Personal Wealth Management / Market Analysis

While Greece Was Reeling

What else is going on in the world besides Greece?

For such a small country, Greece sure has hogged a lot of headlines this week. We're complicit, adding to the headline count yesterday and devoting five of Wednesday's 11 story blurbs to the Hellenic Republic. It's a fascinating topic and changes by the moment. But it is a big world, and a lot of non-Greek things have happened this week-things we reckon investors might like to know about. So here is a rundown of news you might have missed amid the Greek news deluge.

The Fed Didn't Raise Interest Rates

Ok, this one you probably saw. No big changes, no new forward guidance-just acknowledgment that growth has picked up since Q1, which most already suspected. The legendary "dot plot" of Fed people's interest rate forecasts showed they expect rates to rise more gradually than they anticipated three months ago. In her post-game presser, Chair Janet Yellen urged people to stop focusing on the timing of the first hike and think more about the pace of the overall tightening cycle-then told everyone not to read into the dot plots and reminded us it's all data-dependent. "It's data-dependent" is the rough translation of approximately half her answers, which seems like appropriate use of non-committal Fedspeak. Though she did slip once when discussing the eventual first hike, ruminating on the relative unimportance of the timing "whether it is September or December or March," which most assume means no hike in July.[i] And she made an odd reference to the Fed's desire to raise rates "gradually," which she helpfully (?) clarified as about one percentage point per year, or a quarter-point every other meeting. We suggest you not take that to the bank, given how her previous attempts at clarity, specificity and transparency have fizzled-she always seems to move the goalposts. Maybe the Fed indeed "wants" to follow this schedule, but wanting doesn't mean they will. Like the San Francisco Fed's t-shirt says, it's all data-dependent[ii].

With the IMF considering adding China's yuan to its reserve currency basket, expectations were high for China to lift capital controls by year-end to achieve full convertibility, a precursor for reserve currency status. Central bank Governor Zhou Xiaochuan fanned the speculation earlier this year, saying officials intended to liberalize interest rates and free up cross-border capital flows by year-end. Some feared this would be the first step toward dethroning the dollar as the world's favorite reserve asset (a false fear-see this for more). Others, like former Fed head Ben Bernanke, warned a swift opening could do more harm than good, causing big currency swings and foreign investment gyrations and destabilizing China's already-slowing economy. That seemed like a good reason to go slowly, which is what Chinese officials always said they would do, Zhou's comments aside. They confirmed that stance Wednesday, confirming opening the capital account "will be a gradual process." That seemed consistent with recent plans to launch a free-capital-flow trial in the Shanghai free trade zone only. Pilot programs there take a while to go national.

More People Are Running for President

And one of them, former Florida Governor Jeb Bush, pledged to restore 4% annual GDP growth. Folks, we don't have a dog in this fight. We have zero party or candidate preference, and we analyze the things they say and do solely in terms of market impact. And with that in mind, we encourage you not to assume a Jeb Bush presidency means growth speeds up, should he win. One, it's a long-term economic forecast-an effort fraught with peril that usually goes wrong, because the far future is full of variables and changes we can't imagine today. Moreover, the Federal government accounts for just 7% of GDP. Including state and local governments, the public sector oversees just 18.2%. The remaining 81.8% is the private sector, and the government has very little to do with growth there, for good or ill. Taxes and regulations matter, sure, but cyclical factors are often more powerful. There are simply too many variables at work for any politician, regardless of party creed, to say "let there be growth" and have it work.

A Federal Court Declared the AIG Bailout Illegal

Or partly illegal, anyway. And they didn't award any damages, lest they distort financial markets in the here and now, so this is mostly symbolic and, we suspect, an attempt to set precedent. In his decision, Judge Thomas Wheeler concluded that by seizing a 79.9% share of the company in return for bailout loans-without shareholder approval or compensation-the government committed an "illegal exaction" in violation of the Federal Reserve Act.

Some have theorized that this could end the age of bailouts, leaving banks to sink or swim without Uncle Sam's help forevermore, but we have our doubts. This was not a verdict against government aid. It was a verdict against aid that included forced seizure and the Fed firing the CEO. The Fed did this to appease worries that Wall Street was getting handouts. There are other ways to appease these worries, like lending at a penalty rate-as they did with most TARP funding recipients, who paid back just about every penny and then some. (The automakers, last we checked, haven't.) AIG's bailout was far, far stiffer than the rest. As Bloomberg's Matt Levine quipped last October, ousted CEO Hank Greenberg and his cadre of shareholders simply "wanted a nicer bailout." It seems the court agrees and thinks bailouts should be nicer from now on. The Fed and Treasury can marry toughness and niceness. Not that we advocate bailouts, mind you-we rather prefer the traditional playbook, whereby the FDIC does its thing when needed and strong banks buy the assets of failing banks. That's mostly how the Savings & Loan crisis faded, and it worked well then. We're just cynical and don't have faith that the powers that be truly believe the alleged problem of too big to fail has gone away.

