Personal Wealth Management / Market Analysis

Musings on Volatility

Markets haven’t moved a ton lately, but that doesn’t mean we’re witnessing “the death of volatility.”

US stocks took their biggest daily drop in weeks Thursday, with the S&P 500 dropping a bit less than 1% and the Russell 2000 inching toward correction territory. Headlines speculate over whether broader markets will follow the Russell, but there is no way to know—short-term moves are impossible to predict. Corrections can start any time, for any reason (or no reason!) and usually come without warning. But if stocks do pull back from here, it would be the latest instance of markets humiliating those who utter those four little, dangerous words: It’s different this time.

Just two days ago, all seemed well. The S&P and MSCI World indexes closed at record highs Monday and Tuesday. Broader markets seemed immune to the ongoing wobbles in so-called momentum stocks. And several pundits noticed a trend: Some arbitrary measures of volatility were eerily calm. The CBOE’s VIX—a measure of expected S&P 500 volatility based on options transactions—was down from 2014’s start and far below its long-term average. Options volatility in some commodities, currencies and Treasurys was down, too. Observers started eyeing things like “a return to market tranquility.” Many were of “the view that volatility will stay low” as we enter “a period of widespread complacency.” Just for good measure, one Wall Street strategist said, “Current risk pricing in US equities seems to point to something being ‘different’ this time.” That last bit was printed under the headline, “The Death of Volatility?” first thing Thursday morning.

Is it any wonder stocks took a wee turn?

Now, this is all just coincidence—not a trigger, not a cause. Just ironic timing. Markets didn’t wobble because some high-profile pundits said “all quiet on the equity front.” But the whole episode illustrates a key point: Trying to predict volatility is just plain pointless. We aren’t aware of anyone with a public record of precisely and repeatedly predicting short-term moves—the beginning (and ending) of pullbacks or corrections (generally considered a quick drop of 10% or greater over a few weeks or months). All the supposed indicators, like the VIX, are hogwash. They tell you what has happened, not what will happen. Volatility doesn’t predict volatility any more than past returns predict future performance.

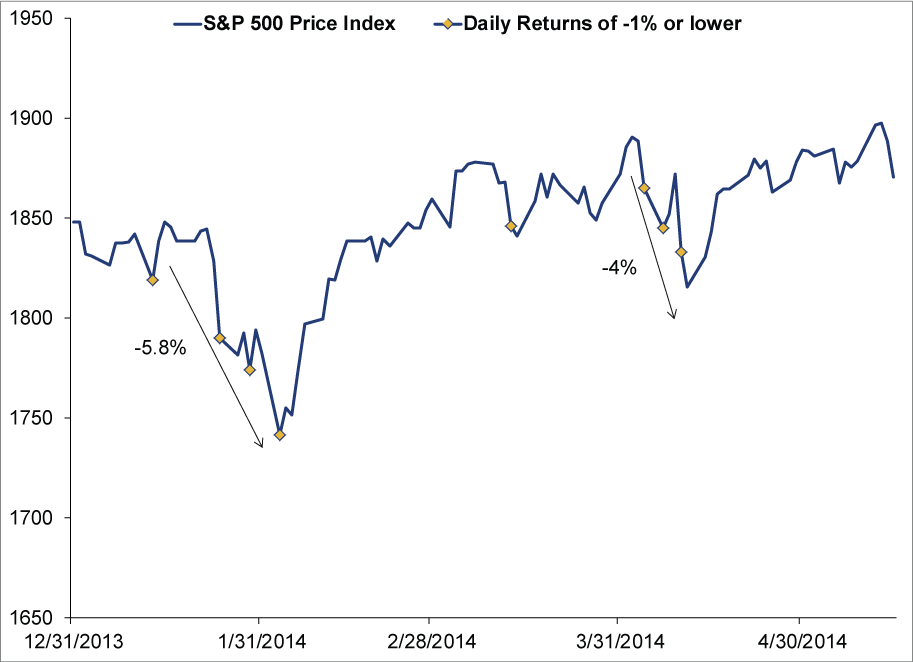

The funny thing about all this is, you don’t need to look at the VIX, gold options or other contracts to see markets have been calm lately. All you have to do is look at stocks themselves—nothing fancy! Exhibit 1 shows the S&P 500 Price Return Index year to date. There are only eight days with returns of -1% or lower, as of Thursday’s close. That’s one per every 12 trading days—much more seldom than the average of one per every 8.2 trading days from 12/31/1982-12/31/2013. Another eight days have gone up 1% or more—also low. Of the 345 complete quarters since 1927, only 39 had flatter returns than Q1 2014. Cumulative year-to-date price return is only 1.2%, and the index has traded in a narrow range—the “big” pullbacks were -5.8% from January 15 to February 3 and -4% from April 2 to April 11. To many, this all feels hugely volatile—as Nobel Prizewinning economist Daniel Kahnemann theorized, humans tend to magnify the pain of losses. But these past four and a half months have been relatively calm.

Exhibit 1: S&P 500 Price Index

Source: FactSet, as of 5/15/2014. S&P 500 Price Index, 12/31/2013-05/15/2014.

If you’re a long-term growth investor, what you want from here is simple, but counter-intuitive: more volatility! When most people think about volatility, they think downside, but volatility just means movement. Stocks can’t go up if they don’t move. Yes, with more movement probably come more occasional dips and dives, too—that’s just the nature of markets. But riding these ups and downs is the tradeoff for getting long-term returns.

No one can predict when market movement will pick up—or whether (make that, when) we’ll see a bigger pullback or correction in the process. Maybe we will! But maybe not. Corrections don’t occur at regular intervals. There is no law saying if markets go an above-average span without a correction, you’re due. And if stocks bounce around a bit after hitting all-time highs, nothing says they have to go down more before they go up. Anyone who tells you otherwise is using methods with zero real predictive power, like charts, moving averages, mean reversion analyses and other technical mumbo jumbo. They might cite patterns, but patterns are just interesting observations—coincidence without causation.

Our advice to long-term growth investors: Tune out the noise. None of it matters. If meeting your financial goals requires getting equity-like growth over time for some or all or your portfolio, then participating in bull markets is requirement number one. Wherever stocks might go in the short term, the longer-term outlook still appears plenty bright. With the global economy still growing, earnings and revenues rising, yield curves steeper today than a year ago, the political landscape benign and sentiment far from euphoric, this bull market should have plenty of room to keep on running.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — August 3 - August 72026-08-11

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, UK GDP, RBA

2026-08-10

2026-08-10 -

Market Analysis Four Overlooked Costs With Dividends2026-08-10

-

Market Analysis Rechewing Fed Independence Fears2026-08-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today