Personal Wealth Management / Economics

The Base-Effect Bump Coming Soon

Detailing the base effects that will … umm … inflate some gauges of prices in the near future.

For most of the last two weeks, inflation worries and interest rate gyrations have dominated the financial press. So it was Thursday, as many investors watched a Wall Street Journal Q&A session with Fed head Jerome Powell. Many expected Powell to drop hints about how the Fed may (nonsensically, in our view) push back against rising long-term interest rates. He offered little on this front, though. However, in a refreshing turn, he did make some very sensible points about upcoming inflation data that we think investors would do well to take to heart now—ahead of next week’s US Consumer Price Index (CPI) release and those in the months immediately to come.

The comments we are referring to came early in the Q&A. Mr. Powell started by summarizing where the US economy is today, in the Fed’s estimation. After running through a recap of the Fed’s dual mandate to balance maximum employment and price stability, he discussed the state of employment. Then it was on to inflation. Here is an excerpt.

So right now inflation is running below 2 percent, and it’s done so since the pandemic arrived. We do expect that as the economy reopens and hopefully picks up, we’ll see inflation move up through base effects, which means just that the very low readings of March and April will fall out of the 12-month window, and also through a surge, if you will, in spending that may come as the economy fully reopens. And that could create some upward pressure on prices. The real question is how large those effects will be and whether they will be sustained or more transitory.

And I’ll just say that for several decades the U.S. and the world, really, economy have been in a low-inflation world, and low inflation is what people expect both here and around the world. For those expectations to change, businesses and people would need to believe that larger increases in prices would be repeated year after year, and we think it’s unlikely that these deeply ingrained low inflation expectations would suddenly change.

It is more likely that effects like the ones I described would be one-time effects as the one-time effects of the fiscal boost fade. We have the tools to assure that longer-run inflation expectations are well-anchored at 2 percent, not materially above or below, and we’ll use those tools to achieve that end.[i]

Intelligent people can and do disagree on the extent of future inflation pressure, the effect of inflation expectations and whether a potential rise in inflation will prove short-lived or not. But one point he raised is inarguable: “Base effects” are highly likely to inflate[ii] readings in gauges like the CPI and the Fed’s oh-so-loosely targeted Personal Consumption Expenditures Price Index. That base effect will fall out of the data—and we can pinpoint pretty much exactly when.

You see, the readings he is referring to are the typical year-over-year changes in gauges like CPI. A year-over-year change, for the uninitiated, compares the reported month’s index level to the level in the same month from the prior year, expressing the change as a percentage. Most often, economists cite this measure to smooth out potential near term wobbles and gyrations in shorter-term, month-over-month changes. But the trouble is, in smoothing out those wobbles, the calculation is rooted in year-old data.

This winter—and especially later this spring—that means the calculation is rooted in the depths of last year’s lockdown-driven contraction. That was an inherently deflationary event, as recessions normally are. When economies contract, lending and spending usually dry up—putting downward pressure on prices. 2020’s contraction was odd in many ways, but this held true.

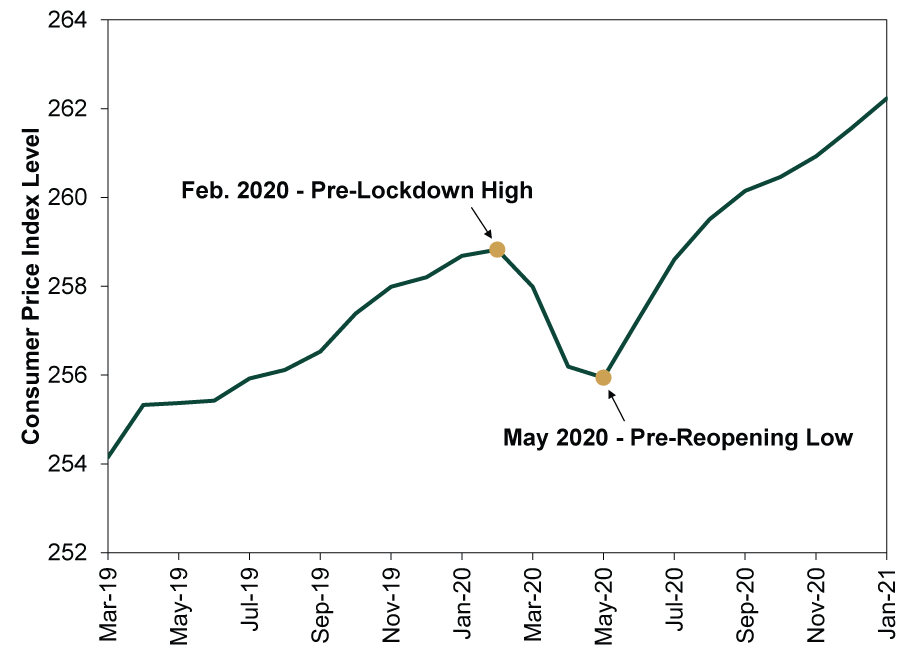

Consider CPI. Exhibit 1 plots the US CPI level since March 2019. Note the swoon in late spring 2020. That is the lockdown’s impact.

