Personal Wealth Management / Market Analysis

Stocks Don’t Need More QE

Bringing back quantitative easing (QE) would be more harmful than beneficial.

In light of recent market volatility, some have suggested not only delaying a Fed rate hike-but bringing back quantitative easing (QE)! The logic? Stocks rose during QE and are now officially flat since it ended, thus markets must need a monetary drip feed-and the central bank should consider bringing it back. This is a case of correlation without causation, in our view. We believe QE is actually an economic depressant, not the stimulant many claim, and resurrecting it would probably do more harm than good.

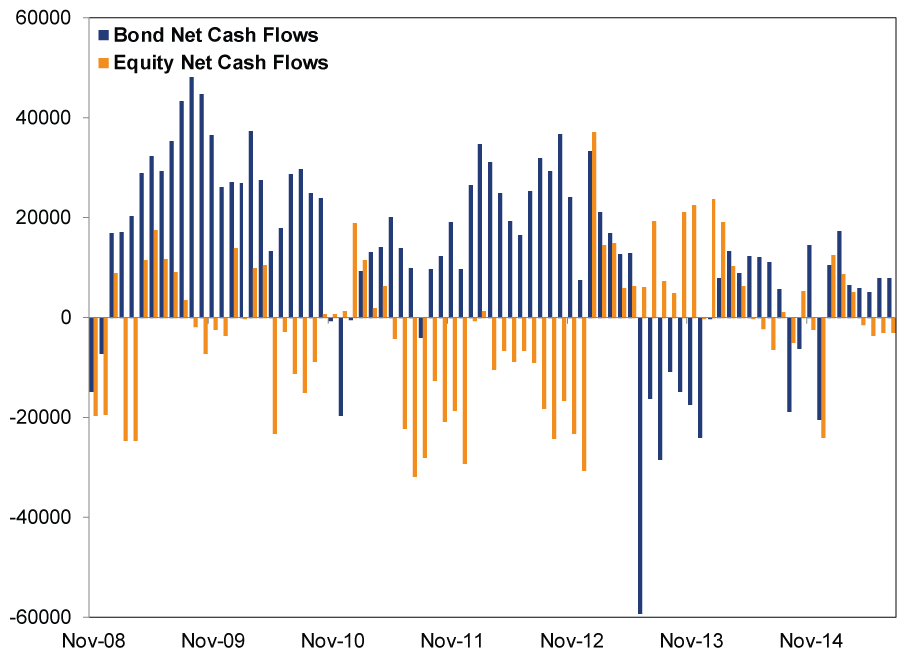

While it's true QE coincided with great returns, many drivers (economic, political and sentiment) move markets-not just monetary policy. One theory posits that by lowering long-term interest rates-and squashing yields-QE drove investors from bonds to stocks. Another says the Fed's funny money went into stocks directly, propping up the bull. We see a couple issues with these hypotheses. The first misunderstands why folks hold fixed income. Most investors generally own stocks for long-term growth purposes and bonds to lessen short-term volatility and provide cash flow (there are exceptions, of course, but overall and on average, this is how investors operate). Most bond investors likely won't jump to an entirely different (and more volatile) asset class if Treasurys yield next to nothing-they would likely just seek a higher-yielding fixed income security (e.g., corporate bonds). Fund flows since Bernanke introduced QE in November 2008 show equity inflows have trailed bond inflows throughout this bull market. (Exhibit 1)

Exhibit 1: Monthly Net New Cash Flows for Equity and Bond Mutual Funds

Source: FactSet, as of 8/27/2015. From 11/28/2008 - 7/31/2015.

