Personal Wealth Management / Market Analysis

The Case Against the BoE’s Bond Buying

As the Bank of England expands quantitative easing, we revisit the program’s flaws.

As England re-enters lockdown, policymakers are trying their darnedest to stave off the worst economic effects. For Her Majesty’s Treasury, that means extending the furlough scheme, which replaces a chunk of workers’ lost wages, and other support programs. For the Bank of England (BoE), it means unleashing a fresh wave of quantitative easing (QE). Although well intended, we now have about a decade of evidence QE hurts economies more than it helps and isn’t stock market rocket fuel. We don’t think more QE will prevent a UK recovery or derail the nascent bull market, but in our view, it is a headwind against banks and value stocks, making it unlikely UK stocks meaningfully outperform any time soon.

QE’s goal is to stimulate lending by reducing household and business borrowing costs and giving banks more liquidity. As implied by the BoE’s name for QE, the Asset Purchase Programme, central banks create new reserves to purchase long-term assets from commercial banks. In the UK’s case, that means the BoE will buy an additional £150 billion worth of UK gilts between now and the end of 2021. Having that big of a buyer gobbling up that much supply drives bond prices up and yields down. Since sovereign yields are a reference rate for the rates banks charge on loans, the thinking goes, reduced borrowing costs will drive demand for loans, while the added reserves increase banks’ ability to lend, boosting loan growth and stimulating economic activity. That, at least, is the theory.

But since central banks began broadly experimenting with QE in 2009, reality hasn’t quite matched the theory. Rather, there is a large volume of evidence that QE doesn’t work as advertised. For one, when the central bank lowers long rates while pegging short rates near zero, it flattens the yield curve. Banks borrow at short-term rates, lend at long-term rates and profit off the spread, which represents their net interest margin on new loans. Therefore, the yield curve heavily influences loan profitability, which in turn influences banks’ incentive to lend. Since banks create most new money through lending, when loan growth sags, it weighs on broad money supply growth, robbing economies of fuel.

Every lending decision balances risk and reward. When lending is more profitable, there is more reward for risk, which broadens the pool of eligible borrowers. But when profits are smaller, it saps the incentive to lend to all but the most creditworthy. In our view, this explains why Senior Loan Officer Opinion Surveys showed banks broadly tightening credit standards during the 2009 – 2020 US economic expansion’s first several years.[i] QE had flattened America’s yield curve.

