Personal Wealth Management / Market Analysis

Meet the New Reserve Currency

Stocks aren't bothered by the yuan's admission to the IMF's reserve currency basket-investors shouldn't be either.

On Saturday, the Chinese yuan finally joined the euro, dollar, yen and pound in the International Monetary Fund's (figurative) basket of reserve currencies. In the past, this might have sparked a range of feverish concerns-that foreign governments will demand fewer dollars, US assets will fall in value and interest rates on US debt will surge. For years, many have fretted a veritable economic cataclysm in which the fiat greenback house of cards collapses at long last, with the ascendant yuan emerging triumphant in its place. This time, not so much, suggesting this long-in-the-tooth fear could be receding-a sensible development, in our view. The yuan's designation as a reserve currency is a non-event-it has zero effect on the dollar's value, is unlikely to affect US interest rates materially and has no relevance for stocks today.

Let's first sort through some jargon. The IMF's "currency basket" refers to the composition of "Special Drawing Rights" (or SDRs): accounting units backed by currencies-the US dollar, Japanese yen, British pound, euro and now Chinese yuan-without any value on their own.[i] Countries can draw on their SDR claims for short-term currency stabilization purposes, or borrow them in an economic pinch (Greece, anyone?). For these reasons, the IMF needs SDR currencies to be easily tradeable, responsibly managed and extremely liquid. (Notice, by the way, that the currency basket is not "the official collection of approved currencies for global trade"-more on this later.) So, why now[ii] for the yuan? Because it trades more freely than before, foreign investment controls are looser and capital controls are less stringent. Note the comparative language-the Chinese government has moved slowly in each of these areas and there is still much to do, as evidenced by the yuan's negligible use in international trade.

