Personal Wealth Management / Market Analysis

Random Musings on Markets, 2019 Edition: Appetite for Musing

In which we round up a selection of curious and amusing financial stories for your reading pleasure.

After a nine-month-ish hiatus, Random Musings has returned for the summer (maybe), with our not-assured-to-be-weekly look at entertaining financial news stories. For those new to this column, our aims are fairly modest: We try to find the weird, quirky and hopefully humorous financial news stories around the web and round them up for you here. Since the last RMoM, a lot has happened. In Q4 2018, the S&P 500 posted its worst three-month return since 2011.[i] Q1’s was the best since 2009![ii] May 2019 was the worst May since 2010—second-worst since 1962.[iii] This month, with a trading day to go, is the best June since 1955. When we last wrote, Elizabeth Banks of Hunger Games fame was hosting bizarre 20-minute spots pumping mid-cap stocks. Now? She’s hosting the Press Your Luck reboot.[iv] (No whammies! Stop!) Only two Democrats had declared their candidacy for 2020 (John Delaney and Andrew Yang). Now we have 25![v] Elon Musk was getting in trouble for tweeting up a storm. Now? He is still getting in trouble for tweeting up a storm. Well, the more things change, the more they stay the same.

In that spirit, we bring you a look at a Fed dissent we are mostly sure wasn’t an audition, how one Democratic candidate is extending a financial lifeline to a few others, fun with straight-line math and more. We hope you enjoy it.

Was the Fed’s Lone Dissenting Vote Actually a Job Application?

At last week’s Fed meeting, one member of the policy-setting Federal Open Markets Committee (FOMC) cast a vote dissenting from the ultimate decision to hold rates steady. That vote, from St. Louis Fed President James Bullard, was for a 25 basis point (0.25 percentage point) cut.

Now, we are sure his dissent was based exclusively on his view of incoming data. Like 89.1% sure of it. But this does follow some pretty public pressure from a certain inhabitant of 1600 Pennsylvania Avenue advocating via Twitter for just such a move. So when news emerged Tuesday Bullard was “in talks” with the White House about a job opening on the Fed’s Washington-based Board of Governors, we couldn’t help but wonder if that dissenting vote wasn’t actually an indication of interest in the post. Now, again, we are mostly sure it isn’t. After all, as The Wall Street Journal reported, “Mr. Bullard would face a large pay cut if he were to accept a position on the Fed’s board. According to the central bank’s annual report, the St. Louis Fed president’s salary in 2018 was $381,000. Fed governors earn $183,100.”[vi] Yikes! Might we also point out to Mr. Bullard that the cost of living in DC is also far higher than St. Louis? If he isn’t already aware, we recommend consulting his own St. Louis Fed’s cost of living calculator.

Then again, taking the job would be a step closer to the Fed chair and, despite Fed officials often trumpeting their independence, this is how central bankers play politics. It is why that vaunted independence isn’t as ironclad as often portrayed. So while our primary theory is Bullard’s dissent wasn’t a job application or an audition, we can’t rule it out.

Bernie’s Big Bailout for Mayor Pete

A certain Independent senator vying for the Democratic Party’s presidential nomination made headlines this week for proposing a bill that, if passed, would use a shiny new financial transaction tax to magically wipe away all $1.6 trillion in outstanding student debt and make public higher education free for all. It is much more campaign virtue-signaling than viable legislation, and we doubt it has even a snowball’s chance of passing. But even so, we have some questions. Like:

- Will this entice fellow candidate “Mayor Pete” Buttigieg, who disclosed six figures’ worth of student loan debt, to vote for Bernie in the Indiana primary? What about California Rep. Eric Swalwell, another rival with student loans on the books? And Ohio Rep. Tim Ryan?

- If taxpayers are to fund higher education, will we get veto power over students’ majors, to ensure a decent return on our “investment” in terms of these students’ future income tax generation?

- Will we also get veto power over staffing decisions at schools? Can we make them cut potentially bloated administrations in order to rein in costs and reduce our tax burden?

- What about all the people who have already repaid their student loans in good faith, graduated without student debt or didn’t attend college? Will they receive retroactive stipends?

- Has anybody thought about the NCAA?

- Will businesses move their 401(k)s to offshore accounts so that retirement savers won’t get hit? What about state and local pension plans? Or will they get a super-secret government waiver?

- Will brokerage firms offer shiny new offshore IRAs?

