Personal Wealth Management / Market Analysis

On 3% Treasury Yields and the Oft-Misperceived ‘Relationship’ Between Yields and Stocks

While most media coverage portrays higher US Treasury yields as a risk for stocks, a look at history—as well as present fundamentals—strongly suggests otherwise.

10-year US Treasury yields hit 3.11% last Thursday—the highest level in 7 years—causing people to warn breaching this “critical level” signaled danger ahead.[i] The argument: Higher inflation, bond rates and borrowing costs will hurt the economy and stocks. Yet for all the chatter and volatility, bond market supply and demand fundamentals haven’t meaningfully changed over the past few months. We still see a tug of war between the two and competing forces that should keep long rates from making huge, lasting moves. As always, investors should beware reading too much into short-term volatility. Moreover, rising rates just aren’t the automatic negative many presume.

Bonds, like all assets, move on supply and demand. Demand is largely a function of inflation expectations. Current inflation is benign, hovering right around the Fed’s 2% target, and doesn’t look likely to spike. Inflation is always and everywhere a monetary phenomenon—too much money chasing too few goods and services. Broad money supply (M4) grew 4.6% y/y in April, its slowest growth since August 2017. M4 grew faster in most of 2016, topping 5% in several months, without spurring hot inflation. Global money supply growth is also tame.

Some argue rising input prices (e.g., oil and other commodities, transport costs) will soon drive consumer prices higher. Yet increases in some goods prices don’t translate to broad inflation. Nor are input costs, as measured by the producer price index, a leading indicator of consumer inflation. For one, companies aren’t universally pushing higher prices to customers. Some have opted instead to preserve market share and operate on smaller profit margins. Overall and on average, supply and demand in the end market determine prices, and demand generally can’t support price hikes without sufficiently fast money supply growth. Furthermore, 69% of the US economy and 59% of the CPI basket is services,[ii] which are more insulated from commodity and transport cost pressures. Therefore, we think it is a stretch to argue a smattering of higher costs will force bonds to pay a significantly higher long-term inflation premium.

The likelihood of benign inflation isn’t the only reason we don’t think long rates are starting a sustained march higher. Bond markets are global. US rates are among the highest in the developed world, which should attract money globally, especially with trillions in negative-yielding Japanese and eurozone debt outstanding. Moreover, supply isn’t galloping ahead of demand. US Treasury issuance is up somewhat this year—partly due to the higher budget deficit, and partly due to the Treasury making up for lost time when the debt ceiling prevented most new issuance—but not astronomically so. Meanwhile, outside the US, deficits are down all across Europe, with several nations (most notably Germany) running surpluses, which helps crimp supply growth globally.

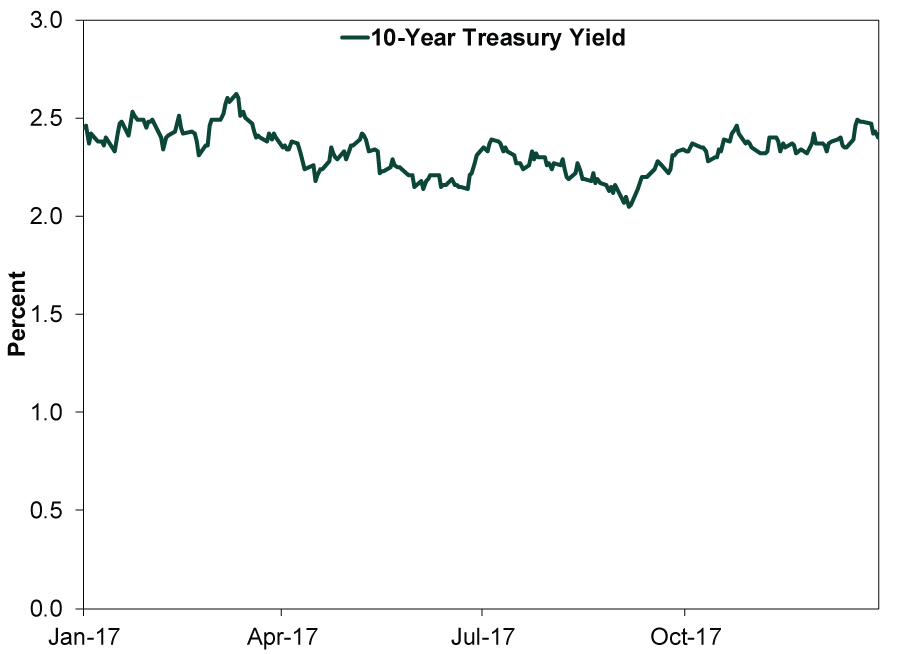

Short-term volatility is normal in bond markets. Each of the last two years featured big swings up and down, yet full-year moves were largely flat. As Exhibit 1 shows, yields started off 2016 at 2.24%. They fell to a record low 1.37%, then rose to end the year at 2.45%—up 21 basis points from start to finish. Exhibit 2 shows yields in 2017 moving as high as 2.62% and as low as 2.05% before ending the year little-changed at 2.40%. This year’s move is bigger—61 basis points so far[iii]—but like those moves, it doesn’t come with a change in fundamentals. Absent a big shift in supply or demand, we don’t expect a sustained move up (or down) in bond yields this year, either.

