Personal Wealth Management / Market Analysis

Some Thoughts on Greece’s Don’t-Call-It-a-Default

Things got even weirder the day after.

Greece's Tweeter-in-Chief, Prime Minister Alexis Tsipras, gives a national television address urging Greeks to reject harsh austerity. Photo by Greek Prime Minister's Office via Getty Images.

So Greece officially missed its €1.5 billion IMF payment due Tuesday, and it is now "in arrears" with the organization. It is not in "default," because the IMF doesn't use that term. Nor does missing an IMF payment trigger credit default swap (CDS) payouts or earn a "default" grade from credit ratings agencies. But that's all semantics. What matters more is where Greece goes next.[i] Whatever verb you use to describe what happened Tuesday, Greece has missed a debt payment and is without a bailout program for the first time in five years.

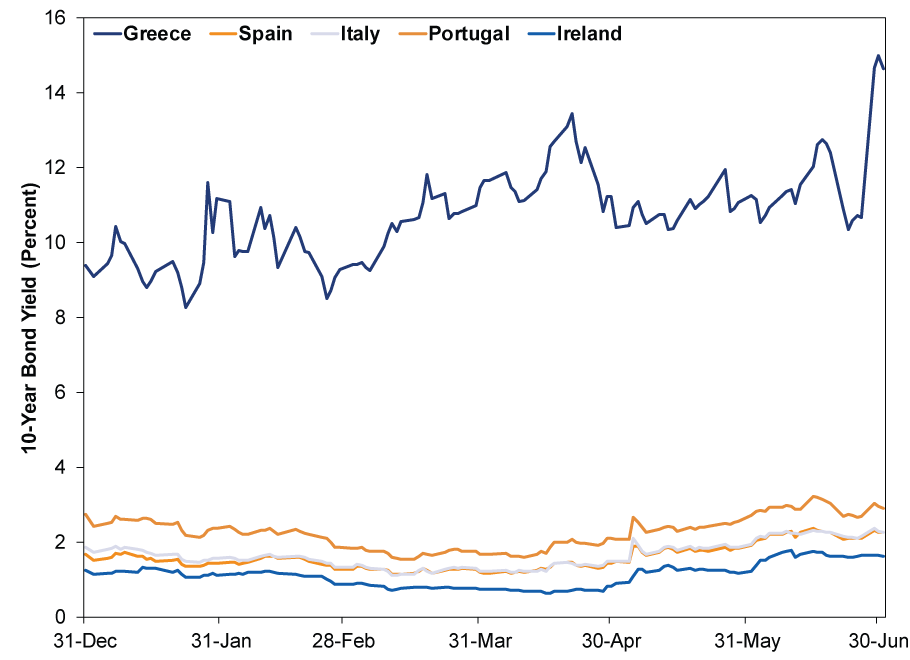

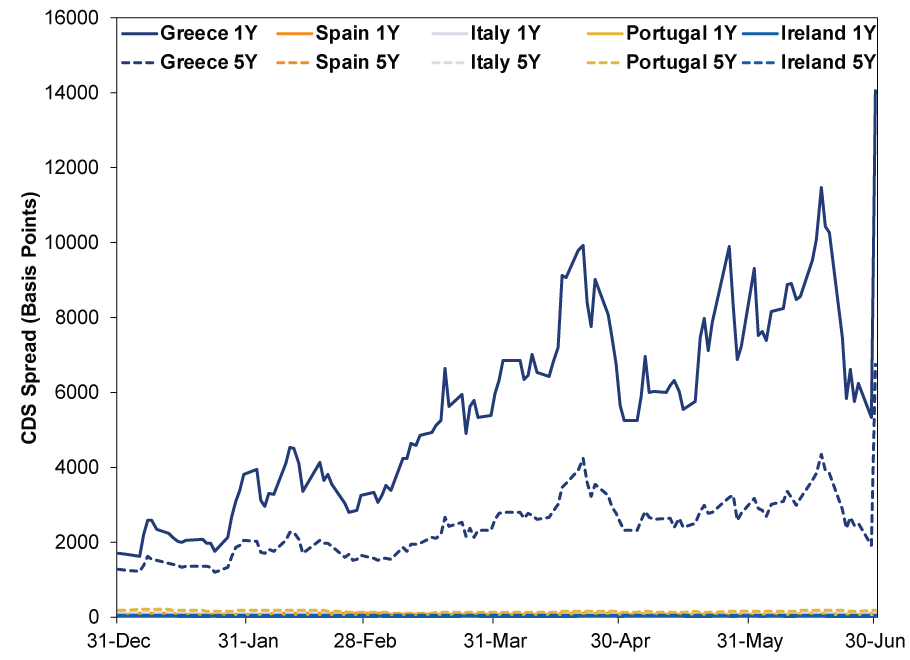

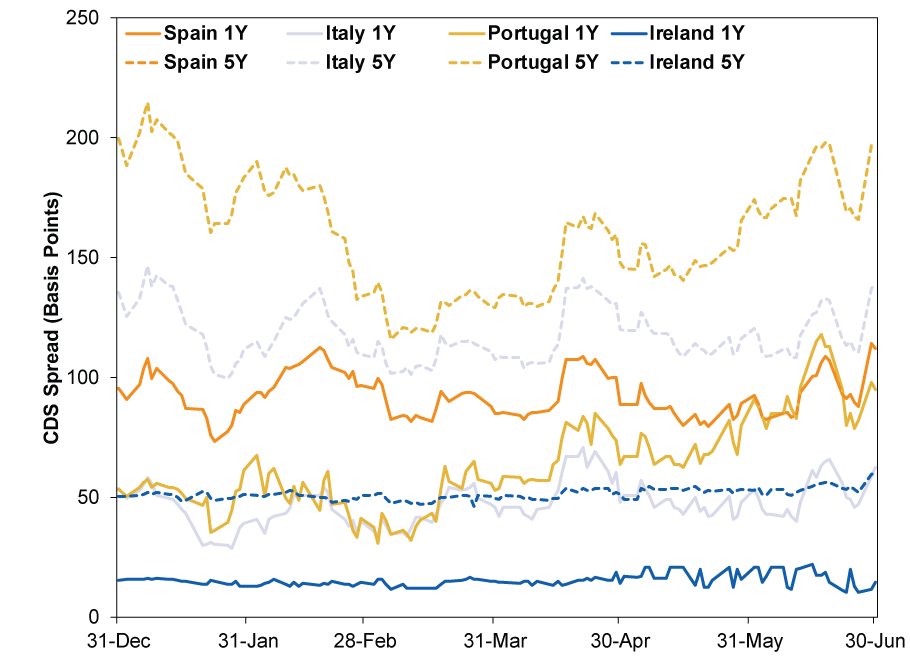

Most importantly, markets have taken all this in stride. US stocks rose 0.3% Tuesday, as everyone counted down to IMF zero-hour, and gained another 0.7% Wednesday.[ii] European stocks rose across the board Wednesday. The Stoxx Europe 600 gained 1.5%, while Stoxx' narrower eurozone benchmark rose 2.1%.[iii] Big winners included France (1.9%), Germany (2.2%) and Italy (also 2.2%), though Spain, Ireland and Portugal all topped 1%.[iv] Peripheral bond yields ticked down a bit for the second day in a row (Exhibit 1). Greek CDS costs went through the roof on Tuesday (Exhibit 2). The others' didn't-they rose Monday, but not to an alarming degree. They're still near post-crisis lows, and Monday's rise was in line with volatility earlier this year (Exhibit 3). No contagion here, folks.

Exhibit 1: Peripheral Eurozone 10-Year Bond Yields

Source: FactSet, as of 7/1/2015. Greek, Spanish, Italian, Portuguese and Irish 10-year yields, 12/31/2014 - 7/1/2015.

Exhibit 2: Peripheral Eurozone CDS Spreads

Source: FactSet, as of 7/1/2015. Greek, Spanish, Italian, Portuguese and Irish 1- and 5-year CDS spreads, 12/31/2014 - 6/30/2015.

Exhibit 3: Exhibit 2 Without Greece

Source: FactSet, as of 7/1/2015. Spanish, Italian, Portuguese and Irish 1- and 5-year CDS spreads, 12/31/2014 - 6/30/2015.

Greece might not have technically defaulted Tuesday as far as linguists and the arbiters of these things are concerned, but judging by one-year CDS nearly tripling in one day, markets expect it any day. It could happen as soon as July 10, when Greece must redeem €2 billion in maturing short-term debt. In theory they could refinance it with new bonds, but Greece has all but lost access to capital markets, as Prime Minister Alexis Tsipras admitted in his written plea for a third bailout on Tuesday.

