Personal Wealth Management / Market Analysis

Serving Up Growth

The global economy keeps growing.

Consumers perusing various goods and services. Photo by Bloomberg via Getty Images.

Headlines still don't fully appreciate how well the global economy is doing. In the US, many still fear the economy can't handle interest rates north of zero. Skepticism towards the UK's expansion and the eurozone's recovery abounds. Yet, data continues showing otherwise-as has been the case throughout this expansion. A handful of high-profile, headline-grabbing weak spots aside, businesses around the world are growing, and stocks' economic fundamentals remain strong.

The broadest, timeliest example comes from July purchasing managers' indexes (PMIs)-surveys indicating how many businesses grew. Readings over 50 indicate more firms grew than contracted, which most presume signals economic expansion. While this isn't airtight since PMIs don't tell you how much each company or country grew, they do provide a timely sense of business activity-and July's numbers suggest firms are plenty busy. In the US, the Institute for Supply Management's (ISM) July Manufacturing PMI hit 52.7, a bit slower than June's 53.5. However, the Non-Manufacturing PMI jumped to 60.3 from June's 56.0, hitting a new high for this expansion. Notably, 15 out of 17 non-manufacturing industries reported growth, with only mining and "other services"[i] reporting contraction-this is broad-based. The forward-looking New Orders Indexes look good, too. Manufacturing hit 56.5 while Non-Manufacturing reached 63.8, suggesting firms must boost output to keep up with demand.

European PMIs also pointed to more expansion. In the UK, Markit's July Manufacturing PMI ticked up to 51.9 from June's 51.4, while its Services PMI reached 57.4-below June's 58.5 but still pretty robust. Eurozone PMIs-52.4 (vs. June's 52.5) in Manufacturing and 54.0 (vs. June's 54.4) in Services-also highlight the 19-member bloc's geographically broad growth. Services PMIs in Germany, France, Spain and Italy all rose, led by Spain, which enjoyed the fastest expansion at 59.7.

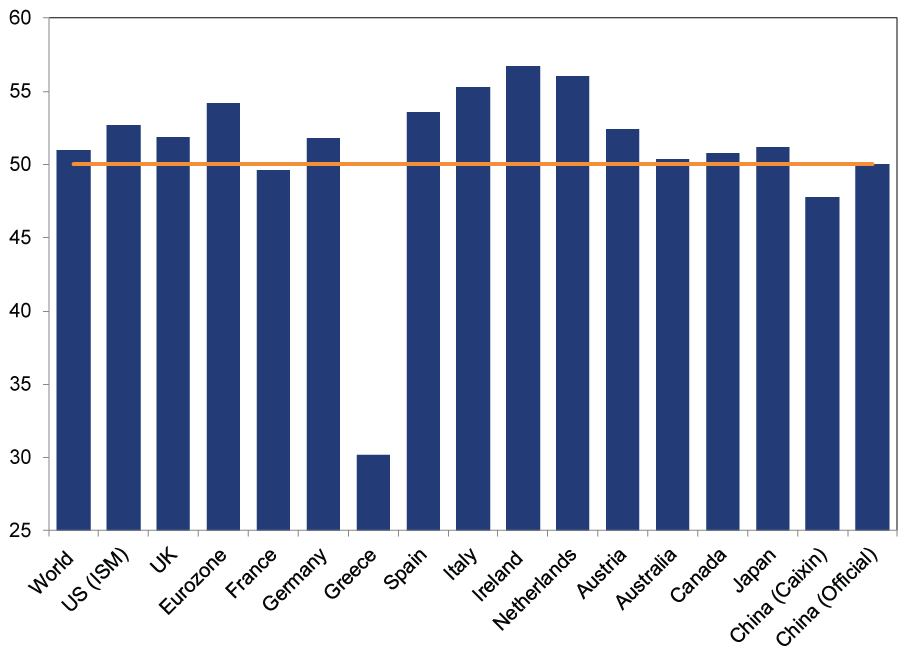

To highlight this expansion's breadth, here is a chart:

Exhibit 1: July Manufacturing PMI

Source: Markit, ISM and National Bureau of Statistics of China, as of 8/4/2015. "World" refers to the JPMorgan Global Manufacturing PMI.

