Personal Wealth Management / Politics

The Brexit Agreement’s Aftermath

Political turmoil that struck the UK cabinet Thursday highlights why we think getting any resolution to Brexit is better than no resolution.

Wednesday, the UK cabinet met to discuss the draft Brexit withdrawal agreement UK and EU negotiators reached Monday. After a raucous session, the cabinet approved the deal—advancing it toward EU and UK parliamentary votes. Thursday, however, it became crystal clear the deal’s cabinet approval wasn’t without costs. Turmoil ensued after several cabinet members—including, notably, Brexit Minister Dominic Raab—resigned. Brexit in name only, which is what most available details suggest this agreement amounts to, isn’t good enough for most euroskeptic ministers. Nor for many Conservative Party MPs, 23 of whom have submitted letters of no confidence in Prime Minister Theresa May as we write—if that number hits 48, which Westminster insiders claim is likely to happen by early next week, it triggers a confidence vote. Meanwhile, many in the opposition Labour Party, including former Prime Ministers Gordon Brown and Tony Blair, are renewing calls for a second referendum on Brexit. All this seems to be spurring volatility, with the pound selling off somewhat overnight Wednesday and small-cap UK stocks falling. But to us, this is just the latest bout in back-and-forth Brexit uncertainty. This agreement—and probably any agreement—would face significant opposition from some constituent group. As we noted Tuesday, it doesn’t clear all uncertainty. However, these political theatrics—and the market reaction—are yet more evidence that just getting Brexit over and done with will benefit Britain.

Equity markets’ reaction has been rather modest at this juncture. The FTSE 100 is basically flat since the cabinet turmoil erupted. The small-cap, UK domestic-focused FTSE 250 Index is down -1.5% since, as of this writing.[i] This doesn’t shock us, as the political backlash is neither surprising nor new. Headlines have warned for months that May might not be able to get a deal—any deal—through Parliament. Rumors of her political demise have raged since she lost the Conservatives’ majority in last year’s government. Surprises move markets, and we daresay nothing about the political reaction to her Brexit deal was a shock. Rather, it was a chain reaction many saw coming.