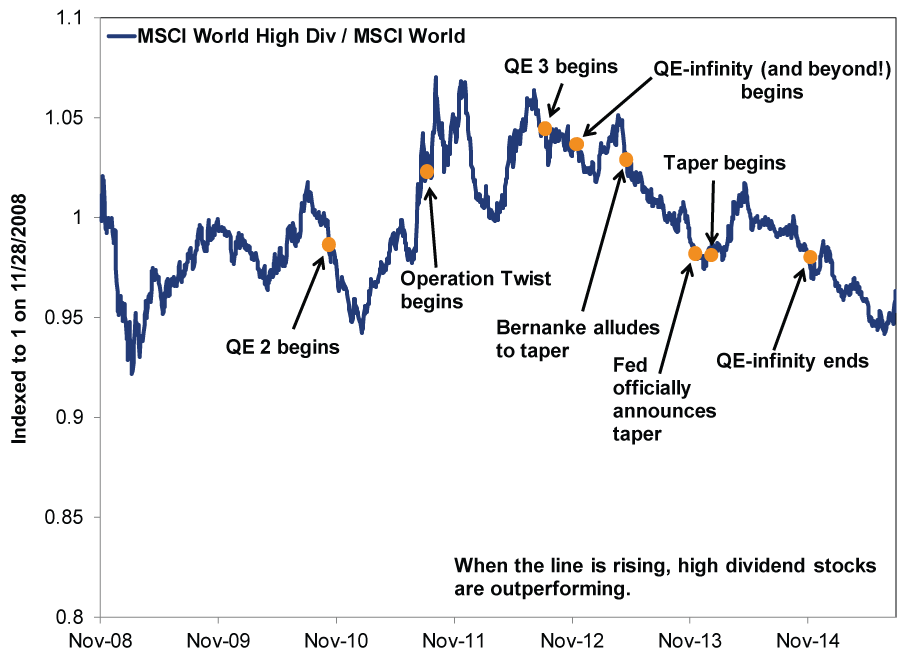

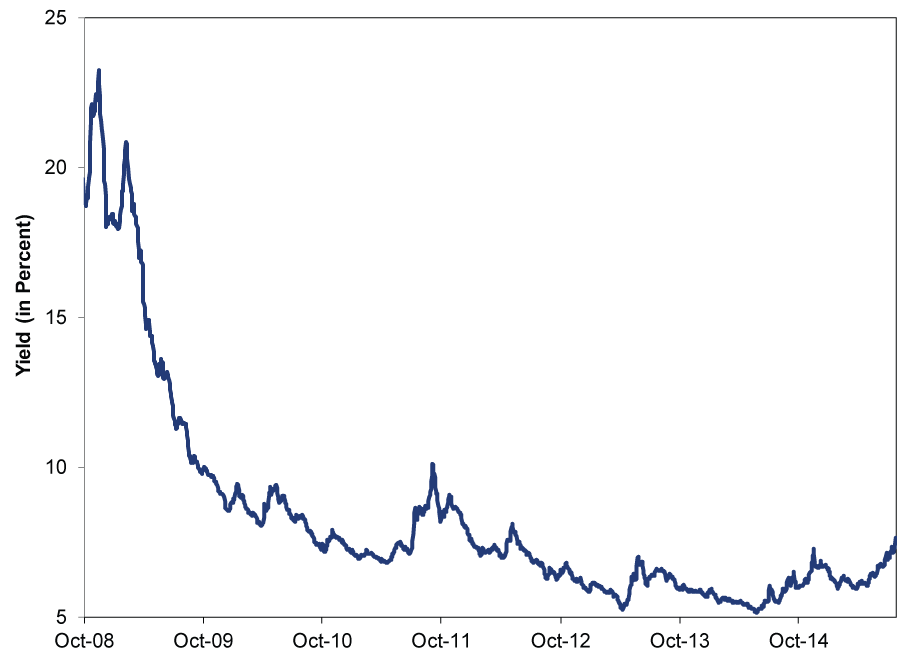

Now, while this doesn't include Exchange-Traded Funds-where equity inflows are higher-it seems a stretch to say investors completely ditched bonds for stocks during QE. High-dividend stocks' relative returns provide more evidence. If investors did yield-chase their way from bonds to stocks, these are the logical destination, and one would expect them to outperform wildly during QE. But as Exhibit 2 shows, they didn't. They had occasional bursts from 2009 through 2011 but largely lagged thereafter. Instead, corporate bonds appear to be the primary beneficiary, judging from the fact junk bond yields plunged to historic lows even as supply soared-demand was robust. (Exhibit 3)

