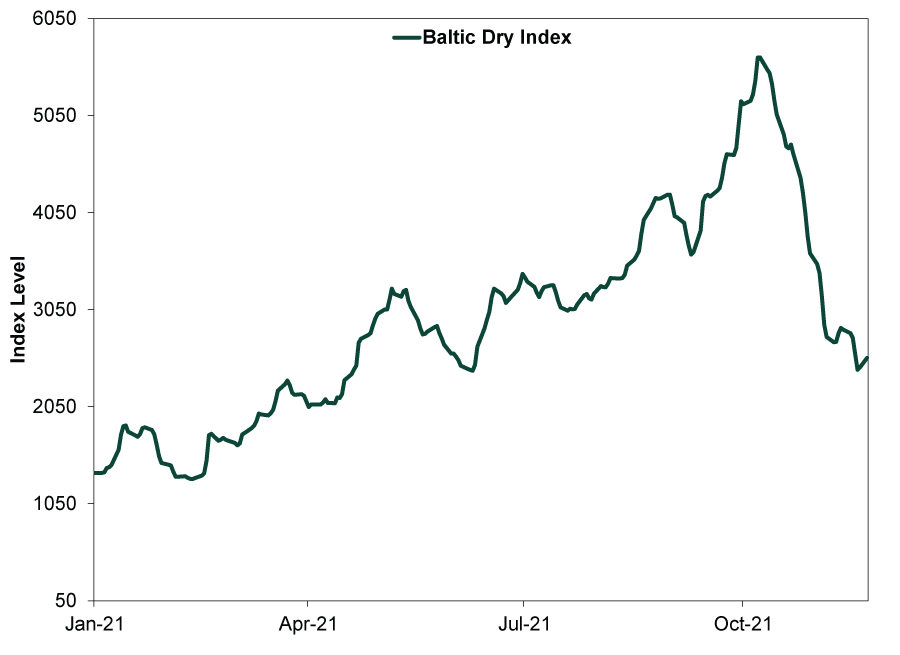

Shipping backlogs? The Baltic Dry Index—a measure of bulk goods’ (like coal and steel) transport costs—hit a 13-year high in October, but it has since tumbled -53.2% as global port congestion eases.[iii]

Exhibit 1: Transport Costs Climb Down

Source: FactSet, as of 11/23/2021. Baltic Dry Index, 1/1/2021 – 11/22/2021.

Container shipping rates remain near record highs, but that is incentivizing companies (and ports) to move freight faster—unclogging terminals—and rates are moving lower.[iv] With 71 ships idling in San Pedro Bay off the Ports of Los Angeles and Long Beach last Friday (down from a peak of 86 a few days before), there is still a lot of cargo to unload.[v] But port operators say that is speeding up with sweeper ships on the way to clear empties and further decongest. Container backlogs have fallen about a quarter over the last month.[vi]

Now, these Southern California ports are just a couple links in the global supply chain. Elsewhere, mudslides have severed rail lines to the Port of Vancouver, threatening a major shipping artery from Canada to Asian markets. But trade finds a way. There are multiple smaller North American ports clamoring for business; shippers can reroute their cargoes accordingly.[vii] Maine’s Port of Portland is moving record volumes, for instance.[viii]

The energy crunch is also softening. Record-high European natural gas prices? Politics may be at play—particularly regarding Russian gas delivery—so a direct supply response looks elusive as long as the Nord Stream 2 pipeline stays in regulatory limbo. But this is prompting substitution effects—another way to limit demand, while boosting energy supply in adjacent markets. China has ramped coal production, tanking prices globally after October’s spike. Now coal-fired electricity generation on the Continent is booming. Coal is headed toward meeting 15% of European power demand from less than 10% in Q1 2021, helping reduce reliance on gas—and Russia.[ix]

Oil prices near seven-year highs? Shale drillers are stepping up. This has total US production approaching 12 million barrels per day (bpd), within spitting distance of its pre-pandemic 13 million bpd record high.[x] Global Energy capex is projected to rise 10% next year.[xi] Meanwhile, President Joe Biden just opened up the Gulf of Mexico to record amounts of new drilling, reversing his “day one” decision to halt oil and gas permits on public lands and waters.[xii]

It takes longer for new semiconductor investments to bear fruit, but even there, we are seeing short- and long-term progress. Some car companies that idled plants have restarted production, saying chip supplies have improved.[xiii] Car inventories remain tight, but they are starting to rise.[xiv] Looking further out, two big US automakers just announced strategic partnerships with chipmakers to ensure future supplies.[xv]

Aluminum prices, near record highs in October, have backed off -16.6% as producers moved to expand output.[xvi] Copper is also down -8.7% from its recent peak for similar reasons.[xvii]

