Personal Wealth Management / Economics

The Fed’s Diet Plan

The Fed's plan to reduce its balance sheet is amazingly gradual and the likely market impact amazingly small.

On Wednesday, the Fed raised rates for the fourth time in this bull market, no one cared, and everyone went home and enjoyed a summer evening walk. Oh, wait, sorry, Janet Yellen and friends also released their roadmap for getting all of those trillions of quantitative easing-related assets off their balance sheet, and made a loose pledge to start the process sometime this year. In other words, another Fed-related thing people have feared for years is about to finally happen. Yet markets took the news in stride, as they have most Fed "tightening" in recent years. Seems about right to us: Not only is shrinking the Fed's balance sheet not inherently negative for the economy (or stocks or bonds), but this is shaping up to be one of the slowest monetary policy moves in central banking history.

The Fed's plan pretty much matches what the bank has telegraphed for months: A slow, steady unwinding that doesn't involve outright selling anything-just not replacing bonds as they mature. We pointed out earlier this year that if the Fed simply let everything roll off its balance sheet as it matured, it would constitute a gradual move that shouldn't shock markets. Well, turns out they're going to go even more slowly, capping the amount allowed to roll off each month. From the official statement:

- For payments of principal that the Federal Reserve receives from maturing Treasury securities, the Committee anticipates that the cap will be $6 billion per month initially and will increase in steps of $6 billion at three-month intervals over 12 months until it reaches $30 billion per month.

- For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of $4 billion at three-month intervals over 12 months until it reaches $20 billion per month.

- The Committee also anticipates that the caps will remain in place once they reach their respective maximums so that the Federal Reserve's securities holdings will continue to decline in a gradual and predictable manner until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.

In other words, they'll start by letting $10 billion roll off each month, and increase the cap by another $10 billion quarterly until it hits $50 billion, where it will stay until the balance sheet has shrunk to where they want it, which isn't specified here. They also hedged a lot and left a few get-out clauses at the end of the statement, giving them plenty of wiggle room to stop the process or (goodness gracious please no) restarting QE if they think they need to.

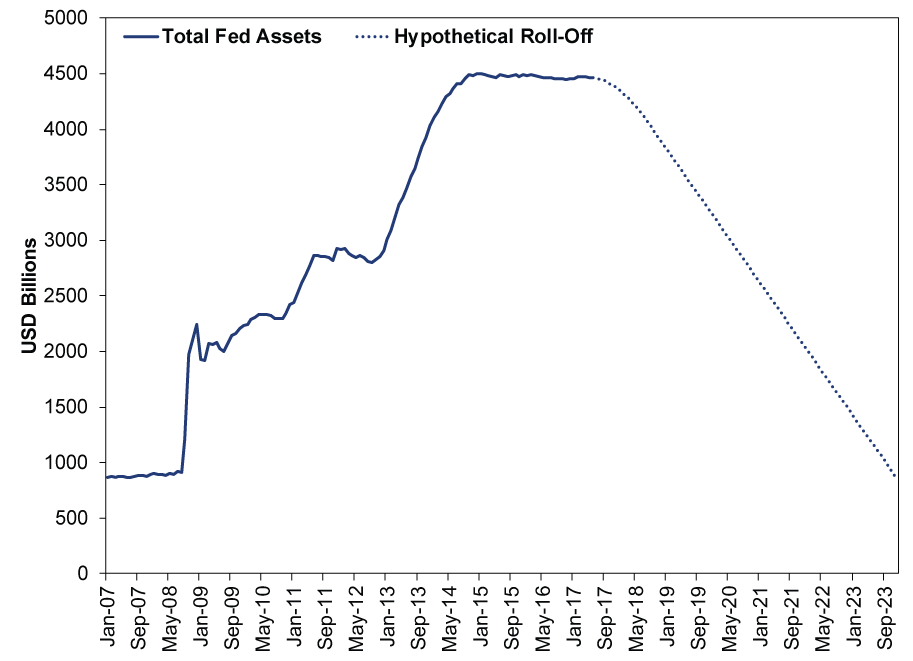

How all of this evolves is unknowable today, of course. But for fun and argument's sake, let's pretend they go with the maximum rate of shrinkage outlined above and don't have any interruptions. If that were the case, straight-line math tells us their balance sheet won't be back at pre-crisis levels until-wait for it-December 2023.