Yes, a third bailout. Greece can't get any more money from the IMF until its government makes good on that overdue payment, so Tsipras turned away from the IMF/EU/ECB "troika" and to the European Stability Mechanism (ESM), requesting €29 billion in crisis loans over the rest of this year and next, to "be used exclusively to meet the debt service payments of Greece's external and internal debt obligations." He also asked to restructure debt due to the EFSF (the ESM precursor that funded the last bailout), presumably by creating a more flexible payment schedule. In a separate letter to troika leaders (European Commission President Jean Claude Juncker, ECB chief Mario Draghi and IMF Managing Director Christine Lagarde), he said Greece "is prepared to accept" the troika's most recent conditions, albeit with a few minor amendments "that fully respect the robustness and credibility of the design of the overall program."

Now, this might sound like a solution, but it is actually a problem. Why? These are the same conditions Tsipras denounced last week. They are the same conditions he is asking Greeks to vote for or against in a referendum on Sunday-and he is urging Greeks to vote "No."

Needless to say, eurozone leaders don't find any of this credible. They aren't negotiating until after the referendum. There is a sharp divide between Tsipras' "ok we'll do it" to creditors and his "no don't do it!" preaching to voters. Eurozone leaders don't see much point in discussing terms Tsipras has already told voters to reject. German Finance Minister Wolfgang Schäuble said they can't do anything until Greece clarifies what it wants. Eurozone finance ministers said there are "no grounds for further talks" until after the referendum. One of German Chancellor Angela Merkel's close allies likened another bailout at this point to pouring money down a black hole. Italian PM Matteo Renzi didn't mince words either: "It's not the case that we have taken early retirement pensions away from the people of Italy just to allow the Greeks to have them! We have brought in labor reform, but it is not the case that, with our money, a number of Greek shipowners can continue not to pay taxes. I could go on." Merkel herself, perhaps resigned to Grexit at this point, said "the future of Europe is not at stake."