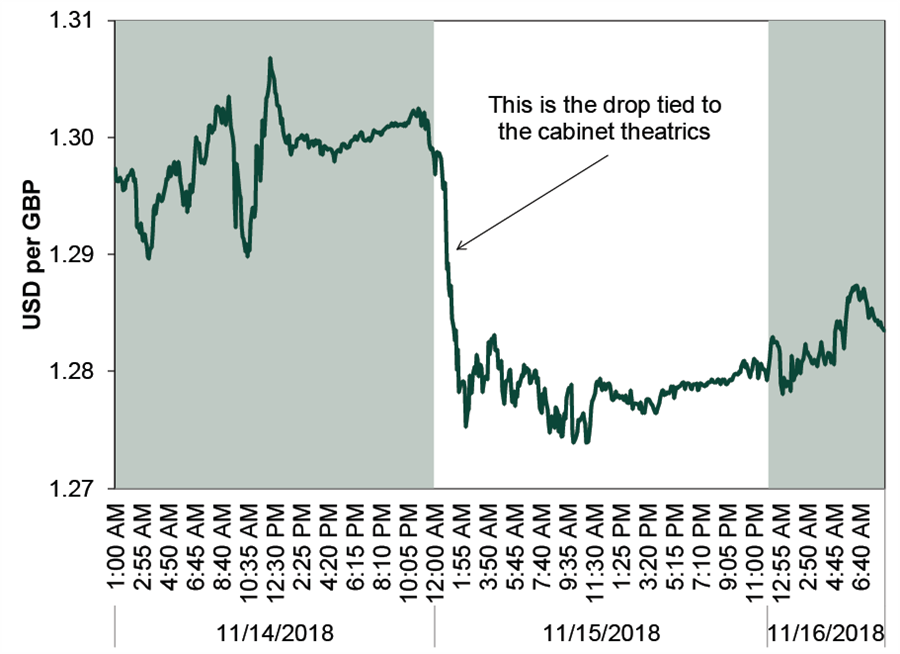

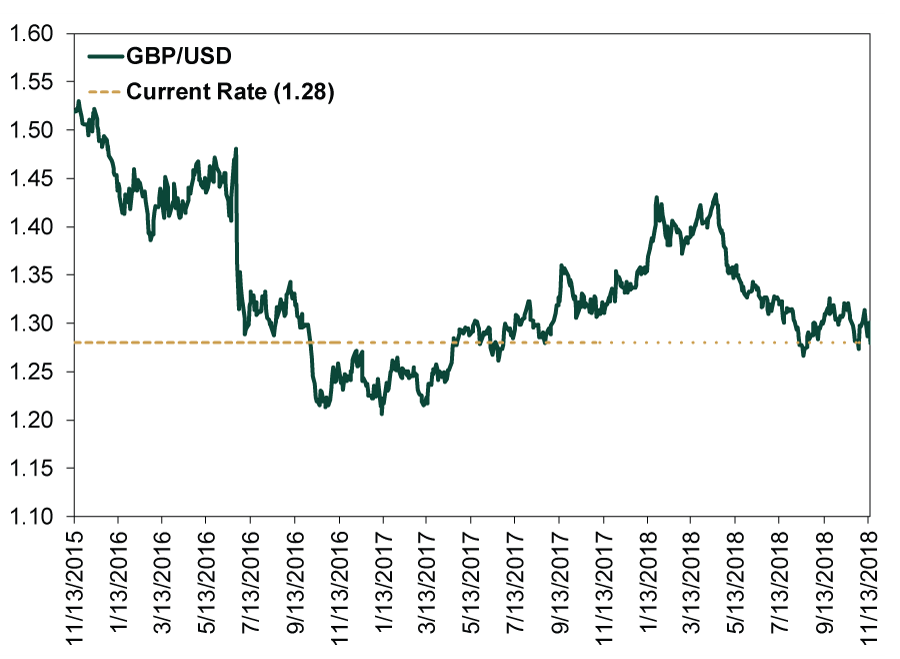

However, most media attention is on the pound, which stabilized Thursday and Friday after that initial overnight plunge. For example, Bloomberg reported Thursday morning that sterling was down “the most in 17 months.”[ii] However, we think this lacks perspective. Exhibit 1 shows the midweek selloff media referred to. Exhibit 2 shows Thursday’s volatility relative to movements in the last three years. It just doesn’t seem that significant at this point. The media reaction looks, to us, like myopia.

Exhibit 1: US Dollars per British Pounds Spot Exchange Rate, 11/14/2018 – 11/16/2018

Source: FactSet, as of 11/16/2018, 8:22 AM Pacific Standard Time. US dollars per British pounds, 11/14/2018 at 1:00 AM – 11/16/2018 at 8:20 AM.

Exhibit 2: The Pound’s Latest Drop in Perspective

Source: FactSet, as of 11/15/2018. US dollars per British pound, 11/13/2015 – 11/15/2018.

So what is in the deal that has politicians so roiled? It appears to render the Brexit vote a symbolic gesture, upsetting pro-Brexit Tories. Said differently, it is among the “softest” possible Brexit proposals—basically a Brexit in name only. Heck, as some cabinet ministers pointed out, Article VII says that UK will be called a “member state.” For one, the entire UK will remain in the EU’s customs union (but not the single market) indefinitely, pending a more permanent solution to the Irish border dispute. The difference here isn’t semantic. Being in the customs union means there wouldn’t be border checks on goods and there wouldn’t be tariffs between the EU and UK. However, being outside the single market means non-tariff barriers, investment restrictions and limits on the free movement of people may apply. Being outside the single market also means regulatory codes and standards can differ.

This move essentially kicks the can on crafting a targeted solution to the Irish border dispute so far down the road it doesn’t even put a date on it. There is no end date to this arrangement and no means for the UK to unilaterally cancel it without an “Irish backstop” being mutually agreed to. Being in the customs union means the UK will not be able to strike free-trade deals with third-party nations on its own. UK negotiators also agreed to align regulations to the EU’s on matters involving competition, social and environmental rules, limiting the freedoms it would get by being out of the single market. Britain’s big banking sector is in a bit of limbo, as the arrangement offered it few protections, leaving the EU free to decide on whether it considered the UK’s regulations “equivalent” or would require banks to take additional measures to operate in the EU. After the transitional period ends in 2020, the UK would have to pay the EU about £10 billion annually to extend these terms.

In addition, Northern Ireland would be required to sign up to the full EU customs code. This could risk May’s losing the support of Northern Ireland’s Democratic Unionist Party, whose support props up her Conservative minority government. So far, May claims the DUP hasn’t walked, though some of her MPs have spoken out loudly against the deal.

Realistically, any deal May struck would likely have faced opposition. The only thing that really sets this one apart is the way it displeases Brexiteer and Remainer MPs alike. It isn’t Brexity enough for the Leavers, and it doesn’t have enough benefits of EU membership to please the Remainers, as it morphs the UK into a rule-taker from a full-fledged member-state with veto power and political heft. This is the driving force behind the second referendum campaign, which argues citizens should get a vote on whether to leave under May’s agreed terms or stay. The likelihood of this happening is impossible to handicap, though the chatter is one more source of uncertainty.

The next step is for the EU to vote on the deal, which seems tentatively scheduled for November 25. Then the UK Parliament weighs in. While she seems to face opposition from all sides presently, it is possible May cobbles enough support together from pro-Remain Tories and more centrist Labour party members to actually pass it—presuming she stays in 10 Downing Street beyond next week, which many observers believe likely as no one else seems to desperately want her job in these present circumstances. But this, too, is impossible to handicap.

Ultimately, we likely won’t know until around Christmas whether the UK will exit under these terms, something else or the much-hyped “no deal” scenario, which remains on the table. Wiggles and big breaking news headlines like this week’s are a perfect illustration of why we think getting a resolution—any resolution—to Brexit is preferable to the limbo currently existing. The sooner European politicians get on with Brexit, the better for UK and EU stocks.

[i] Source: FactSet and Bloomberg, as of 11/16/2018. FTSE 250 Index price return, 11/14/2018 – 11/16/2018 (at 8:12 AM).

[ii] “Pound Falls Most Since 2017 as May’s Divorce Plan Rocked,” Charlotte Ryan and Shoko Oda, Bloomberg, 11/15/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Politics France Falls Into Political Purgatory … Again2025-09-12

-

Expert Commentary Fisher Investments Reviews Fed Rate Cuts2025-09-12

-

Expert Commentary Should Investors Hold Cash on the Sidelines?2025-09-11

-

Market Analysis Putting Stagflation Claims in Actual Context2025-09-11

Learn More

Learn why 185,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 6/30/2025

New to Fisher? Call Us.

Contact Us Today