Exhibit 1: 10-Year Treasury Yield in 2016

Source: Federal Reserve Bank of St. Louis, as of 5/21/2018. 10-year Treasury yield, daily, 1/4/2016 – 12/30/2016.

Exhibit 2: 10-Year Treasury Yield in 2017

Source: Federal Reserve Bank of St. Louis, as of 5/21/2018. 10-year Treasury yield, daily, 1/3/2017 – 12/29/2017.

Some also fear rising rates make corporate debt too expensive for companies to bear, choking off financing and investment as well as jeopardizing corporate balance sheets. But most corporate debt is fixed rate, unfettered by gyrations in market rates. Rates would have to rise much higher and stay that way for a long time—forcing companies to refinance maturing debt at more costly rates—before significantly impacting company finances. Indeed, signs of credit stress aren’t evident: Corporate yield spreads, defaults and delinquencies remain historically low. This means companies have flexibility to increase borrowing even at slightly higher costs. Medium-grade corporate yields are presently up 68 basis points year to date, from 4.17% to 4.85%.[iv] If a 68 basis-point rise in borrowing costs is enough to render a project unprofitable and suspend an investment, it was shaky to begin with.

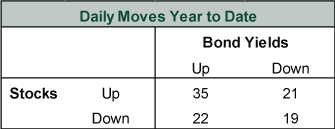

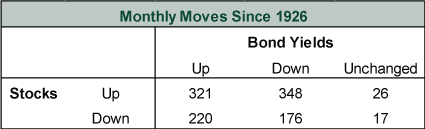

Moreover, whatever direction they head, bond yields don’t drive stocks. As Exhibit 3 shows, on days this year when bond yields rose, stocks rose 35 times and fell 22 times. No meaningful relationship there. On days when yields fell, stocks’ direction was a coin flip. Exhibit 4 extends this exercise to the 1,108 monthly moves since 1926. In the 541 months when bond yields rose, stocks rose 321 times and fell 220 times. In the 524 months bond yields fell, stocks rose 348 times and fell 176 times. Overall, about the only meaningful conclusion we can draw is that stocks rise more often than not, regardless of long rates’ wobbles.

Exhibit 3: Stocks and Bonds Move Independently—Daily Edition

Source: FactSet, as of 5/22/2018. S&P 500 daily percent price change and US 10-year Treasury daily yield change, 1/2/2018 – 5/21/2018.

Exhibit 4: Stocks and Bonds Move Independently—Monthly Edition

Source: Global Financial Data, Inc., as of 5/22/2018. S&P 500 total return monthly percent change and US 10-year Treasury monthly yield change, January 1926 – April 2018.

More recently, some suggest stocks benefited from a “great rotation” out of bonds in recent years as investors chased higher yields elsewhere—a trade that will reverse as bond yields rise, hurting stocks as money pours out. But fund flow data strongly suggest the great rotation never happened, as bond fund inflows have been pretty consistently positive throughout this bull market. Yield chasing en masse always struck us as a myth—oft-discussed but never seen. Arguing relatively higher stock yields are the sole reason investors bought stocks over the past several years also ignores the stock market’s many positive fundamentals, like solid corporate earnings and revenues, a growing global economy and relatively low legislative risk. Those drivers haven’t changed.

Ultimately, bond yield jitters strike us as the latest iteration of this year’s fear morph. This is a normal feature of most stock market corrections, and it doesn’t shock us that with stocks still below January’s high, investors are still seeking reasons to be fearful. Yet, in our view, the real time to be fearful is when fundamentals have demonstrably changed for the worst. As far as we can see, that just isn’t the case today.

[i] Source: FactSet, as of 5/23/2018.

[ii] Source: US Bureau of Economic Analysis and US Bureau of Labor Statistics, as of 5/24/2018. Private services-producing industries as a percentage of GDP, 2017, and services less energy services’ relative importance, March 2018.

[iii] Source: US Department of the Treasury, as of 5/24/2018. 10-year Treasury Yield change, 12/29/2017 – 5/23/2018.

[iv] Source: Federal Reserve Bank of St. Louis, as of 5/24/2018. Moody’s Seasoned Baa Corporate Bond Yield, 12/29/2017 – 5/23/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today