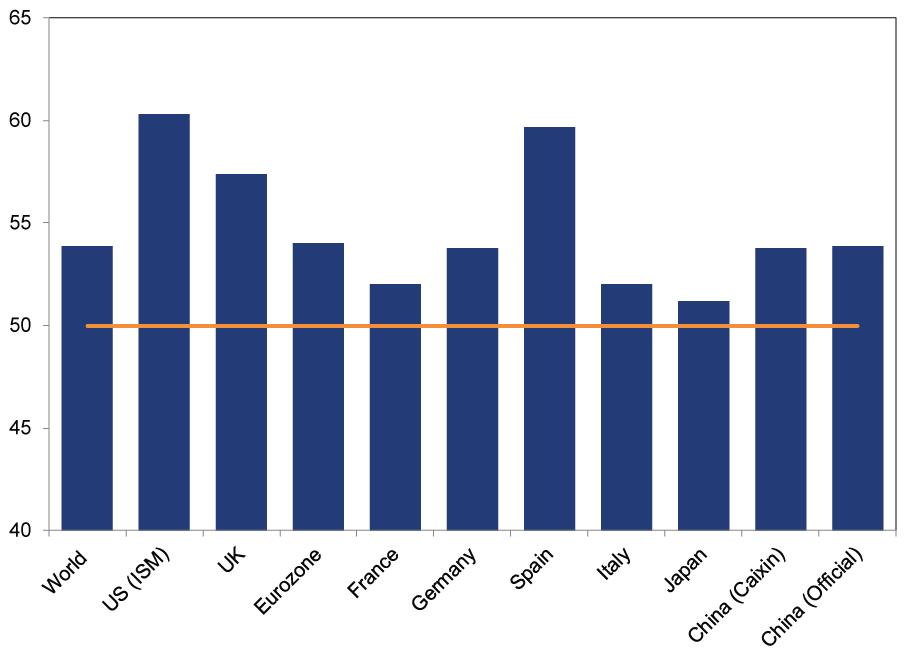

Most countries are over or very near 50-the obvious exception being Greece, which fell to an all-time low of 30.2 as capital controls wreaked havoc.[ii] Non-manufacturing/services PMIs look even better. (Exhibit 2)

Exhibit 2: July Non-Manufacturing (Services) PMI

Source: Source: Markit, ISM and National Bureau of Statistics of China, as of 8/4/2015. "World" refers to the JPMorgan Global Services PMI.

Though fewer countries have reported services PMIs, the levels are stronger-welcome news since the service sector comprises the biggest slice of most developed countries' economies. China, too! Though folks fret China's lackluster manufacturing PMIs, the service sector is increasingly dominant-both bigger and faster-growing than the country's heavy industry. If the biggest sector of your economy is growing the fastest, that's pretty good.

Other recent data confirm growth isn't a mirage. After US GDP accelerated in Q2, other evidence suggests the expansion continued. June factory orders rose 1.8% m/m. Take that headline figure with a grain of salt, at it is skewed by surging aircraft orders at the Paris Air Show. Excluding transportation, factory orders grew a milder 0.5% m/m. Bucking the recent trend, new orders for mining, oil field and gas field machinery rose 5.5% m/m, suggesting oilfield cutbacks paused at least temporarily-a theory further supported by rising rig count in late July. Core capital goods orders-nondefense capital goods excluding aircraft-rose 0.7% m/m, which should help ease lingering fears of weak business investment.

June trade data were more disappointing, but there were some mitigating factors. While imports climbed 1.2% m/m, exports slipped -0.1% m/m, and 2015's year-to-date export tally is below 2014's at the same point, heightening strong dollar fears. However, falling oil prices have contributed heavily here: About half the year-to-date decline comes from falling oil-related exports. Plus, that widely cited year-over-year decline isn't adjusted for inflation. Real exports, year to date, are 1.2% above the same period in 2014.

Other data from across the Atlantic, though mixed, largely point higher. UK goods export volumes surged 6.6% q/q in Q2, surprising many experts and defying fears the strong pound would hammer UK businesses. June industrial production was less rosy on the surface, falling -0.4% m/m, but that was largely tied to mining and quarrying's -3.8% m/m drop-perhaps a sign North Sea oil producers pulled back a bit after a renewed drop in oil prices took some of the shine off recent energy sector tax breaks. The narrower manufacturing gauge, a better indicator of UK factory activity, rose 0.2% m/m, snapping two previous monthly declines. However, production overall comprises less than 15% of UK economic output-while services comprises about 80%-so whether positive or negative, the impact here is limited.

In the eurozone, June's German factory orders jumped 2.0% m/m-up from May's -0.3% m/m and trouncing expectations for 0.3% m/m-a good sign for the export powerhouse. However, many focused on eurozone retail sales, which slipped -0.6% m/m (1.2% y/y) in June, renewing weak recovery fears. That seems premature to us. For one, monthly data are volatile, and blips happen. Retail sales still rose in seven of the past nine months. Plus, the decline wasn't uniform: Denmark, Ireland and France all reported growth. Besides, retail sales are a slice of total consumer spending. Services spending comprises a large swath. So rather than calling falling retail sales evidence of eurozone weakness, we're more inclined to call it a brief hiccup in a continued economic recovery.

Looking ahead, global economic prospects look good: See forward-looking indicators, like The Conference Board's Leading Economic Index (LEI). US June LEI rose 0.6% m/m, its 16th rise in the past 17 months. Similarly, the eurozone's June LEI gained 0.4% m/m, its eighth straight monthly rise. With many LEIs worldwide in a nice upswing, the global expansion looks likely to climb further-an underappreciated economic driver for stocks.

[i] "Other Services" literally are other services besides those categorized separately by ISM, ranging from Equipment & Machinery Repairing to Temporary Parking Services.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today