Exhibit 2: MSCI World High-Dividend Yield Index Relative Returns

Source: FactSet, as of 8/28/2015. MSCI World High-Dividend Yield Index and MSCI World Index net returns, 11/28/2008 - 8/27/2015. Indexed to 1 on 11/28/2008.

Exhibit 3: US High-Yield Corporate Bond Yields

Source: St. Louis Federal Reserve, as of 8/27/2015. BofA Merrill Lynch US High Yield Master II Effective Yield, from 10/31/2008 - 8/26/2015.

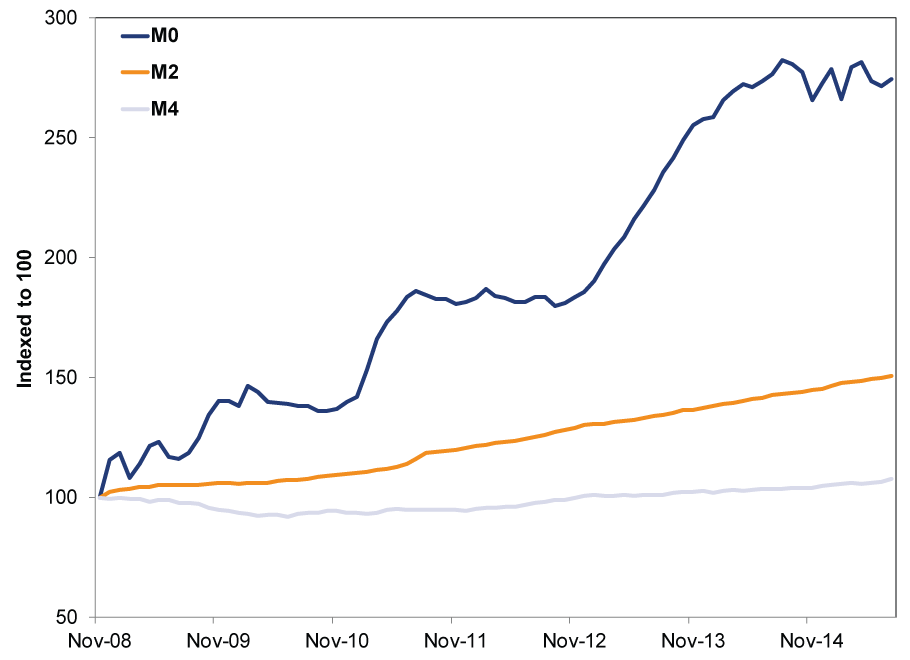

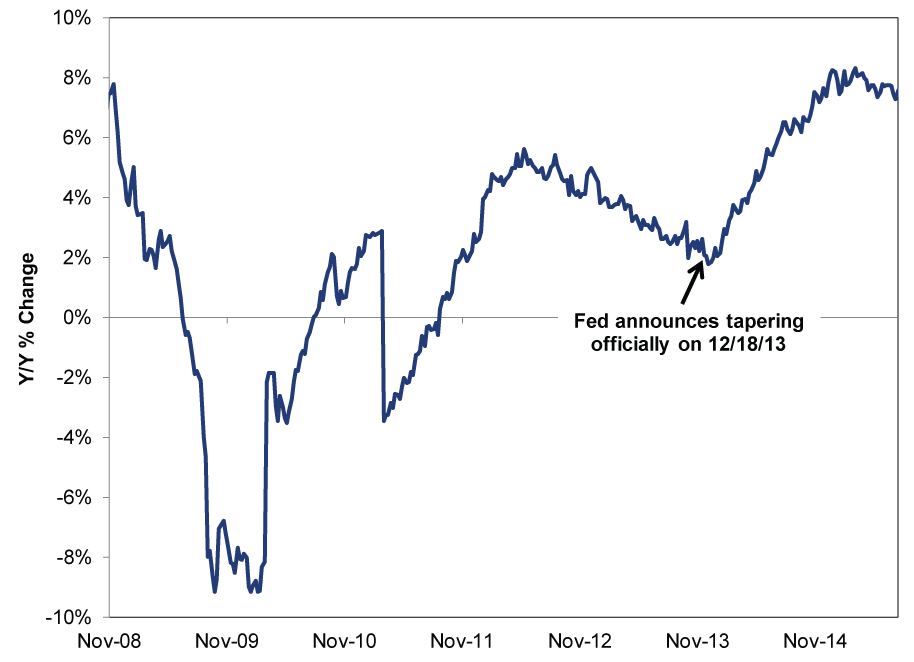

As for QE money going directly to stocks, this would require the new reserves to leave bank balance sheets. This could happen only if the funds backed a surge in new loans, which didn't happen since banks had little incentive to lend-because of QE. QE aimed to lower long-term interest rates and spur economic growth through cheaper borrowing costs and thus more lending. But with short-term rates already near zero, lower long-term rates flattened the spread between short- and long-term interest rates, aka the yield spread. The yield spread represents loan profitability (banks borrow at short rates and lend at long rates), and the flatter the spread, the less incentive banks have to lend-so they didn't do it much. For evidence QE didn't flood markets with cash, consider the divergence between narrow and broad money supply. (Exhibit 4) The narrowest, M0 (bank reserves, notes and coins in circulation) zoomed, but the broader M2 and M4 didn't. M4, the broadest measure, even contracted for a long stretch as lending slowed significantly. Incidentally, loan growth took off right as the Fed began tapering. (Exhibit 5) The data suggest all those built-up reserves mostly stayed idle during most of QE's lifetime-they didn't boost anything.

Exhibit 4: M0, M2 and M4 Since QE1

Source: St. Louis Federal Reserve and the Center for Financial Stability, as of 8/27/2015. From November 2008 - July 2015.

Exhibit 5: Total Year-Over-Year Loan Growth at US Banks

