Personal Wealth Management / Market Analysis

China Devalues the Yuan

The yuan's depreciation doesn't spell doom for the world.

On Tuesday, China's yuan suffered its biggest one-day drop in 20 years as the central bank sort of stopped propping up the exchange rate , surprising the world and knocking global markets. Volatility continued into Wednesday as headlines pondered the potential motivation and ramifications. Some speculated China is desperate to boost growth and out of stimulus tricks, leaving officials no choice but to devalue the currency and hope for an export boost. Many fear it will knock America and Europe by hurting multinationals' Chinese sales or complicate the Fed's rate hike plans by "exporting deflation."

As ever, a little perspective is in order. A -1.9% one-day drop is hardly big. It is abnormal in China's tightly controlled markets, but for most countries, it would be considered normal volatility. It isn't like officials slashed a third of the yuan's value to undercut competitors, and most Chinese economic indicators confirm such a move would be wholly unnecessary. Nor should a slightly weaker yuan disrupt trade flows globally or cause a dreaded "currency war." China is simply moving to a somewhat more market-oriented system. Volatility might continue as markets try to determine just how hands-on China will be from now on, but the shift isn't a sweeping fundamental change for global stocks.

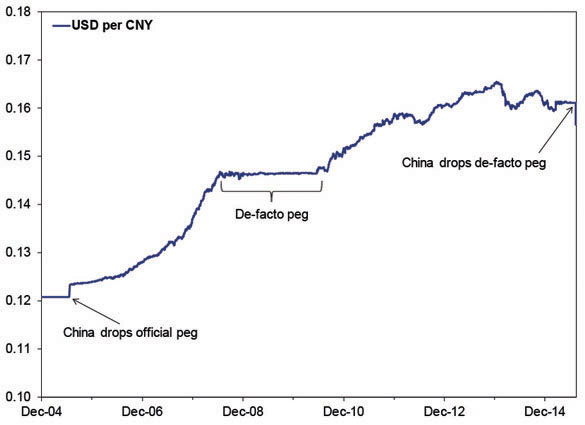

Since 2005, China has officially used a managed float against a basket of currencies, setting a daily reference rate for the yuan and allowing it to trade within a 2% bandwidth (in either direction). The next day, they'd set a new rate that may or may not have anything to do with the prior day's movement. Practically, officials have used this system to manage the RMB/USD exchange rate. From 2005 to mid-2008, they allowed the yuan to strengthen against the dollar, then held the rate steady until mid-2010. It then appreciated on and off through early 2014, depreciated intermittently through mid-March 2015, then appeared to peg back to the dollar in mid-March. (Exhibit 1)

Exhibit 1: US Dollar per Chinese Yuan, 12/31/2004 - 8/12/2015

Source: FactSet, as of 8/13/2015.

Now, they're injecting somewhat more transparent methodology, basing the daily fixing rate on the prior day's closing price and market makers' quotes. Though the 2% up-or-down trading bandwidth will remain and the system leaves some room for arbitrary meddling, it is nevertheless more market-based. To prepare for the change, the PBOC set Tuesday's yuan-to-dollar reference rate at 6.1162, almost 2% below Monday's close as a "one-off" adjustment, basically acknowledging the official exchange rate was substantially higher than the market-set rate. To most studied observers, that went without saying, considering the yuan was pegged to a strong dollar while China experienced capital outflows. In a free market, those outflows would have dropped the currency value.

This is sort of the inverse of what Switzerland did in January, removing its artificial ceiling on the franc's value relative to the euro and ending its efforts to prevent massive capital inflows from strengthening the currency. While the Swiss franc strengthened almost right away (13% against the euro in one day), China's 2% bandwidth prevents similar volatility. Many expect the exchange rate to weaken further under the new system and slowly catch up with fundamentals, presuming the central bank is tired of digging into forex reserves to prop the yuan. The PBOC set Wednesday and Thursday's reference rates at levels more or less consistent with the prior day's closing, and the yuan traded lower both days before mysteriously gaining 0.2% in the final minutes of trading-evidence of continued intervention, most believe. At a rare press conference Thursday, PBOC Assistant Governor Zhang Xiaohui said the devaluation is "basically already completed," and Vice Governor[i] Yi Gang said the bank will intervene if "volatility is excessive." Their jawboning seemed intended to talk the yuan up, not down.