Coffee at record highs? Drought in Brazil, too much rain in Colombia and civil war in Ethiopia have constrained the world’s top-producing Arabica suppliers. As long-term contracts reprice, that could spike a cup of joe’s price this winter, but the crop situation for 2022 is looking better.[xviii]

You may have noticed chicken prices are up. This is due in part to labor shortages, which you may have also heard about.[xix] But slaughterhouses aren’t sitting still. Even as they have improved staffing levels, processors are also investing in automation.[xx]

Not all meat has risen—pigs haven’t flown. After rising to near record highs in June, lean hog prices have fallen -31.7%.[xxi] This was due to a pig glut in China, after a shortage there subsequently led to excess production—a reminder how these things tend to move in cycles.[xxii]

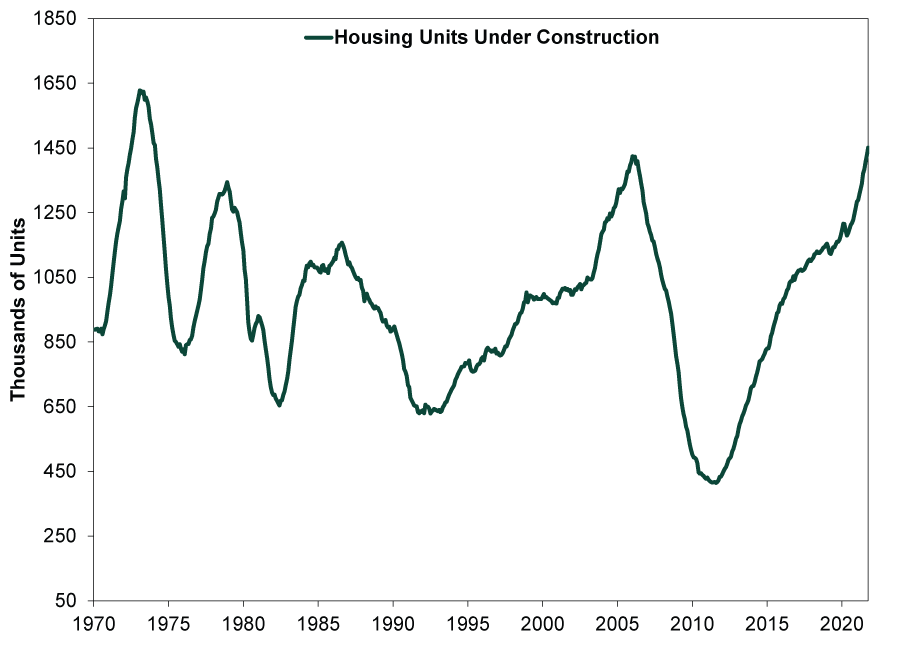

Last, but not least, what to make of record high home prices? Home builders have an answer: New housing under construction is the highest in almost 50 years.

Exhibit 2: Building Boom

Source: Federal Reserve Bank of St. Louis, as of 11/23/2021. Total new privately owned housing units under construction, January 1970 – October 2021.

