Personal Wealth Management / Market Analysis

Putting America’s Diesel Situation Into Perspective

Supply should prove more resilient than feared.

Steep oil prices have stolen headlines all year, enflamed by supply concerns after Russia’s invasion of Ukraine. Now, it seems US diesel prices are getting their turn after major US diesel supplier Mansfield Energy warned of a potential shortage earlier this week—particularly for the East Coast.[i] While it is possible such a shortage rekindles some near-term supply chain issues, we think the evidence suggests any pain would likely be short-lived. More importantly for investors, fears of potential diesel shortages have been widely discussed since March, suggesting negative surprise power for stocks is likely minimal.

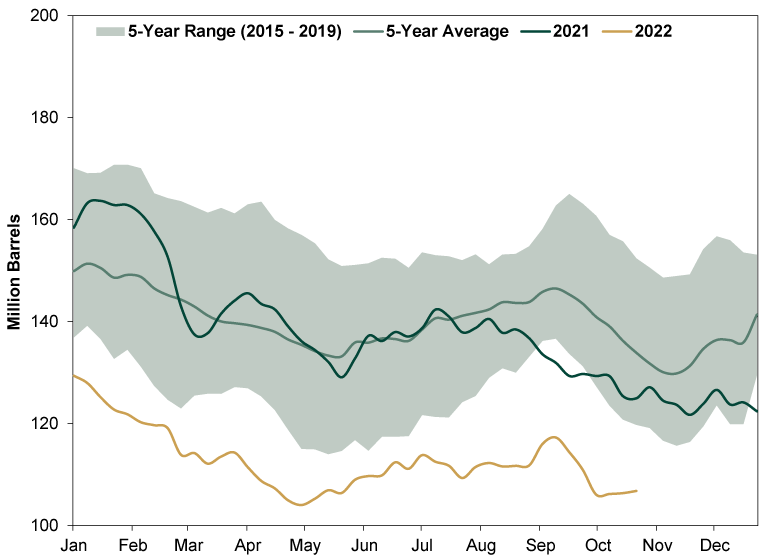

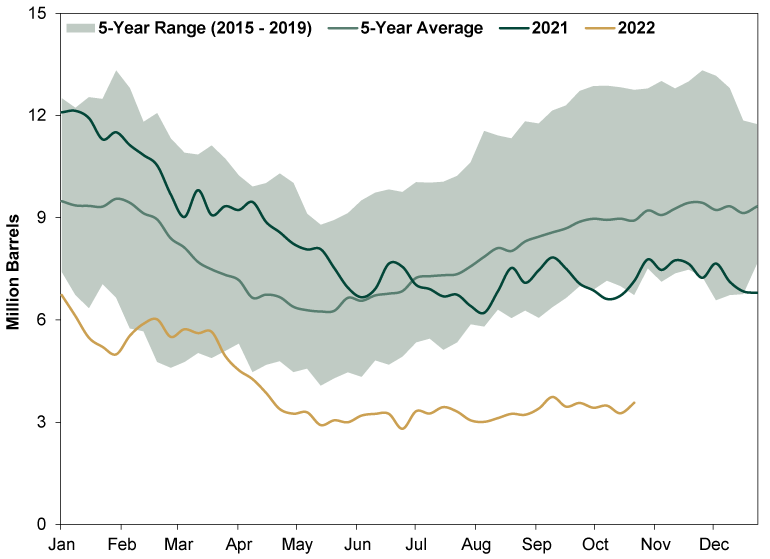

Diesel—heavily used in transport, trucking, farming, manufacturing and heating—is a hot commodity presently. Many fear a potential shortage would worsen supply-chain issues, push inflation higher and increase the likelihood of recession. There is little data on diesel itself. However, it, jet fuel and heating oil are primary distillate fuels—industry lingo for petroleum products made from vapors emitted by heating crude oil. US distillate inventories are currently about 20% below their five-year seasonal average, amounting to roughly 25 days of reserves.[ii] (Exhibit 1) This has pushed diesel prices up about 45% y/y.[iii] Supplies are particularly low—about -60% under typical levels at this time of year—in the Northeast, where heating demand is higher. (Exhibit 2)

Exhibit 1: Total US Distillate Inventories

Source: FactSet, as of 11/2/2022. Weekly ending stocks of total US distillate in millions of barrels, 1/7/2015 – 10/27/2022.