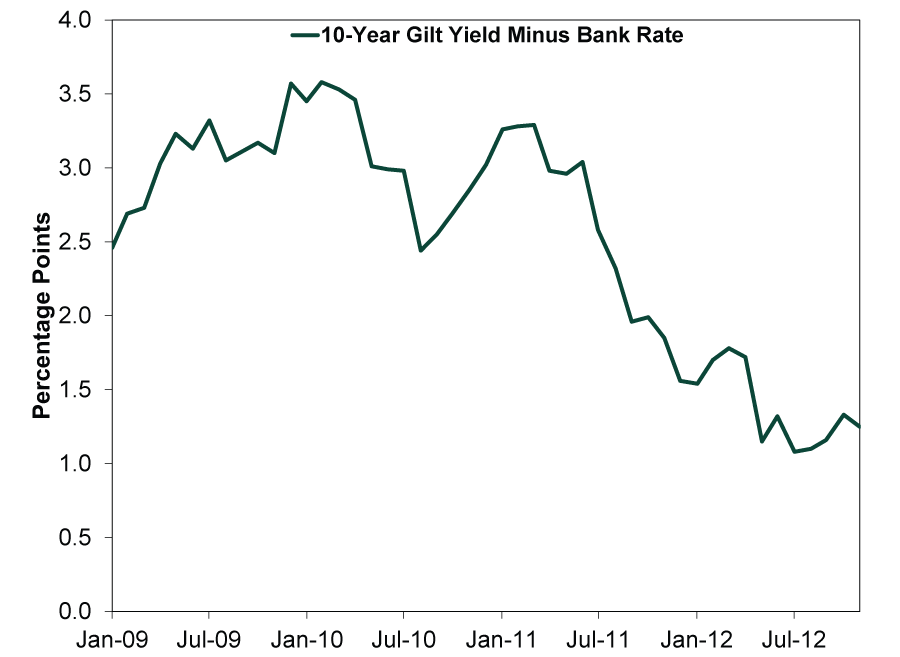

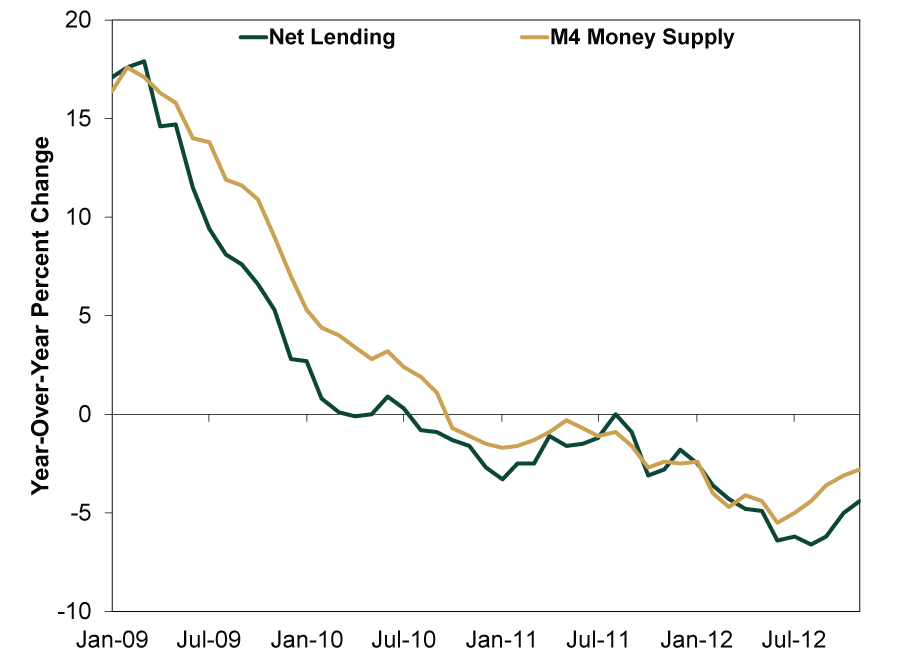

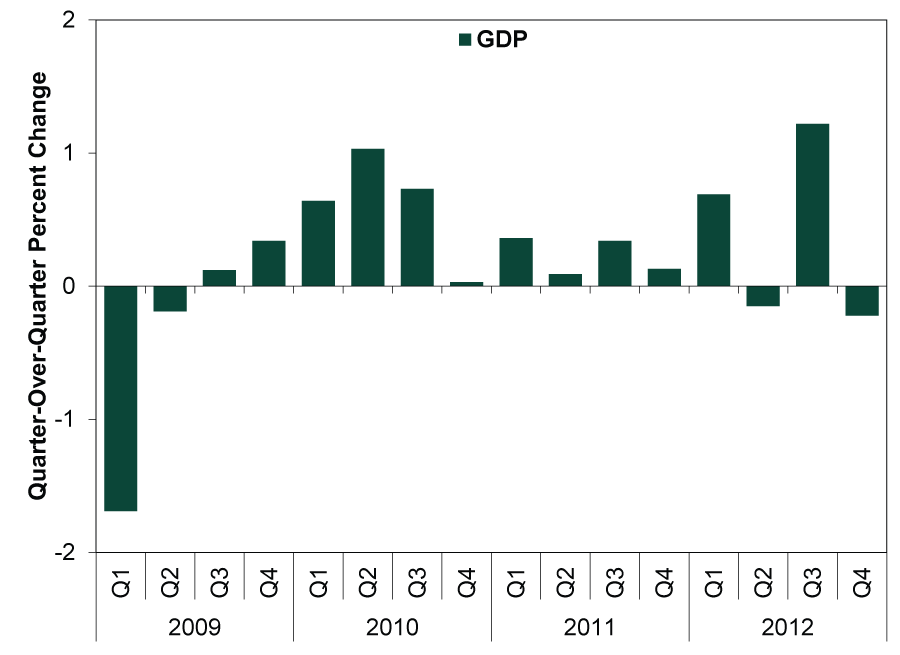

Beyond theory, consider hard evidence. When QE ran from January 2009 to November 2012 in the UK, growth stalled. During this time, the BoE quadrupled its balance sheet to £400 billion. But in the process, it flattened the yield curve (Exhibit 1), causing lending and broad money supply to shrink (Exhibit 2), which in turn weighed on GDP growth (Exhibit 3). After QE stopped, loan and money supply growth began to recover. GDP accelerated.

Exhibit 1: QE Flattened the Yield Curve

Source: FactSet, as of 11/11/2020. 10-year gilt yield minus Bank Rate, January 2009 – November 2012.

Exhibit 2: Loan and Money Supply Growth Turned Negative

Source: FactSet, as of 11/11/2020. UK net lending excluding securitizations to private sector and M4 money supply, January 2009 – November 2012.

Exhibit 3: GDP Slowed to a Crawl

Source: FactSet, as of 11/11/2020. UK GDP, Q1 2009 – Q4 2012.

The same occurred after the Fed and ECB tapered and then ended their QE programs. In 2013, the Fed began slowing its bond purchases, stopping them in October 2014. The US yield curve steepened in 2013 as the market priced in the Fed’s jawboning about tapering QE. Loan and money supply growth rose sharply, and GDP picked up in 2014. The eurozone experienced similar results in 2016 – 2018 when the ECB tapered and then ended its QE. US and eurozone stocks rose throughout tapering and after QE’s end.

Although we think QE is a headwind, it probably isn’t a huge negative. As the last decade showed, it may slow growth, but it doesn’t sink economies altogether. Also, lower long-term interest rates tend to cut government’s debt service costs, which in the UK’s case helps keep debt affordable even as it hits peacetime highs as a share of GDP.

But QE probably does make it unlikely value stocks, which get most of their funding from bank loans, lead any time soon. Banks themselves are also value-oriented, and the flat yield curve hampers them. This all adds particular headwinds to the UK’s stock market, which is heavy on value and Financials. That sector makes up almost 20% of the UK’s market value, nearly double the world’s share.[ii] In essence, a policy aimed at stoking UK growth is actually a headwind for both the real economy and the UK stock market.

We wouldn’t advise avoiding UK stocks altogether, as diversification calls for owning stocks in categories you expect to be out of favor. But we don’t view QE as a good reason to be bullish there or anywhere else. In our view, markets rise despite QE, not because of it.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today