Personal Wealth Management / Market Analysis

Chinese Stocks’ Symbolic Emergence

The addition of some Chinese stocks to a popular Emerging Markets index doesn't make China a better choice for investors.

Last Tuesday, China received the news it has awaited for four years: MSCI, a prominent index provider, will include mainland Chinese stocks known as A-shares in its Emerging Markets (EM) Index starting in May 2018-a move some declared a "huge vote of confidence," a "breakthrough" that will unleash a "wave of foreign investment." Perhaps, one day, we'll all look back at this as the first major milestone on China's long road to financial openness. However, let's not overstate the case now. The change was mostly symbolic, and it doesn't render China a more (or less) attractive investment destination.

While Chinese stocks have been in the MSCI EM Index for over two decades, mainland China mostly hasn't. Because of China's capital controls, big Chinese companies have three main share classes: H-shares (traded in Hong Kong), A-shares (traded in Shanghai and Shenzhen) and B-shares (traded in foreign currency in Shanghai and Shenzhen, and far less common). Foreigners can easily access H-shares, but the government restricts access to A-shares, so MSCI included only H-shares and B-shares in its EM Index. Since there are only 222 H-shares (with a market cap of $762 billion) versus 3261 A-shares (with a market cap around $7 trillion), many see A-shares' inclusion as a big deal for all managers and index funds benchmarked against the MSCI EM.

China sees it as a big deal, too, hoping mainland shares' inclusion will attract a flood of capital from fund managers and institutional investors with MSCI EM-based mandates-hence their years-long lobbying effort. Until now, MSCI declined, citing restrictions on investment, regulators' tendency to arbitrarily halt trading of volatile stocks for long stretches, and rules limiting index funds' stock sales. But now it seems China has done enough to win MSCI's blessing.

Yet the change is scarcely noticeable. MSCI will add only 222 A-shares-not the whole kit and caboodle. China was already 28% of the MSCI EM Index; after the change takes effect, it will rise to 28.73%. MSCI is starting small because Chinese markets are still fairly restricted. Pilot programs have improved foreign investors' access to A-shares, but they have strict caps, and lengthy trading suspensions are also still common. Trading in about 8% of A-shares was halted as of May, and MSCI has to add A-shares in two stages next year (May and August) to get around "daily trading limits."

The move's small scope is one reason we don't expect a huge boost for A-shares. The simple fact that index reclassifications usually don't have a meaningful impact is another. MSCI moves slowly, announcing its decisions a year before they take effect, giving markets plenty of time to price in the change before index funds start buying. Markets discount all widely known information, and MSCI's move is widely known.

