Personal Wealth Management / Market Volatility

Some Perspective on October’s Resurgent Economic Growth Concerns

Beyond PMIs and a couple days’ market wobbles, broad data aren’t hinting at a recession, in our view.

Reminiscent of August, this week markets turned rockier, with many pundits citing “weak data” and renewed US recession chatter. World and US stocks sold off on Tuesday and Wednesday, falling a total of -2.7% and -3.0%, respectively.[i] Headline reactions to the swings ranged from “Stocks Tumble, Bonds Climb as Slowdown Fears Mount” and “Stocks Are Off to Ominous Start in Fourth Quarter” to worrying that weak manufacturing is infecting the stronger services sector. While we agree there are weak spots in the global economy presently, we think the growing talk of a recession is going much too far. Here we will try to share some perspective on what is fueling the fears—and why we don’t think it is a call to action now.

The principal “weak spot” in the US economy is manufacturing—a global trend, and not a new one. In many corners of the world, manufacturing purchasing managers’ indexes (PMIs, surveys tallying the breadth of growth) aren’t looking great. So it was this week, when Tuesday’s Institute for Supply Management (ISM) US manufacturing PMI came in at 47.8, meaning more than half of businesses contracted—for the second straight month.[ii]

That isn’t so hot. But there are a couple of points to consider here: One, as we’ve written many times on these pages, manufacturing is a small slice of most major economies, including America’s. According to data from the Organization of Economic Cooperation and Development, it is 11.6% of US GDP. Services is nearly seven times bigger. ISM’s non-manufacturing PMI—which includes the services industry, mining and construction—slowed in September. But it remained in expansion at 52.6.[iii]

Further, PMIs aren’t perfect measures of growth. Because they tally only growth’s breadth, narrowly contractionary data like September’s manufacturing PMI don’t necessarily mean output fell. If the minority of firms reporting growth expand quickly enough, they can offset contraction elsewhere. There is also a large sentiment component to these data that can wiggle alongside headlines and events. The Brexit vote in June 2016 is the classic example: PMIs tumbled immediately thereafter, but GDP didn’t decline.

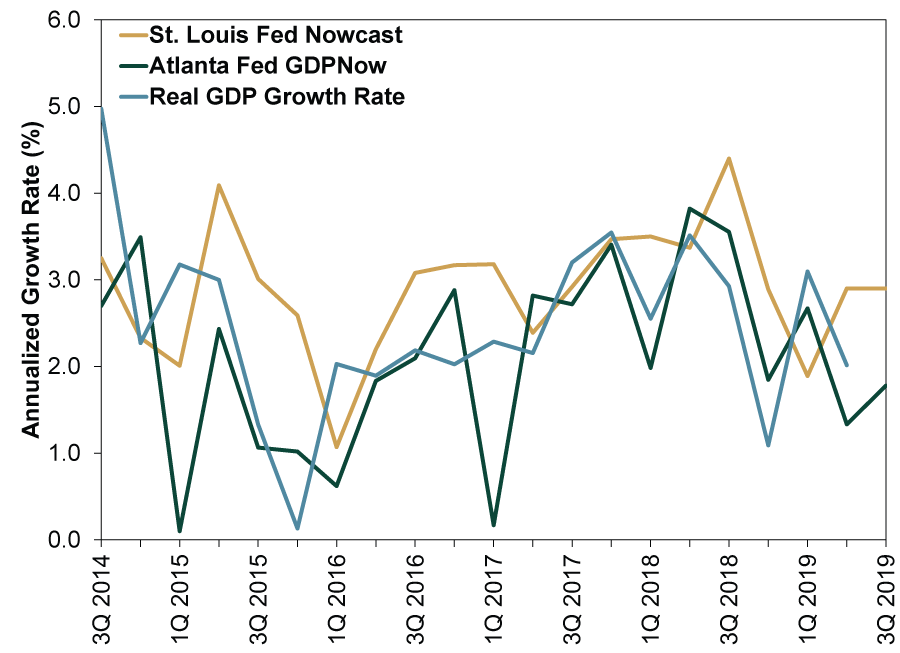

So while PMIs are good tools and we don’t dismiss them whatsoever, you can’t automatically take them to the bank. You must consider other data. To our minds, this is one of the strengths of various attempts to “nowcast” GDP. These gauges—constructed and maintained by the Federal Reserve Banks of New York, Atlanta and St. Louis—combine a broad array of data releases to generate a moving estimate of the current quarter’s GDP. They aren’t precise, of course! But they tend to align directionally with actual GDP growth. (Exhibit 1)