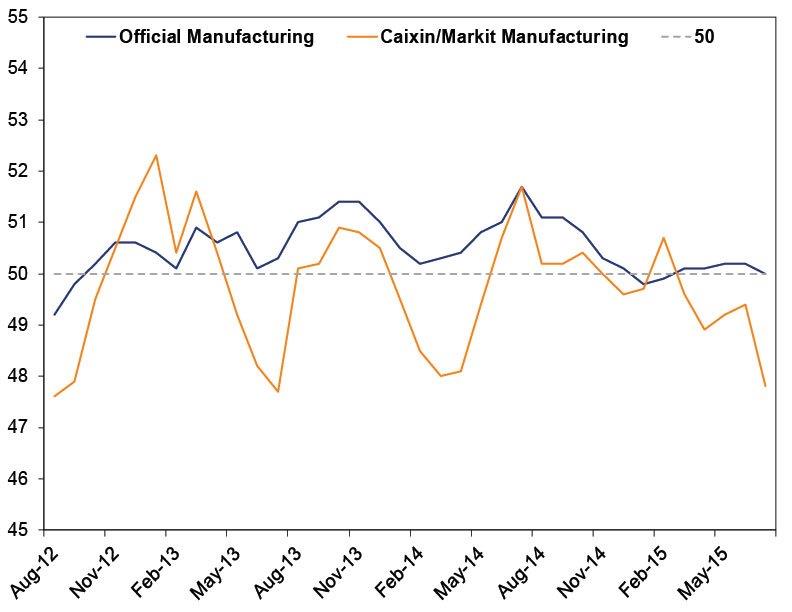

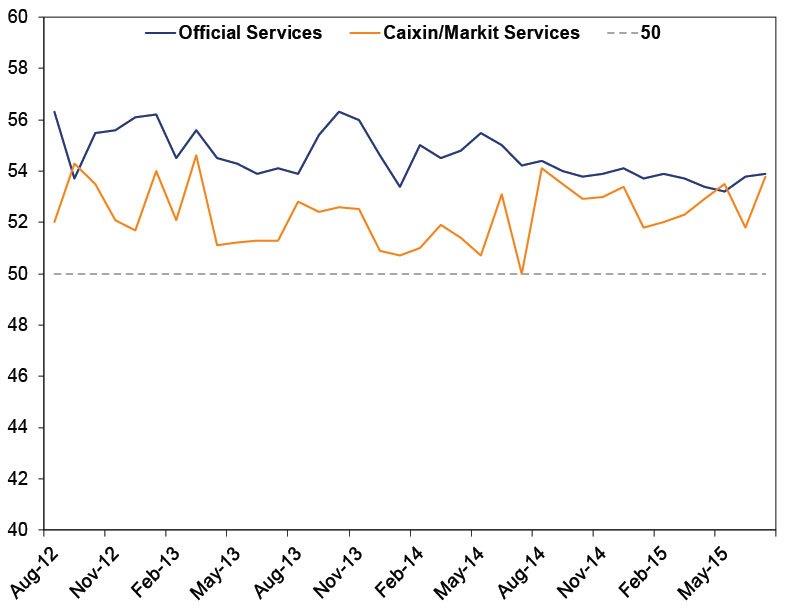

Considering all this, and the fact the yuan is down only around 3% since Monday, it seems a pretty big stretch to interpret the move as a sign of economic desperation. Though we always take this stuff with a grain of salt, Yi called rumors China wants a big devaluation to help exports and boost growth "nonsense" at Thursday's presser. Nor is there evidence China needs a big boost, export-oriented or otherwise. As scary as July's -8.3% y/y export decline seems, exports declined just -0.6% y/y through 2015's first seven months versus the same period in 2014-down a tad, not off a cliff. And considering China wants to rely less on business investment and exports and more on services and consumption, the lower number isn't a surprise. The purchasing managers' indexes (PMIs) for China not only highlight this ongoing shift, the most recent readings suggest businesses are right in their long-term trend. (Exhibits 2-3)

Exhibit 2: China Manufacturing PMI Since August 2012

Source: FactSet and Bloomberg, as of 8/12/2015. Readings over 50 indicate expansion.

Exhibit 3: China Services PMI Since August 2012

Source: FactSet and Bloomberg, as of 8/12/2015. Readings over 50 indicate expansion.

Other recent Chinese data confirm long-term economic trends remain intact, too. July industrial production rose 6.0% y/y and retail sales were up 10.5% y/y-both slightly lower than June's figures (6.8% and 10.6%, respectively) but not wildly off, either. Similarly, from January - July 2015, fixed asset investment and property investment were up 11.2% and 4.3% y/y, respectively, reflecting these categories' steadily declining growth rates. Nothing here suggests China's economic reality has wildly diverged into unexpected territory. Some posit the big recent drops in China's domestic "A-share" equity markets portend upcoming economic trouble. However, stocks are only reliable forward-looking indicators in liquid and open markets-China's aren't. Consider: Chinese domestic stocks have endured over 10 bear markets in the past 25 years . Compare that to the S&P 500's two since the Shanghai Index opened December 19, 1990.

Competitive devaluation-i.e., currency war-chatter seems wide of the mark to us, too. The PBOC is (officially) intervening less here and allowing more market influence, which goes against the whole "deliberate intervention" part of the currency war theory. As does that propping on Wednesday and Thursday. Plus, we don't see much urgency elsewhere to depreciate. Currency war theory says a weaker yuan would undercut Korea, one of China's direct export competitors. Yet South Korea's finance minister pointed out recently that his country exports a ton to China-China is South Korea's biggest trading partner-and said if a weaker yuan boosted Chinese growth, it would benefit Korea. As for the US, well, America did fine in 2012, when the yuan/dollar exchange rate matched today's. And though Mexico competes directly with China, the peso has already weakened significantly. So has Vietnam's currency. We just don't see a there there.

Overall, we suspect markets are overreacting to a procedural move-and one that is probably a long-term positive for China, as it injects more market forces into its economy. The IMF sort of agrees, though only time will tell how this impacts China's quest to join its Special Drawing Rights currency basket. (A debate of little importance beyond symbolism anyway.) For investors, however, we suggest looking past all the theories and speculations and focusing on the facts: Nothing in China has radically changed to the point of worry. While market bumpiness may persist because of new worries about China, Greece or even no reason at all, remember positive volatility can come just as quickly as negative volatility. During bull markets, the positive volatility is much more frequent, but to benefit from it, long-term investors must remain disciplined and ride through the rough patches, too.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today