Personal Wealth Management / Market Analysis

The Employment Twitch

The reaction to Friday’s US Employment Situation report was far from exuberant.

Looking for signs we’re not in a period of irrational exuberance? Look no further than the rampant skepticism following the release of Friday’s March US Employment Situation report.

Relative to expectations, the report was a flub. Nonfarm payrolls grew by 88,000 jobs—far fewer than the forecasted 190,000 hires. The unemployment rate fell by 0.1 percentage point to 7.6%, but a reduced workforce, not hiring, drove the decline. Private payrolls grew 95,000 while total government employment fell by 7,000 as a 12,000 decline in Postal Service employment (accounting for all public cuts) was partly offset by gains in other Federal, State and Local governments. (Calling into question theories today’s lower-than-expected figure was due to the sequester.)

If sentiment were actually Pollyanna-ish, it would be hard to find analysis making much of the less-than-stellar numbers. (Or pundits comparing Friday’s expected market reaction and cartoons of Wile E. Coyote falling off a cliff.) Yet in our perusal, we found ample coverage and analysis, with many suggesting the numbers raise the specter of slower growth ahead.

This is not the stuff of bubbles. In fact, many media sources seem downright irrationally pessimistic based on the figures. While unemployment can be personally devastating, it’s a late-lagging indicator with few forward-looking macroeconomic or broad equity-market implications. Historically, jobs follow growth and the stock market leads them both. Therefore, the notion a slower rate of hiring means much for economic conditions ahead confuses cause and effect.

And it overlooks other extant data points that simply don’t show anything to be concerned about. Also reported Friday, US total trade grew in February. Reported earlier this week, US factory orders surged 3% in February, the ISM manufacturing and services indexes were both nicely in expansionary territory, construction spending grew and March motor vehicle sales were 8% higher y/y. These data suggest growth continues and may have accelerated recently. Jobs data likely reflect very old economic conditions, not present or future. And, lest we forget, the figures show positive hiring—for the 30th consecutive month (37th for private-sector hiring), for that matter.

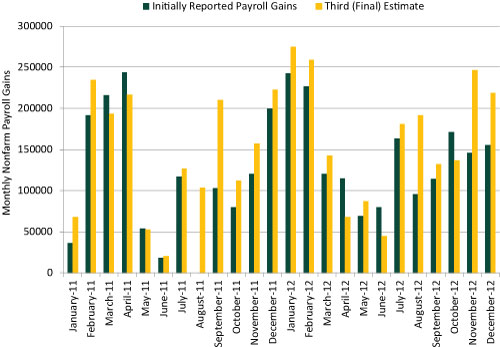

There’s just very little reason to think this one monthly report showing slowing hiring is anything other than mere noise. Noise that might be revised away! After all, in 2011 and 2012, the average revision between the first and third (final) nonfarm payroll gains figures was plus or minus 38,680 people—perhaps best illustrated by August 2011, when the initial report’s zero hires was revised to +104,000 by the final. (Exhibit 1)

Exhibit 1: Initially Reported Payroll Gains vs. Final (Third) Estimate

Source: Bureau of Labor Statistics.

(Note that change was seemingly NOT due to pulling hires from July or September’s estimates.)

Yet in the current, skepticism-laden environment, negative factors—whether correctly perceived or not—still catch many folks’ eyes. For weeks, many have noted the US economy could repeat 2011 and 2012’s pattern—though the mid-year growth-rate slowdowns seen then look like mere data variability considering both years logged positive jobs and economic growth throughout.

At a high level, the reaction to Friday’s lackluster report largely defangs fears of a bubble in the here and now. But taking a broader view also shows wiggles in employment data are typical. Don’t sweat one slower data point much more than that.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today