Exhibit 1: Nowcasts Hint at GDP’s Direction

Source: Federal Reserve Bank of St. Louis, as of 10/2/2019. St. Louis Fed GDP Nowcast and Atlanta Fed GDPNow growth estimates at quarter end. US real GDP growth rate in same quarter as forecast.

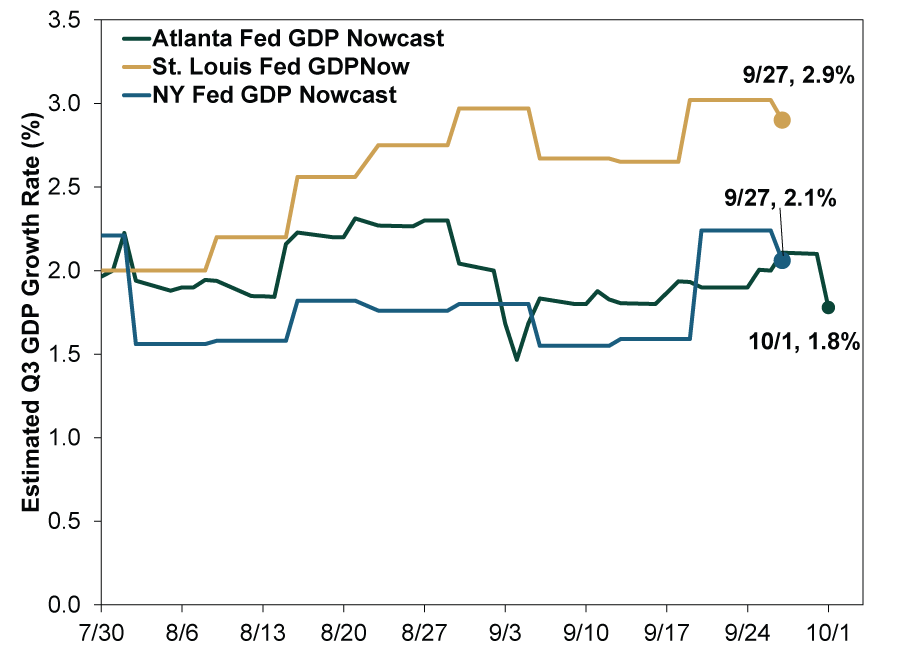

So, you might ask, “How have estimates of Q3 growth moved with data releases?” That would be a good question! Exhibit 2 answers it.

Exhibit 2: None of the Three Nowcasts Project Q3 Contraction

Source: Federal Reserve Banks of St. Louis, New York and Atlanta, as of 10/2/2019. The Atlanta Fed’s GDPNow is updated daily when economic data included in its model are released. The other two are updated weekly.

Hence, data broadly suggest growth is persisting. Slowing, maybe. But growth often ebbs and flows in bull markets—we have seen two manufacturing-led slowdowns in this cycle. Both featured contractionary manufacturing PMIs (2011 – 2012 and 2015 – 2016). Neither killed the bull market and expansion.

Of course, all these are just Q3 data. Stocks are likely already looking beyond this quarter. But a recession—a broad-based contraction in economic activity—doesn’t seem at hand, based on available evidence. Hence, we suspect recent market volatility is much more about sentiment than fundamentals—likely to prove another frustrating-but-fleeting wobble and not a bear market.

[i] Source: FactSet, as of 10/3/2019. MSCI World return with net dividends and S&P 500 total return, 10/1/2019 – 10/2/2019.

[ii] Source: Institute for Supply Management, as of 10/3/2019. https://www.instituteforsupplymanagement.org/ISMReport/MfgROB.cfm

[iii] Source: Institute for Supply Management, as of 10/3/2019. https://www.instituteforsupplymanagement.org/ISMReport/NonMfgROB.cfm

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today