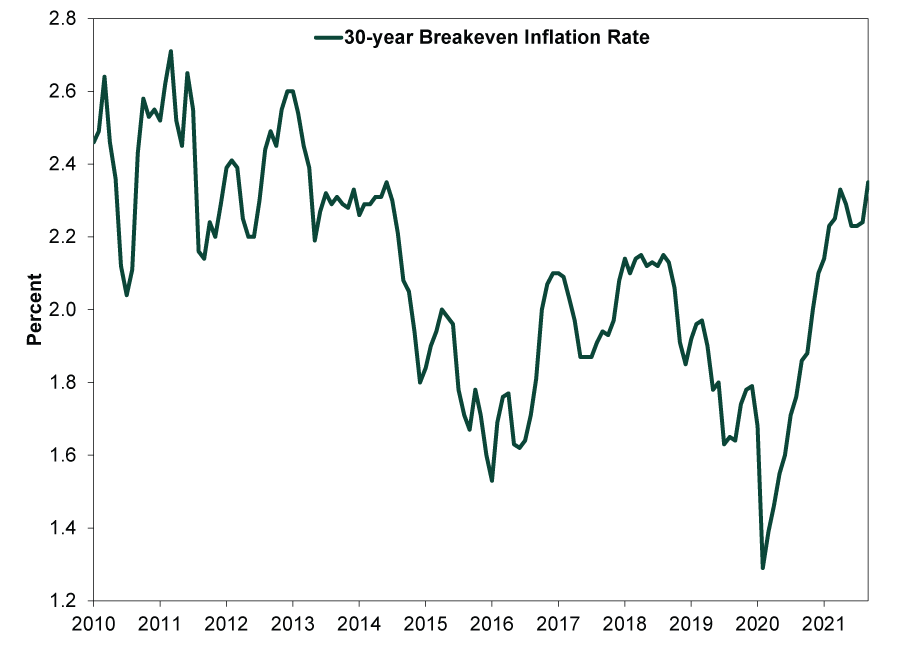

Supply-side reactions to price signals don’t usually have an immediate effect—they take time. But as supply (and demand) adjust, which you can see if you dig a bit, it is a good indication that today’s price pressures are temporary, not the start of a lasting spiral so many headlines warn about. We think this is a big reason why the bond market, which is most sensitive to inflation and inflation expectations, isn’t ringing alarm bells. Yes, implied 30-year breakeven inflation expectations are elevated. (That is, the difference between 30-year Treasury and Treasury inflation-protected security yields, which represents the market’s expectation for the average inflation rate over the next 30 years.) They just hit their highest level in seven years. But that level happens to be just under 2.4%.[xxiii] Historically low 30-year Treasury yields, which are near pre-pandemic levels at 1.9%, indicate a return to normal—not panic, in our view.[xxiv] If a 1970s replay was commencing, bond yields would probably be rising a lot more.[xxv] They aren’t.

Exhibit 3: Long-Term Inflation Expectations in Check

Source: Federal Reserve Bank of St. Louis, as of 11/23/2021. 30-year breakeven inflation rate, February 2010 – October 2021.

[i] Source: FactSet, as of 11/23/2021. Lumber price per board feet, 5/7/2021 – 8/19/2021.

[ii] Ibid. Lumber price per board feet, 5/7/2021 – 11/22/2021.

[iii] Ibid. Baltic Dry Index, 10/7/2021 – 11/22/2021.

[iv] “The U.S. Supply-Chain Crisis Is Already Easing,” Brooke Sutherland, Bloomberg, 11/18/2021.

[v] “Supply-Chain Problems Show Signs of Easing,” Stella Yifan Xie, Jon Emont and Alistair MacDonald, The Wall Street Journal, 11/21/2021.

[vi] “Container Logjam Eases as L.A. Port Threatens Penalties,” Michael Sasso, Bloomberg, 11/16/2021.

[vii] “Smaller U.S. Ports Pitch for Cargo as California’s Logjams Swell,” Augusta Saraiva, Bloomberg, 11/5/2021.

[viii] “With Other Cargo Ports in Chaos, Portland’s Is Sailing Toward a Record-Breaking Year,” Peter McGuire, Portland Press Herald, 11/13/2021.

[ix] “Big Winners From Natural-Gas Crunch: Coal Power Plants in Europe,” Joe Wallace, The Wall Street Journal, 11/17/2021.

[x] Source: EIA, as of 11/23/2021. Weekly US field production of crude oil, 2/21/2020 – 11/12/2021.

[xi] Source: Fisher Investments Research and company filings, as of 11/19/2021.

[xii] “U.S. Holds Historic Oil and Gas Lease Sale in Gulf of Mexico Days After Climate Summit,” Emma Newburger, CNBC, 11/17/2021.

[xiii] “Supply Chain Crisis Shows Signs of Gradually Easing,” Neal Freyman, Morning Brew, 11/17/2021.

[xiv] “U.S. October Car Sales and Inventories Rise, but Don’t Call It a Comeback,” Claudia Assis, MarketWatch, 11/3/2021.

[xv] “Ford and GM Are Getting Into Chip Development to Help Deal With the Shortage,” Jasmine Hicks, The Verge, 11/18/2021.

[xvi] Source: FactSet, as of 11/23/2021. Aluminum price per ton, 10/18/2021 – 11/22/2021.

[xvii] Ibid. Copper price per ton, 10/19/2021 – 11/22/2021.

[xviii] “Brazil’s Coffee Crop Expected to Rebound After Above-Average Rain,” Marvin G. Perez, Bloomberg, 11/5/2021.

[xix] “Tyson Foods Raises Meat Prices as Costs Escalate,” Jacob Bunge and Matt Grossman, The Wall Street Journal, 11/15/2021.

[xx] “Tyson Turns to Robot Butchers, Spurred by Coronavirus Outbreaks,” Jacob Bunge and Jesse Newman, The Wall Street Journal, 7/9/2020.

[xxi] Source: FactSet, as of 11/23/2021. Lean hog price per pound, 6/9/2021 – 11/22/2021.

[xxii] “CME Lean Hog Futures Slip Amid Export Demand Doubts,” P.J. Huffstutter, Reuters, 11/2/2021.

[xxiii] Implied 30-year Inflation expectations of 1.3% in March 2020 were probably an overreaction, highlighting how this indicator can be sentiment driven, so we wouldn’t take its projections as gospel. But given its relatively narrow range over the last decade, we think it is safe to say it isn’t currently pricing anything out of the ordinary.

[xxiv] Source: Federal Reserve Bank of St. Louis, as of 11/23/2021. 30-year Treasury yield, 11/19/2021.

[xxv] Or if rising debt loads were getting out of hand or hitting the debt ceiling was a problem or, or, or.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today