- Will all that trading activity that happens in New York move to Bermuda, Zurich or London?

- Would Congress have voted to nationalize student debt in 2010 if they knew erasing it was the endgame?

To our cursory eyeballs, this proposal just looks like an epic case of picking winners and losers—not an economic panacea. Having student debt paid off isn’t assured to make Millennials ramp up consumption, get married and buy homes. While stories of six-figure debt abound, the Fed’s surveys say the “typical” amount of student debt ranges between $20,000 and $24,999—a not uncommon car loan, with deferred payment options in most cases.

The theory underpinning debt forgiveness and free college assumes education is a “public good,” with benefits redounding to all of America. So if this law passes, Elisabeth might decide to go get her Ph.D. studying the advancement of capitalist theory through Buffy the Vampire Slayer and Golden Girls. Just be thankful your taxes will support this critical endeavor in the name of the public good.

Adventures in Straight-Line Math

This week, the CBO performed its semi-annual ritual of releasing apocalyptic long-term debt forecasts. In it, we learned US debt will reach 144% of GDP by 2049, far exceeding World War II-era levels and almost doubling today’s 78%. The culprits, we are told, are rising health costs and an aging population, coupled with slow future GDP growth of just 1.9% annually.

We have never been fans of long-term forecasts, and we feel bad that the math whizzes at the CBO are required to churn them out. Any good scientist knows even small changes to variables can impact a model, and the next 30 years are almost surely filled with changes no one can predict today. So rather than try to do so, we will simply point out some of the assumptions the headline forecast makes.

- No changes to Social Security (alternate models factor in potential changes, including limiting benefits to annual revenues after 2032).

- 22% of the population aged 65 or older by 2049, even though there is zero way to know the age breakdown of immigrants over the next 30 years.

- A fertility rate of 1.9 children per woman from 2022 onward. What if Bernie pays everyone’s student loans and we get that mythical baby boom![vii]

- 3.8% average 10-year US Treasury yields through 2039, as if today’s interest rates mean anything to interest rates 20 years from now.

When we discovered that last item, we thought it would be fun to dig up 1989’s CBO forecast to see if they nailed 2019’s interest rates. Alas, however, back then they only projected 5 or 10 years out, depending on the publication. Still long term, but a heck of a lot more reasonable than 30 years. If only the political climate would enable a return to the old ways.

Again, we aren’t picking on the CBO here. Their report is crystal clear that people shouldn’t take the headline projections to the bank. It acknowledges repeatedly the uncertainty inherent in its exercises. For instance, on page 8, it states: “In CBO’s assessment, there is about a two-thirds chance that federal debt would be between 71 percent and 175 percent of GDP in 2039.” That wide range presumes no changes to laws affecting debt. If the no-change scenario has that much uncertainty, how much more could the actual future, with all its unknowns, vary?

So whenever you encounter a super long-term forecast, whether it is scary or sunny, just remember the CBO’s massive amounts of hedging and warnings of uncertainty, and then resume going about normal life.