Exhibit 2: Northeast Distillate Inventories

Source: FactSet, as of 11/2/2022. Weekly ending stocks of total Northeast distillate in millions of barrels, 1/7/2015 – 10/27/2022.

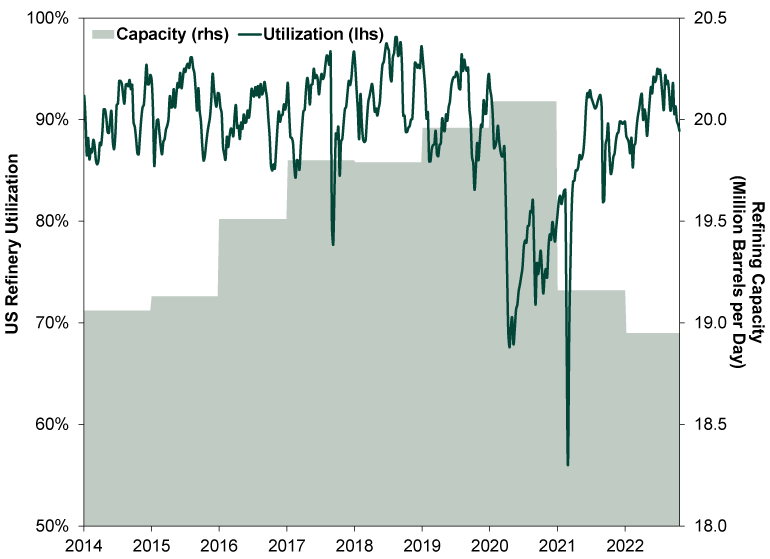

In our view, there are four main reasons for this year’s low diesel inventories. The first and primary one: US refining capacity is still below pre-COVID levels. (Exhibit 3) US refiners cut capacity at the start of the pandemic when fuel demand plunged, while others have closed facilities to convert them into biofuel refineries. Few have reopened. Even fewer new refineries have opened—a long-running trend in the US.[iv]

There are a few reasons for this. One, it is pretty difficult to reopen a refinery. It requires machinery inspections, operating permits, reintegration with supply chains, new staff hiring and training—all of which takes time. Two, refiners have little incentive to spend the capital to reopen them. It is an enormous upfront cost to build or reopen a refinery, which can take years to construct and even longer to recoup the sunk costs. Prices are high now, but if you consider the course of the last decade, they were mostly low—and on a rollercoaster ride overall. That experience made many drillers slow to increase oil output, and the same holds for refiners. It may be doubly true when many see environmental standards, increasing electrification of vehicles and the like potentially weighing on far-future demand. This isn’t to say refiners aren’t trying to boost capacity of their existing sites—refinery utilization was at 92% in September, up from 88% in January.[v] However, they seem less willing to invest in building new sites or reopen old sites.

Exhibit 3: US Refiner Capacity and Utilization

Source: FactSet, as of 11/2/2022. Annual US refinery capacity in million barrels per day and weekly refinery utilization rate, 1/1/2014 – 10/21/2022.

The second reason: The US hasn’t imported any petroleum products from Russia since April. Though Russia accounted for just 8% of US petroleum imports in 2021, 20% of those imports were used to refine products like diesel.[vi] Hence, their absence has had some impact. Third, backwardation—when near-term oil futures are priced at a premium to longer-term futures—bears some blame. It has caused diesel to lose value over time, reducing incentives to store large amounts needed ahead of winter. Finally, there are shorter-term supply and demand issues. Some refineries experienced maintenance outages this autumn, reducing output. The Colonial Pipeline—which supplies about half of the East Coast’s fuel and made headlines after getting cyber-attacked last year—also wasn’t fully operational. This—paired with seasonal demand spikes ahead of harvest, holiday shopping and winter heating seasons—deepened the impact on inventories.

Pain at the pump and localized supply-chain disruptions from high distillate prices are real possibilities. Small trucking companies, middle- to lower-income farmers and heating consumers—especially in the Northeast, which has started rationing fuel in some parts—are particularly vulnerable. However, evidence suggests any pain may be fleeting.

For one, while diesel inventories are lower than they have been historically, this doesn’t mean the US will run out in 25 days. That would happen only if all shipments and pipelines were to stop indefinitely overnight—virtually impossible. More supply is coming. The Colonial Pipeline is now running at full capacity to meet higher demand and bring additional diesel fuel to consumers. This could bring up to 1.2 million barrels per day of distillates to the East Coast.[vii]

Plus, energy traders are diverting Europe-bound diesel tankers to the US in order to capture higher prices. So far at least two tankers carrying a total of almost 1 million barrels of diesel have been rerouted.[viii] In their short-term hunt for higher margins, these traders’ additional supplies likely push longer-term prices down for consumers. There is also talk of the Biden administration easing the antiquated 1920s-era Jones Act, which requires shipments between US ports use US-flagged and manned vessels. That could help ease the Northeast’s supply issues.