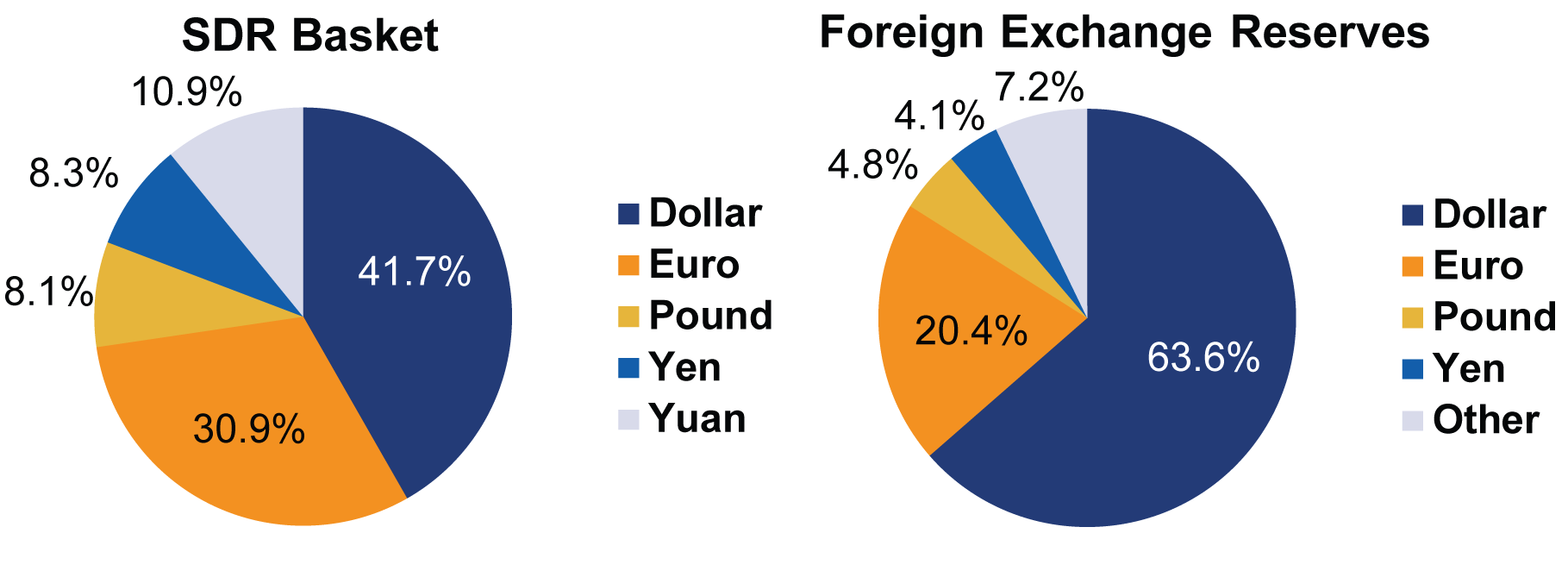

But, you may say, that was before the IMF initiated the yuan into its Elite Currency Honor Society[iii]-won't that catapult it into prominence, leading global central banks to stockpile yuan instead of dollars in their foreign exchange reserves? There is an easy way to check: Compare SDR composition to actual foreign exchange reserves.

Exhibit 1 - Special Drawing Rights vs Foreign Exchange Reserves

Source: IMF, as of 9/30/2016

Those pie charts aren't close to identical. Note, for example, that the yen's share in the IMF's basket is 8.3%, but just 4.1% in countries' foreign exchange hoards.[iv] And that "other" includes Canadian and Aussie dollars, the Swiss franc and, um, others as well as the yuan. Countries want similar currency qualities as the IMF-liquidity, free capital movement and market depth-and importantly, the IMF doesn't tell them what to hold in their reserves! If they want to hold dollars, they'll do so. Pounds? Sure! The Malaysian ringgit or Angolan kwanza? Why not?[v] We wouldn't be shocked to see more interest in the yuan now, but the impact is likely A) marginal, B) gradual, and C) dependent on more capital-freeing reforms. Besides, China doesn't even issue nearly enough debt to fill reserve demand, with only $1.6 trillion in outstanding central government debt as of Q2. Foreign ownership is still limited as well. The US, on the other hand, issues plenty, so countries are able to hold a lot. Simple as that.[vi]

But let's explore further: What if the world's central banks were champing at the bit, eager to swap out reserve dollars for yuan at the crack of dawn on Saturday?[vii] Might this slash the dollar's value? Still no, because countries' reserve holdings don't materially influence the value of currencies or demand for assets. Folks have feared a Chinese selloff of US Treasurys for ages-but though China has been selling Treasurys for at least a year, yields have stayed near record lows. At the same time, the dollar's share of foreign reserves is actually rising. Ultimately, national demand for currency reserves just isn't a big interest rate driver-foreign government ownership of US debt stands at about 30% of the total, and private demand (for trade and investment purposes) makes up the rest.[viii] This makes sense: As noted above, the IMF and central banks prefer stable, liquid currencies-and so do multinational companies. Hence, nearly half of all global payments take place in dollars, against a shade under 2% for the yuan.

The yuan's admission to the IMF's currency basket is old news anyhow-the IMF announced the exact date it would take effect in November 2015. The press covered it extensively. Hungary bizarrely threatened to flip all its forex holdings to yuan.[ix] Markets price in such changes before they take effect-and in market time, 10.5 months is eons. Nothing has changed since the announcement: US debt didn't grow unaffordable, dollar-denominated assets didn't plummet and the yuan is still a bit player in international commerce. Stocks have long since put this fear to rest-investors should follow suit.

[i] This makes them a poor candidate for some sort of alternative global currency that would gradually displace existing monies, as some fear.

[ii] Well, actually "why last November," as that's when the IMF made the decision.

[iii] We don't think this is any odder a label than "currency basket."

[iv] Also relevant: Every central bank has known the yuan will be In the Basket on October 1 for nigh-on a year, and could have beefed up reserve holdings in anticipation. Yet the yuan doesn't even register here.

[v] Anything goes in the wild world of national foreign exchange reserves.

[vi] Incidentally, if you're worried about the decline of the dollar, odds are you wouldn't be a fan of the sort of deficit spending spree that would push foreign dollar reserves way higher. The two go together.

[vii] Which is nonsense-see footnote iv.

[ix] It may be worth noting Hungary only has about $30 billion in total foreign reserves and doesn't rank on the Treasury's list of Major Foreign Holders of US debt, which is 36 nations/regions deep.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today