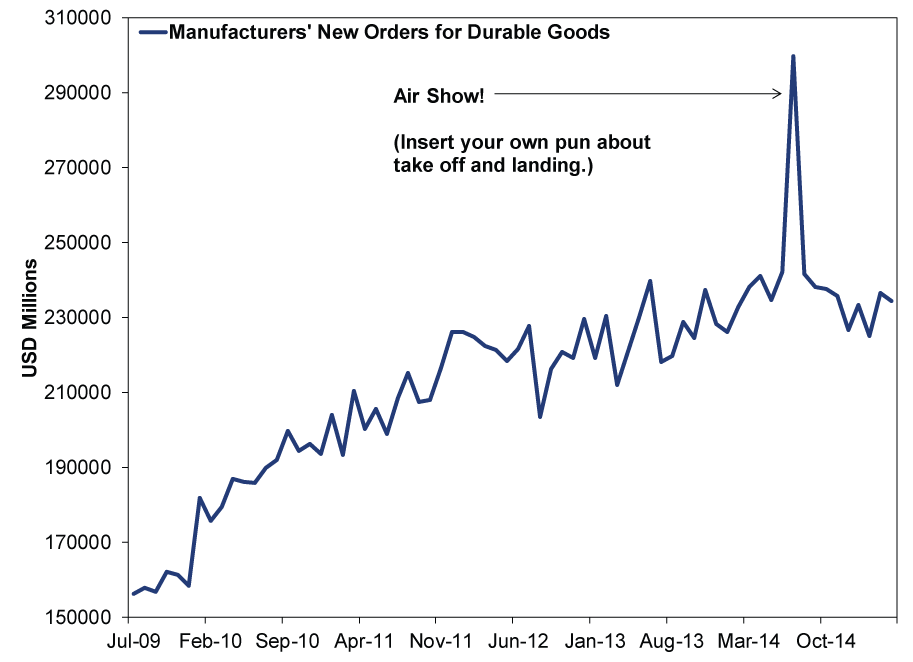

And both halves of everyone's favorite global airplane duopoly sold a lot of planes. We point this out because it could cause a big surge in durable goods orders, just as the Farnborough International Air Show in England did last year, when orders showed up in July's durable goods report (Exhibit 1). Neither that boom nor the double-digit drop that followed reflected the economy's true state. It was just noise. Any air show-related boom this time around will be similarly noise. Don't ignore durable goods or anything, but we suggest paying more attention to the core measure, which strips volatile aircraft and defense-related orders.

Exhibit 1: Durable Goods Orders in This Expansion

Source: Federal Reserve Bank of St. Louis, as of 6/17/2015. Manufacturers' New Orders for Durable Goods, July 2009 - April 2015.

Wheeeeee! UK wages rose 2.7% y/y in the three-month period from February to April. (Yes, the Brits report unemployment and wage growth on a rolling three-month basis.) Wages aren't a leading indicator for the economy or stocks, so don't read too much into this, but wage growth was long the missing ingredient from the UK's expansion. But it has trended up since mid-2014, and this is the fastest reading in years-nice confirmation that the UK economy remains on track. Hear, hear!

Shinzo Abe Received a To-Do List

Finally, Japanese Prime Minister Shinzo Abe's Regulatory Reform Council handed him a whopping 182-point list of policy recommendations. That isn't a typo, it really was 182. Japan has a lot of red tape, folks. Some of the measures are small, like paving the way for Airbnb in Japan and ending the 14-day limit on certain medical prescriptions. Others are bigger, like establishing a "financial settlement system for fired workers," which would remove a big roadblock to more flexible labor markets. Japan's byzantine labor markets are a huge headwind to recapturing that 1980s economic dynamism, and this proposal and related reforms face stiff opposition. Abe's Liberal Democratic Party tried to pass a raft of labor market measures last week, but the debate turned to fisticuffs, so they had to delay. That wasn't a typo either, there really was a scuffle, and the labor committee chief ended up in a neck brace. Abe's coalition has more than enough votes, in theory, to pass all this stuff, and Japan would benefit if they did. But doing so will take a lot of chutzpah, horse trading and political capital. It remains unclear whether Abe is willing to spend his political points on the economy instead of military matters, where most of his focus remains. This is a big reason why we suspect investors' hopes for Japan remain too high, with better opportunities in other countries.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today