Exhibit 1: US CPI Level

Source: FactSet, as of 3/4/2021. US CPI, March 2019 – January 2021.

The decline in CPI after February means that, starting in March, year-over-year readings will be rooted in depressed levels. That is particularly true of May, when CPI was at its nadir. It will likely be done skewing the data by July, when CPI was only a hair below February 2020’s pre-lockdown high.

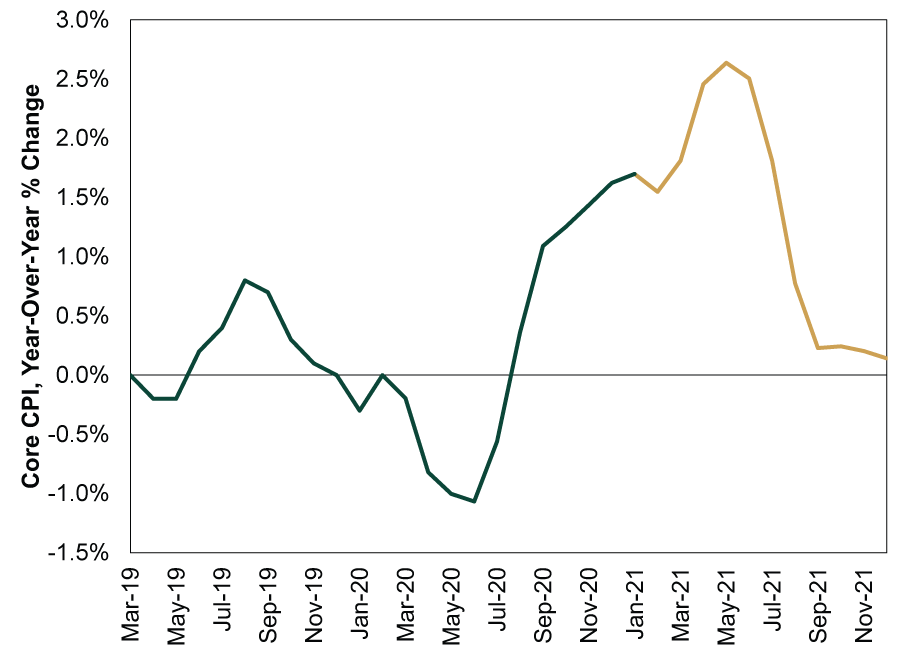

To see the impact of this consider Exhibit 2. In this, we are showing actual year-over-year inflation rates through January 2021, the latest reading available (green line). The yellow line holds January’s reading constant for the rest of 2021—a hypothetical way to see the base effect in action. Hence, in every month below, the hypothetical month-over-month CPI is unchanged, 0.0%. But that is far from the case in the year-over-year rate. Exhibit 3 shows the same using the core CPI—the gauge excluding food and energy to limit price volatility tied to non-monetary factors.

Exhibit 2: The Base Effect in Actual and Hypothetical Action

Source: FactSet and Math, as of 3/4/2021. Readings from February 2021 through December 2021 are hypothetical illustrations using no change from January 2021’s index level. This is neither likely nor our forecast. It is solely to reveal the base effect bump coming this spring.

Exhibit 3: The Base Effect in Actual and Hypothetical Action, Core CPI Edition

Source: FactSet and Math, as of 3/4/2021. Readings from February 2021 through December 2021 are hypothetical illustrations using no change from January 2021’s index level. This is neither likely nor our forecast. It is solely to reveal the base effect bump coming this spring.

The base effect skewing data higher isn’t a new phenomenon by any stretch. The 2008 financial crisis. The oil price crash in 2015 and 2016. Any time an extreme event temporarily depresses inflation gauges, it will inflate them a year later, all else equal. That isn’t earth-shattering news. It is just math. But it is math worth keeping in mind as the spring draws near and base-effect inflated readings start rolling in.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today