Personal Wealth Management / Politics

Regulating Regulators’ Regulations

It seems were going to have fewer nonsensical federal regulations following a recent government review. But let’s hope this baby-step doesn’t conclude their efforts.

In this year’s State of the Union, President Obama made a highly sensible suggestion we entirely agree with: Review all existing federal regulation to ensure it isn’t overly burdensome and actually achieves its stated intentions. Roughly eight months later, how’s that effort going? Well, the Office of Management and Budget’s (OMB) Cass Sunstein provides an update in today’s Wall Street Journal touting the government’s successes to date. In all, the reforms announced are expected to save more than $4 billion over the next five years—which sounds like a big number but actually isn’t even remotely big relative to our economy’s size. Moreover, is it even sensible to quote regulation in terms of its direct costs to businesses?

First and foremost, we aren’t anti-regulation. We’ve said many times well-reasoned regulation is a critical component of a rules-based, free market, capitalist society. But there’s no doubt a good deal of regulation on the books is dated, conflicting, does more harm than good, has no clear objective and generally may have made some sense at one point but that sense has since been long lost in reams of bureaucratic red tape. (Mind you, this isn’t just our opinion, but the official position of this nation’s government.)

However, it’s largely impossible to “price” regulation in many cases and only partly on-target to try—the question isn’t solely what businesses pay now, but also what economic activity doesn’t occur because of regulation. For example, it would be extraordinarily difficult to attempt to slap an all-inclusive price tag on the reduction in IPOs and downstream business spending impacts stemming largely from 2002’s Sarbanes-Oxley Act, but that doesn’t mean those effects aren’t real.

Instead of a government-issued cost savings estimate associated with a miniscule, government-ordained reduction in a government-created regulatory morass, we suggest measuring this in paper, staffing and budgets. From 2000-2010, full-time employment at regulatory agencies increased 54.3%. Admittedly, the Transportation Security Administration accounts for roughly half the gain, but more staffing equals more regulators—whether it’s 54% more or something smaller. Additionally, regulatory agencies’ staffing has increased 13% since President Obama took office and is expected to grow 3.9% and 3.5% in 2011 and 2012, respectively. Hardly the direction you’d expect it to move if true regulatory cuts were being made!

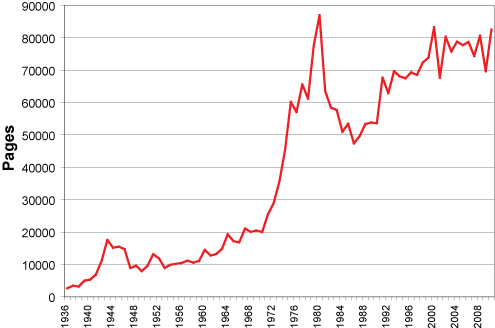

Or how about the following graph, which shows the federal registry’s growth since 1936—again, not especially indicative of less regulation. (Incidentally, if you’re interested in reading a copy of your own, it will cost you a whopping $929 if you’re a US citizen—but add a 40% premium if you’re a foreigner.)

Pages in the Federal Registry, 1936-2010

Sources: US Government Printing Office, Law Librarians of Washington, D.C.

Maybe that increased workforce consists of sharp, targeted deregulators flipping through the federal government’s 80,000+-page regulatory tome looking for pages to remove. We hope so. But considering we’ve heard similar government-streamlining talk from multiple administrations, we’re skeptical.

From a budget perspective, it’s easy to see regulatory growth. Outlays to federal regulatory agencies grew 63.1% from fiscal years 2000-2010. Excluding Dodd-Frank and the Affordable Care Act (many aspects of which are neither in place nor determined), regulators’ budgets are projected to grow more slowly during 2011 and 2012—but growth is growth. And growth in staffing, budgets and paper doesn’t amount to much real deregulation.

Rather than relatively inconsequential regulatory cuts—though they’re inarguably a step in the right direction—what may be more urgently needed is an overhaul of government’s regulation creation process. Consider this depiction of the federal regulatory process. There are a handful of reasons for concern. Here’s one: Step one in the rulemaking process includes drivers like either government agency employees brainstorming about priorities and plans or accident response. The former is a bad way to get good regulation, since the officials aren’t even impacted. The latter is tantamount to regulatory backlash—a recipe for politically motivated, reactionary policy (read: bad regulation). Public comments aren’t taken until step six—a step that can be bypassed “if an agency determines that a rule likely would not generate adverse comment.” Which means the very folks impacted by potential regulations may never get the chance to comment on them—or if they do, their opinion isn’t considered until well down the road to finalization. Is it even a good idea to task government employees with creating unsolicited regulation? After all, what’s their incentive to then say, “Our current regulatory environment is sufficient”? Answer: None—and that can lead to a lot of dumb rules.

As of today, we apparently have marginally fewer of these silly regulations, and we certainly won’t complain about progress of any magnitude toward reducing businesses’ regulatory burdens. In general, whereas sensible regulation can smooth the functioning of many industries, knee-jerk and/or purely politically motivated regulation can hamper productivity and require businesses to expend resources complying with regulations—resources they might otherwise use creating jobs, expanding or innovating (a concept we’ve discussed before). But realistically, the recent regulatory cuts amount to a drop in the proverbial bucket—especially when regulations like the aforementioned Dodd-Frank are legally on the books but carry as of yet-untold “costs,” given all the downstream regulation isn’t even written.

When it comes to regulating its own regulatory volume, in our view, the government has and largely continues to fall pretty short.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today