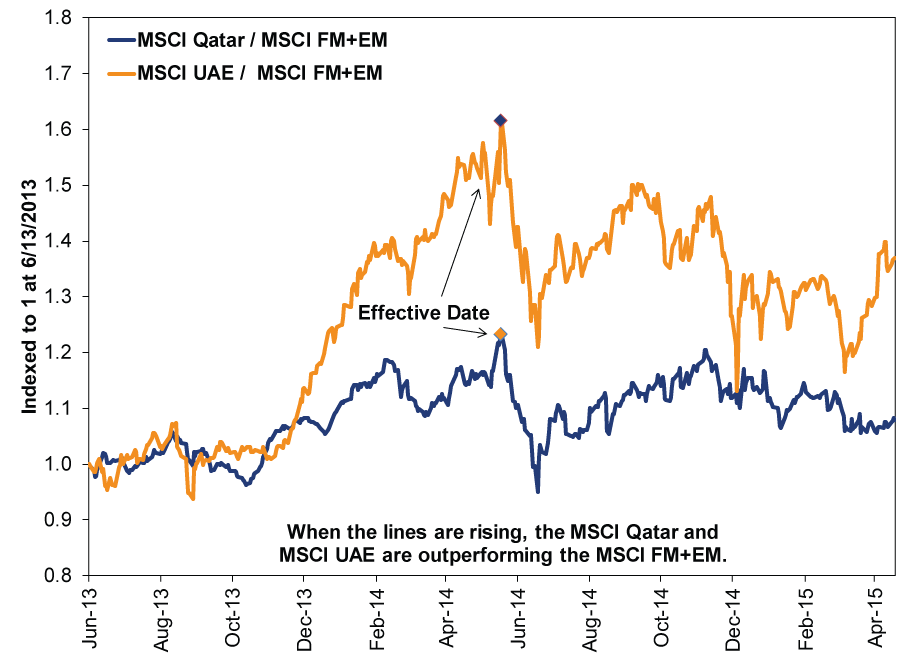

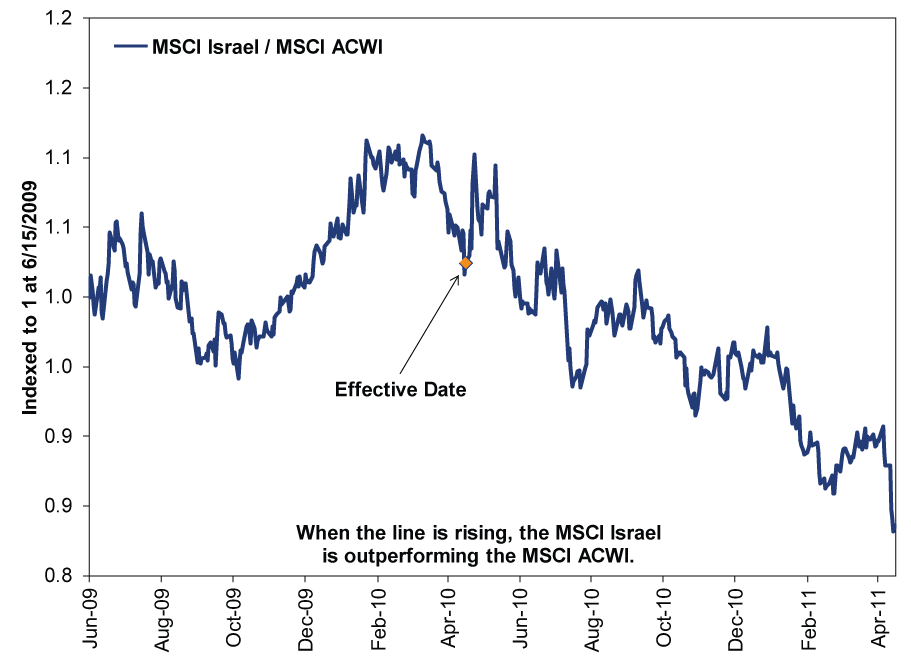

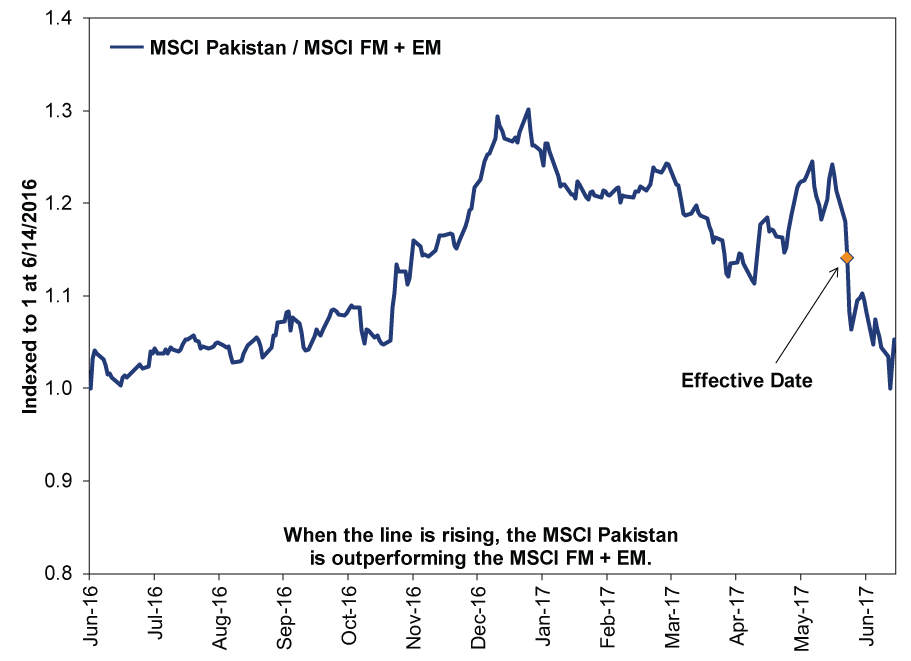

History vets this out. MSCI announced the UAE and Qatar's upgrade from Frontier to Emerging markets in June 2013. Between then and May 2014, when the change took effect, both outperformed the MSCI Frontier Emerging Markets Index, which combines their past and present benchmarks. But after the reclassification went live, they lagged. Israel, tapped for an upgrade to Developed in 2009 and officially added to the MSCI World Index in 2010, led the MSCI All Country World Index (which includes Emerging Markets and developed countries) before the effective date and lagged after. Recent MSCI EM inductee Pakistan has so far followed a similar course, outperforming the MSCI Frontier Emerging Markets Index after MSCI announced the upgrade on June 14, 2016, but lagging since the change took effect a few weeks ago.

All this suggests investors tend to bid up shares in upgraded countries before they're in new indexes, front-running the index funds. However, as Exhibits 1-3 show, this isn't a timing tool. Reclassified countries don't uniformly start outperforming as soon as MSCI announces its decision, lead all the way until the change takes effect, then lag. It's much more nuanced, and the timing of their leadership shifts is inconsistent. That's quite logical when you consider that forthcoming index changes are only one variable influencing demand-and a small one at that. This is a big reason MSCI's A-share announcement isn't a reason to load up on Chinese companies now to front-run the change. Political and regulatory risks persist, and most A-shares tend to be lower-quality and more value-oriented, which tend to underperform in maturing bull markets.

Exhibit 1: MSCI UAE and MSCI Qatar vs MSCI Frontier Emerging Markets

Source: FactSet, as of 6/23/2017. MSCI UAE, MSCI Qatar and MSCI Frontier Emerging Market Index returns with net dividends, 6/13/2013 - 4/30/2015.

Exhibit 2: MSCI Israel vs MSCI All Country World Index

Source: FactSet, as of 6/23/2017. MSCI Israel and MSCI All Country World Index returns with net dividends, 6/15/2009 - 4/30/2011.

Exhibit 3: MSCI Pakistan vs MSCI Frontier Emerging Markets

Source: FactSet, as of 6/23/2017. MSCI Pakistan and MSCI Frontier Emerging Market Index returns with net dividends, 6/14/2016 - 6/22/2017.

More fundamentally, the idea that more index funds purchasing mainland stocks will boost returns misunderstands how markets work. In an auction marketplace, price movement isn't a function of the number of buyers. It is a function of buyers' willingness to pay up. Besides, the scope here is so tiny that even if you do think adding participants matters, you aren't talking about much more buying.

EM classification is no game-changer for China's long-term outlook, either. MSCI's decision is backward-looking-a reaction to (mostly incremental) reforms markets already knew about. Our coverage of some of these events is years old, as you'll see here, here and here. Might China keep liberalizing and become a major financial hub several years down the line? We won't rule it out, but speculation about the distant future isn't a reason to pile into A-shares today. China still has a strong economy with growing investment opportunities, but EM classification doesn't alter the backdrop.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today