So all eyes turn to the referendum. As we wrote earlier this week, it is a big can of worms. One, it is a vote on a bailout package that no longer exists and terms that are no longer on the table. Two, the referendum doesn't meet the European Council's standards for transparency and clarity, as it doesn't meet the two-week minimum between announcement and vote (it also has some other technical issues). Three, it might be unconstitutional. Four, the referendum documents, by many accounts, were mistranslated into Greek. Five, it asks voters to read through pages of bailout terms and analysis of Greek debt sustainability-materials anyone who isn't a trained economist would struggle to understand-and then accept or reject the terms. Six, depending on who you ask, it is (Merkel, Renzi) or isn't (Tsipras) a referendum on euro membership. Who do you trust? How do you decide? Will anyone accept the results as legitimate?

Because of these issues, speculation was rife that Tsipras would call the whole thing off. But he isn't, and he is still urging Greeks to vote "No!" Or, in Greek, "OXI!" Polls, for whatever they're worth, show a tight race, with support for "No" plummeting after capital controls took hold. Meanwhile, the ECB declined to boost emergency funding for Greek banks Wednesday, and when Greek banks opened to serve cash-strapped pensioners who don't have credit or debit cards, it was basically mayhem. Eurozone leaders say a no vote will destroy Greece's banking system. To that, Tsipras says ... well, we'll let the man's Tweets speak for themselves:

Sunday's #referendum is not about whether or not #Greece remains in the Eurozone. #dimopsifisma

-Alexis Tsipras @tsipras_eu 7:32 AM PDT July 1, 2015

Come Monday, the Greek government will be at the negotiating table after the #referendum, w/better terms for the Greek people. #dimopsifisma

-Alexis Tsipras @tsipras_eu 7:38 AM PDT July 1, 2015

Its unacceptable that in Europe of solidarity bank closure would be forced, as a response to Gov't letting Greek ppl decide #Greferendum

-Alexis Tsipras @tsipras_eu 7:47 AM PDT July 1, 2015

You're being blackmailed & urged to vote Yes to all of institutions' measures without any solution to exiting the crisis. #dimopsifisma#OXI

-Alexis Tsipras @tsipras_eu 7:56 AM PDT July 1, 2015

#ΟΧΙ (NO) is not just a slogan. NO is a decisive step toward a better deal. #Greece#dimopsifisma#Greferendum

-Alexis Tsipras @tsipras_eu 7:57 AM PDT July 1, 2015

#ΟΧΙ / NO does not mean breaking w/Europe, but returning to the Europe of values. #ΟΧΙ / NO means: strong pressure. #Greece#dimopsifisma

-Alexis Tsipras @tsipras_eu 7:59 AM PDT July 1, 2015

There are those who say that I have hidden agenda, that w/an #OXI / NO vote, I'll take #Greece out of EU. They are flat out lying to you.

-Alexis Tsipras @tsipras_eu 8:05 AM PDT July 1, 2015

We owe it to our parents, our children, ourselves. It is our duty. We owe it to history. #Greece#Greferendum#dimopsifisma#OXI

-Alexis Tsipras @tsipras_eu 8:25 AM PDT July 1, 2015

(Finance Minister Yanis Varoufakis, by contrast, kept his online campaigning to six bullet points on his blog.)

Anyway, at this point it looks like things are in a holding pattern until Monday, though you never know. The Greek government's behavior is increasingly irrational and unpredictable. Books will one day be written about the firebrand Prime Minister who Tweeted portmanteaux. But for now we're still living this story, and we'll have to keep living it, day by day, to see what happens.

So stay tuned, watch this space, and watch our "Headlines" page[v]-we'll keep you posted. Over and out.

[i] Not literally, because obviously Greece will stay right where it is on the map, nestled between Turkey and Albania, Macedonia and Bulgaria. It won't sidle across the Balkans to cozy up to Russia. We assume its Turkish border won't disappear to form a new Ottoman Empire, which we'd be inclined to call New Ottomania or the Grottoman Empire. And it won't sink into the Mediterranean. It'll still be there, being Greece, with its islands, mountains, statues and ruins.

[ii] FactSet, as of 7/1/2015. S&P 500 daily price return on 6/30/2015 and7/1/2015.

[iii] FactSet, as of 7/1/2015. Stoxx Europe 600 and Euro Stoxx 50 daily price returns in EUR on 7/1/2015.

[iv] FactSet, as of 7/1/2015. France's CAC 40, Germany's DAX, Italy's FTSE MIB, Spain's IBEX 35, Ireland's Ireland ISEQ and Portugal's PSI All-Share daily price returns in EUR on 7/1/2015.

[v] And check out these charming Greek memes, because if you can't laugh, what else is there? We're partial to the one with the kitty.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today