The Thing With “All” Is…

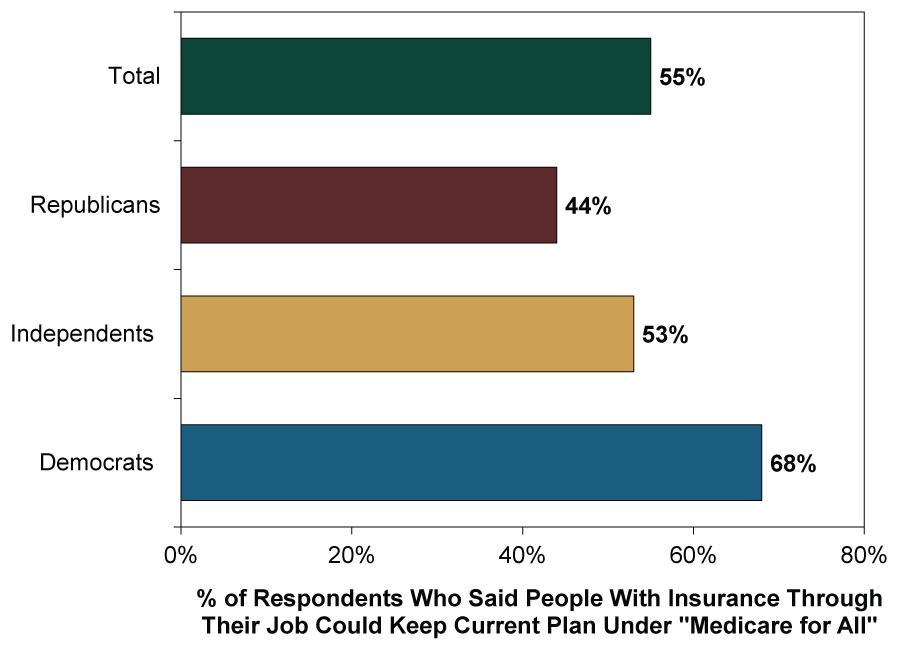

At this week’s opening Democratic Debates, several candidates professed to support Sen. Bernie Sanders’ plan to create single-payer, government-provided health insurance. The plan, dubbed “Medicare for All” has been circulating for a few months now, with several leading Democrats reportedly backing it—including Sen. Elizabeth Warren and New York Mayor Bill de Blasio Wednesday night. Now, like the aforementioned student loan bailout, we won’t spend much time here analyzing these policy ideas—the potential nominee and Congressional races are much too far off to make that worthwhile. However, we saw one striking poll question from the Kaiser Family Foundation (KFF) on the subject. Here is a depiction of it.

Exhibit 1: Medicare for … umm … All?

Source: “KFF Health Tracking Poll – June 2019: Health Care in the Democratic Primary and Medicare-for-All,” Ashley Kirzinger, Cailey Muñana, Lunna Lopes and Mollyann Brodie, Kaiser Family Foundation, June 18, 2019.

From this, we draw three conclusions. One, a majority of Americans believe they are not included in the word, “All.” How odd. Two, time may prove us wrong, but to date, campaigning on big policy ideas seems like it isn’t catching lots of potential voters’ eyeballs. Medicare for All isn’t a very new idea. But it seems most folks are unaware of a pretty key part. Three, the Republicans have really not bothered to target this as yet, considering 44% of people who claim party affiliation aren’t up to speed on it. This last point shows you just how early in the campaign this is. Even the GOP apparently believes it is too soon to address a much-ballyhooed plan touted by several Democratic frontrunners.

So You’re Telling Us There’s a Chance …

Here is some friendly unsolicited advice: If you are trying to handicap the likelihood of a no-deal Brexit, maybe don’t lean on things the two men vying for Conservative Party leadership are saying. They have demonstrated a rather remarkable inconsistency on this issue. We shall let them speak for themselves.

- The way to get our friends and partners to understand how serious we are is finally, I’m afraid, to abandon the defeatism and negativity that has enfolded us in a great cloud for so long and to prepare confidently and seriously for a WTO or no-deal outcome. – Boris Johnson, June 24

- But I don’t think that [a no-deal Brexit] is where we are going to end up – I think it is a million-to-one against – but it is vital that we prepare. – Boris Johnson, June 26

- I’ve always said that in the end, if the only way to leave the European Union, to deliver on the result of the referendum, was to leave without a deal, then I would do that. But I would do so very much as a last resort, with a heavy heart, because of the risks to businesses and the risks to the union. – Jeremy Hunt, June 3

- It’s not impossible to do this [renegotiate the Brexit deal] by 31 October, but it will be difficult. I’m not committing to a 31 October hard stop at any cost, because I don’t think you can make that guarantee. – Jeremy Hunt, June 16

Sooooo … have to be ready for a no-deal Brexit, but it isn’t going to happen. Leave without a deal, sure, but not really because you can just renegotiate with Brussels until the end of time, if necessary, to get a deal. Looks like even knowing the leadership race’s outcome next month won’t help businesses get any more clarity, alas. Get ready for a summer of uncertainty. One that would be all the more pleasant, we think, if Mr. Johnson would at least start an Instagram for his now-infamous wooden model buses.

Enjoy your weekend.

[i] Source: Global Financial Data, Inc., as of 6/28/2019. S&P 500 rolling three month total returns, December 1925 – June 2019.

[ii] Ibid. June still had a day to go as of this writing, which we guess could change this.

[iii] Ibid.

[iv] We ask you: Is this a promotion?

[v] We see you, Mike Gravel!

[vi] “Bullard Approached About Board Seat,” Paul Kiernan, The Wall Street Journal, 6/26/2019.

[vii] Disclosure: This is a joke.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08 -

Market Analysis On the Iran Flare Up2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today