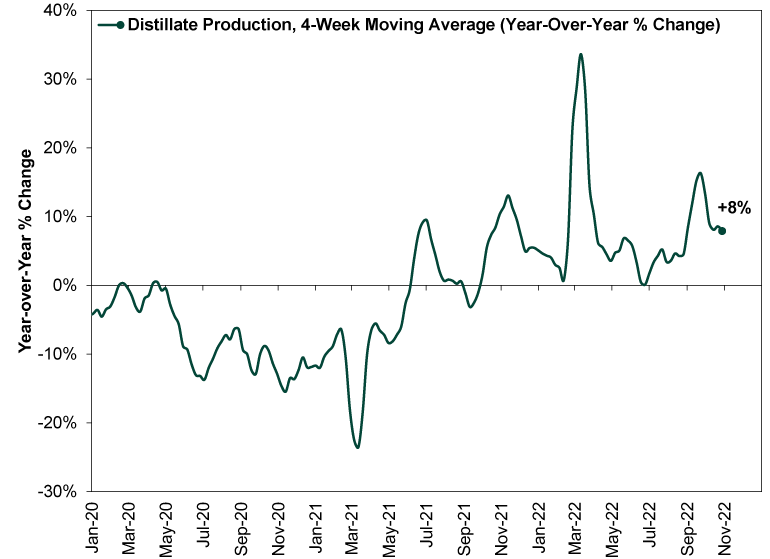

US refiners are also increasing their diesel production. Total US distillate production is up 8% y/y. (Exhibit 4) It is likely to continue rising amid increased refinery utilization.[ix] Typically, refiners ramp up production going into yearend in order to build sufficient inventories for the winter months’ heating demand. Plus, since October 2021, refinery utilization has increased nearly 3 percentage points, with 10% left to spare. (Exhibit 3)

Exhibit 4: US Distillate Production Growth

Source: FactSet, as of 11/2/2022. Four-week moving average distillate production, 1/3/2020 – 10/28/2022.

Most importantly for investors, fears of US diesel shortages have been widespread since March. They lack surprise power by now. For today’s supply issues to be a negative for stocks from here, they would have to be far worse than what stocks have already priced in, which doesn’t seem likely to us. Even with some localized fuel rationing in the Northeast, stocks haven’t shown an identifiable reaction. Markets are efficient discounters of widely known information. It isn’t likely they would wait to see an actual economic effect to react.

So while we don’t downplay possible near-term issues in the US or Europe, they don’t seem likely to deliver a shock substantial or lasting enough to drive material downside in markets. Higher diesel prices, yes. But higher prices incent more production—markets’ way of alleviating scarcity and shortages.

[i] Source: “US Diesel Supplier Warns Businesses to Prepare for Shortages, Higher Prices for Consumers,” Greg Wehner, FoxBusiness, 10/31/2022.

[ii] Source: US Energy Information Administration, as of 11/2/2022. Weekly days of supply estimates for distillate fuel oil, 10/22/2022 – 10/28/2022.

[iii] Source: US Energy Information Administration, as of 11/3/2022. Weekly US No2 diesel ultra-low sulfur (0-15 ppm) retail prices, 11/2/2021 - 11/2/2022.

[iv]“Frequently Asked Questions: When Was the Last Refinery Built in the United States?” Staff, US Energy Information Administration, 10/6/2022.

[v] Source: FactSet, as of 11/3/2022. Weekly US refiner capacity in thousand barrels per day and utilization rate, 1/1/2014 – 10/21/2022.

[vi]“The United States Imports More Petroleum Products Than Crude Oil from Russia,” Staff, US Energy Information Administration, 3/22/2022.

[vii] Source: McKinsey Energy Insights, as of 11/2/2022.

[viii] “Traders Divert Europe-Bound Diesel to US in Race to Re-Stock,” Ron Bousso and Laura Sanicola, Reuters, 10/14/2022.

[ix] Source: FactSet, as of 11/2/2022. Weekly US refiner and blender net production of distillate fuel oil, thousand barrels per day, 1/1/2019 – 10/28/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today