Exhibit 1: Balance Sheet Fun With Excel

Source: Federal Reserve Bank of St. Louis and Math, as of 6/15/2017.

That is...slow? Six and a half years is an eternity to markets, which usually don't look more than about 30-ish months ahead. Stocks also usually pre-price widely telegraphed, slow-moving changes, which are the very definition of "things that lack surprise power."

We'll have to wait and see how things progress and what future developments influence Fed decisions over this span-we aren't blindly declaring the next six years surprise-free and predictable. But for now it's notable how much pains the Fed is taking to ensure markets get plenty of time to discount all of this in advance. Fed people have been rumbling about shrinking the balance sheet for months. Recent meeting minutes said they'd release a plan soon. Now the plan is here, well before they actually start doing anything. And unlike the tapering of QE, which Yellen and her predecessor, Ben Bernanke, constantly said was not on a pre-set course, they have a pre-set course! How nice of them. Their blatant telegraphing likely has a lot to do with the fact that markets barely blinked, defying all those who fear shrinking the balance sheet means sucking trillions out of the US economy and dooming us all to some deflationary depression. As UCSD Professor James Hamilton quipped Wednesday afternoon, despite the past few years' headlines, markets make it clear "Fed balance-sheet reduction is not scaring anyone."

Nor should it. Those who fear Fed unwinding presume QE was wonderful stimulus that staved off recession from 2009 through 2014, when it ended. Some have fiddled with Excel to create charts alleging that the Fed's balance sheet during this span perfectly tracked the S&P 500, probably making Darrell Huff roll over in his grave. In reality, there was no relationship. Nor should there be, considering QE money didn't much make its way into the broad economy. Rather, it sat on bank balance sheets. In order for it to have had an effect, banks would have had to lend hand over fist. Yet loan growth was weak, and QE money idled as excess reserves, not required. If QE money backed a massive lending increase, those reserves would have been required. In reality, they sloshed around doing nothing.

As the Fed's balance sheet shrinks, so will banks' reserve piles. The Fed's statement says as much, and it seems they see this as sort of a science experiment: "The Committee expects to learn more about the underlying demand for reserves during the process of balance sheet normalization." In other words, QE has so distorted the market that we really have no idea how much extra cash banks would like to have on hand, above and beyond regulatory requirements. It seems like a foregone conclusion that banks would want something of a buffer, considering a) their desire to avoid another 2008 and b) regulators' occasional threats to treat banks as bankrupt if they simply go below minimum capital requirements, regardless of whether they've actually failed. How big a buffer remains to be seen. But in the meantime, what matters is that draining these excess reserves shouldn't amount to actual tightening, because they aren't backing loans. Basic logic dictates that if QE wasn't stimulus, erasing QE shouldn't be a wallop.

As for interest rates, 10-year US Treasury yields have risen about four basis points since the Fed's announcement-that is four hundredths of one percentage point. 0.04. It literally rounds to zero. That's a good sign bond markets-like stocks-discounted this a while ago. All else equal, as the Fed stops rolling over maturing bonds, bond supply would rise, which promotes higher rates. But the increase-$30 billion monthly in US Treasurys at maximum-is so tiny compared to the nearly $14 trillion (and counting) US Treasury market that it is difficult seeing this move the needle. Bond markets, like stock markets, tend to discount well-telegraphed, gradual supply shifts. Plus, the Fed is just one driver. New issuance matters, too. And so does demand, which is multifaceted. Could they change course and have a bigger impact? Sure, maybe. But that doesn't seem likely based on what we know now.

Ultimately, in our view, QE unwinding looks like the latest widely hyped Fed fear to be a big dud of a nothingburger in reality. Again, if their actions end up radically different or if financial conditions change markedly, this might be worth a second look. But for now, the likely market impact of all this is so small we can't believe this article almost hit 1300 words.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today