Personal Wealth Management / Market Analysis

MSCI and the Addition of Chinese A-Shares: Big News, Limited Opportunity

Why Chinese A-Shares’ pending addition to the MSCI Emerging Markets Index isn’t a game-changer for global investors.

Following last year’s much ballyhooed announcement, next month MSCI will include Chinese A-shares in its Emerging Markets (MSCI EM) index. If the recent past is any guide, you can probably expect a rerun of the fanfare the original announcement received as the inclusion date nears. But whatever media hype A-shares’ inclusion in the EM gauge receives, this move probably isn’t as monumental as many believe. With a small representation to start—and an uphill battle to increase exposure—Chinese A-shares likely won’t be a meaningful part of the MSCI EM or any broad index for a while. Moreover, such moves lack lasting impact on relative performance, suggesting the inclusion isn’t a huge opportunity for global investors.

First, a bit about structure. China has three share classes: A-shares, which are companies primarily trading on China’s domestic exchanges; B-shares, which are shares trading on domestic exchanges in foreign currencies—by far the rarest; and H-shares, which trade on Hong Kong’s exchange and have been in the MSCI EM a while. For years, China has been pushing MSCI to include A-shares, too, and finally got its wish last summer … to a small degree. In two stages (half in June, half in September), MSCI EM will add just 234 of the roughly 3,000 A-Share companies, eventually making up about 0.8% of the index—a rounding error that pales in comparison to Chinese H-Shares’ roughly 28% weight.[i] I expect A-shares will likely remain a small weight until China’s government further opens up its domestic market.

Why? A-shares might offer some interesting opportunities, but they carry investment risks due to limited investor access and historical government intervention. For example, it is currently possible for global investors to purchase A-shares only through the Qualified Foreign Institutional Investor (QFII) program and two Hong Kong “connect” programs—narrow channels affording foreigners limited access to A-shares since 2002 and 2014, respectively. But QFII limits foreigners’ ability to get invested capital out of China and requires investors be licensed by Chinese regulators. The connect programs have a daily “net buy” quota, which just rose from around $2 billion to $8.3 billion on May 1, limiting inflows. A forthcoming London-based “connect” program will likely have similar quotas. Additionally, the Chinese government has a history of intervening in the A-share market and suspending trading. In 2015, China suspended roughly 50% of total A-shares—including about 15% of the securities expected to be included in the MSCI EM—and for some companies the suspension lasted weeks.

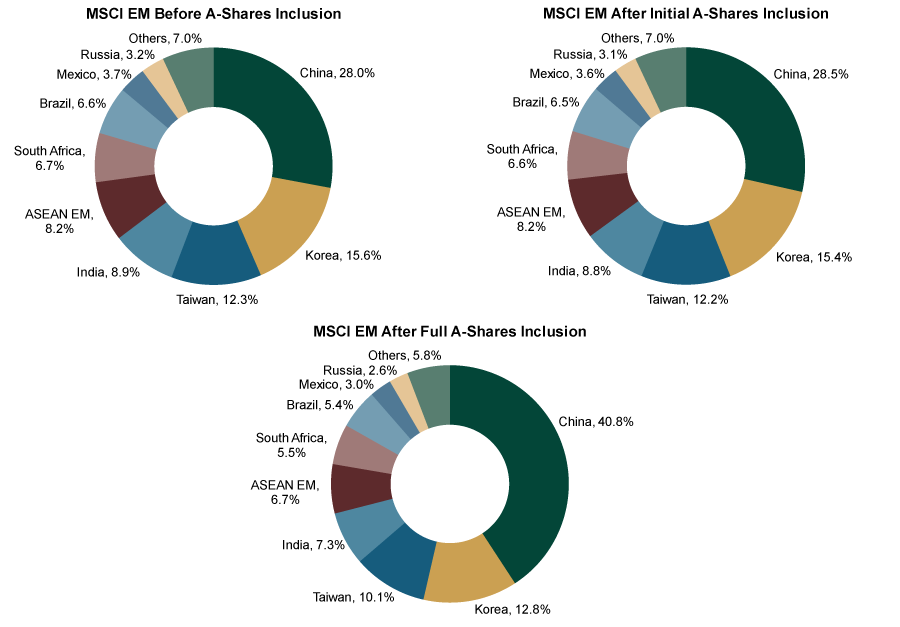

However, China has been trying to open up. If it continues increasing access to local equities and all A-shares get added to the MSCI EM, it could have a big impact—it would just take a while. Estimates suggest if both Chinese A-shares and H-shares are fully included, China’s representation in the MSCI EM will jump to 41%—more than three times the next largest country, South Korea, which would dwindle to around 13%. (Exhibit 1) Active and passive managers would need to meaningfully increase their exposure to China to remain benchmark-like. If history holds, an announcement of this may briefly bump up China’s relative performance, similar to what happened to Pakistan, UAE and Qatar when MSCI announced adding them. However, that isn’t certain, especially considering this could easily be a multi-decade process, mitigating market impact. Taiwan and South Korea started with fewer capital controls and higher percentages of their stock markets’ capitalization being added (~40%) initially, and their full inclusions in the MSCI EM took 10 years. Given the Chinese government’s slow approach to opening capital markets, A-shares likely see a lengthier process.

Finally, that sentiment impact is on the announcement, not the inclusion. Markets pre-price these things near instantly, so by the time inclusion happens, the effect is likely gone. Hence, the actual inclusion of Pakistan’s markets and others has typically accompanied underperformance, not outperformance.

Exhibit 1: Potential Index Inclusion Roadmap for Chinese A-Shares

Source: FactSet, as of 6/19/2017. MSCI EM index constituents before Chinese A-share inclusion, after 2018’s planned inclusion and if all A-Shares were added, based on market capitalization and MSCI estimates on 6/19/2017.

While the inclusion of A-shares does represent progress for Chinese equity markets, it is a baby step—and unlikely to mean much for returns in the here-and-now. Full inclusion could take decades and is dependent on the removal of capital controls by the Chinese government, a historically slow process. More importantly, the category as a whole comes with additional risks and tends to be smaller in capitalization and lower quality, characteristics that typically tend to underperform at this point in the market cycle.

Note: This article was updated on May 15, 2018 to reflect MSCI's final figures after they announced the list of Chinese A-Shares that will be added to the MSCI EM index. The second paragraph originally referenced 222 companies making up 0.7% of the MSCI EM index.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today