Source: St. Louis Federal Reserve, as of 8/26/2015. Loans and Leases in Bank Credit, All Commercial Banks, seasonally adjusted, weekly.

Overemphasizing returns since QE ended also misses how markets work. Markets price in all widely known information and move in advance of upcoming events, and QE's end was widely known long before it happened. In May 2013, then-Fed Chair Ben Bernanke alluded to winding down QE, and markets began discounting that eventuality then. Long-term rates rose a full percentage point from May through year end. Stocks pulled back a tad at first as end-of-QE jitters spiked, then soared. Once the Fed actually started tapering in January 2014, long-term rates fell and US stocks rose. The end of Fed bond-buying was already baked in. The claims that stocks are flat since it ended are basically gripes about a flat year preceding the current correction.

QE's track record doesn't inspire confidence, and we think restarting it would introduce unnecessary headwinds. Growth picked up in both the US and UK after QE ended. Japan, whose QE program is the biggest relative to GDP, remains economically stagnant. In our view, the US grew and stocks soared in spite of the Fed's bond buying, not because of it. In the unlikely prospect the Fed restarts QE, it probably wouldn't kill the current bull market or expansion-it didn't do so before. However, it would still likely be a drag on growth.

With the many false fears swirling about today-China hard-landing, weak global growth, China's equity markets, low oil prices, lagging Emerging Markets, China's devaluation, to name a few-we understand why folks view accommodative Fed monetary policy as one of the few positives. However, plenty of evidence suggests the Fed hasn't fueled the current bull market or expansion. We remind investors that this bull has plenty of fundamental support, and despite the market's most recent downturn, it doesn't need a boost from the Fed to rise higher.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today