Personal Wealth Management / Market Analysis

Our Thoughts on Coal Stocks’ Return From the Abyss

Coal stocks aren’t contradicting long-term climate initiatives or a ripe investment opportunity today, in our view.

Energy stocks have been the hottest game in town since the electricity shortage erupted in mid-September, and one category is especially catching eyeballs: coal. One discussion that caught our interest today—and is well worth a read if you have the time and access—was a New York Times piece by Jeff Sommer that investigated the disconnect between near-term returns and long-term climate initiatives. In our view, it is a prime example of a simple point: Stocks look only about 3 – 30 months ahead.

For the better part of the last decade, pundits have presumed coal stocks were consigned to permanent weakness because emissions targets and international climate accords were killing off everyone’s least-favorite Christmas present. Some pointed to climate policy as the culprit (for better or worse) for coal stocks’ long-running lag and cited each coal plant closure as another nail in the coffin. But now coal use and coal stocks are soaring amid the global natural gas shortage, and it is drawing many investors’ attention. Some are confused, seeing this as contradicting the long-term direction of energy markets. Others see opportunity. We see neither.

When you own stocks, you own a share in future earnings. But stock prices today don’t reflect earnings 10 or 20 years from now, for the simple reason that the far future is impossible to predict. Hence, markets tend to looker closer to the present, weighing economic drivers and trends affecting earnings. So even if governments (particularly in developing nations) do phase out coal over the next few decades, that isn’t terribly meaningful to earnings today.

Still, though, for a rally to last, it would likely have to be backed by lasting drivers—that is why we say 3 to 30 months and not “right now” or “next week.” We don’t see that for coal. For one, the Energy sector is heavy on value stocks, which generally lag in a slow-growth world. Two, within Energy, we think major integrated oil and gas companies are likely a better means of diversification than coal, as supply and demand drivers for oil appear more balanced. To see this, consider why coal initially fell out of favor last decade. Perhaps climate policy played a role at the margin, but the chief driver was the shale revolution. That brought cheap, abundant, cleaner-burning natural gas to the fore. As that power source became cheaper than coal, a classic substitution kicked off, driving demand for the pricier, dirtier energy source down.

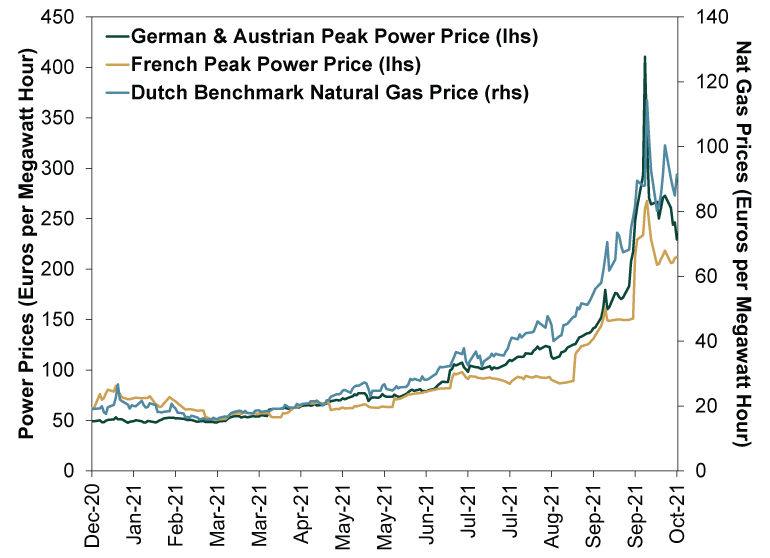

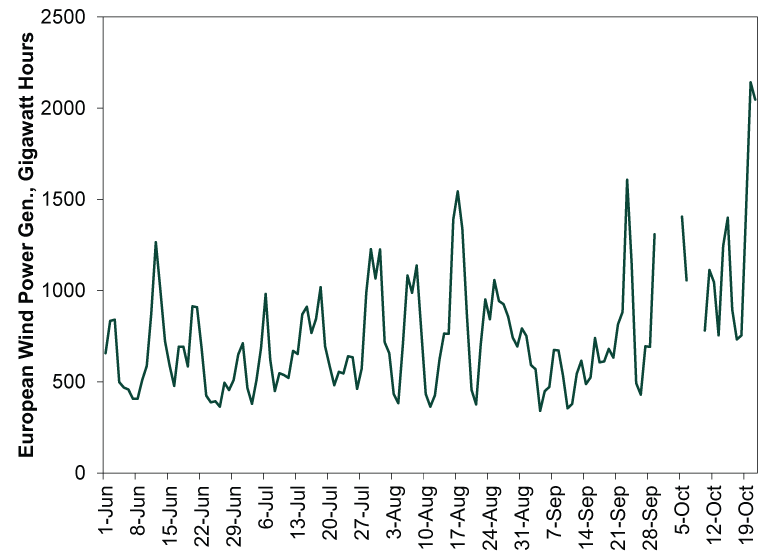

For the moment, that has reversed thanks to the acute natural gas shortage, naturally benefiting coal producers. But this doesn’t appear likely to last much more than three months, maybe five or six at the long end, as the natural gas shortage looks likely to ease sooner rather than later. As Exhibit 1 shows, natural gas prices globally have already started moderating, in large part because wind power generation has picked up. (Exhibit 2) That could reduce demand for coal relatively quickly, tugging down coal prices and producers’ earnings. It may take some time and could see reversals here or there—weather is hard to predict. But if this general trend persists, coal’s recent drivers will likely be blown away, rendering this recent coal stock bounce a thing of the past.

Regardless, we think this saga is worth bearing in mind whenever you see someone arguing that events 10 or more years out should influence stocks now. Ditto for events within the next 3 months. In the long term, anything is possible. But markets move on probabilities, not possibilities—specifically, the probability of profits being better or worse than expected over the next couple of years. In the very, very short term, it is highly likely stocks already reflect the events you are reviewing.

Exhibit 1: Natural Gas and Electricity Are Already Settling Down

Source: FactSet, as of 10/22/2021. Dutch TTF natural gas prices, EEX Phelix Peak electricity prices (Germany and Austria) and EEX France Peak power prices, 12/31/2020 – 10/22/2021.

Exhibit 2: European Wind Power Generation Is Picking Up

Source: WindEurope, as of 10/22/2021. Daily onshore and offshore wind power generation, 5/31/2021 – 10/21/2021. Note: WindEurope’s archive is missing data for a few days in late September and early October.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today