Personal Wealth Management / Market Analysis

The Red Scare

What should investors make of the Russian ruble's recent plunge?

Russia is a mess. The ruble is in free fall. Russian stocks are sagging. Inflation is surging. The central bank is projecting a nasty 2015 recession. Russian "President" (read: dictator; strongman; would-be tsar) Vladimir Putin-fresh off being named Russia's "Man of the Year" for the 15th consecutive year and finishing second to Janet Yellen in a poll seeking to identify the "Most Important Person to 2014 Capital Markets"-says a downturn is looming but will only last two years . While Russia likely has a tough time in the near future, this isn't 1998. And, 1998 or no, we don't see this as a real global economic threat.

Interested in market analysis for your portfolio? Our latest report looks at key stock market drivers including market, political, and economic factors.

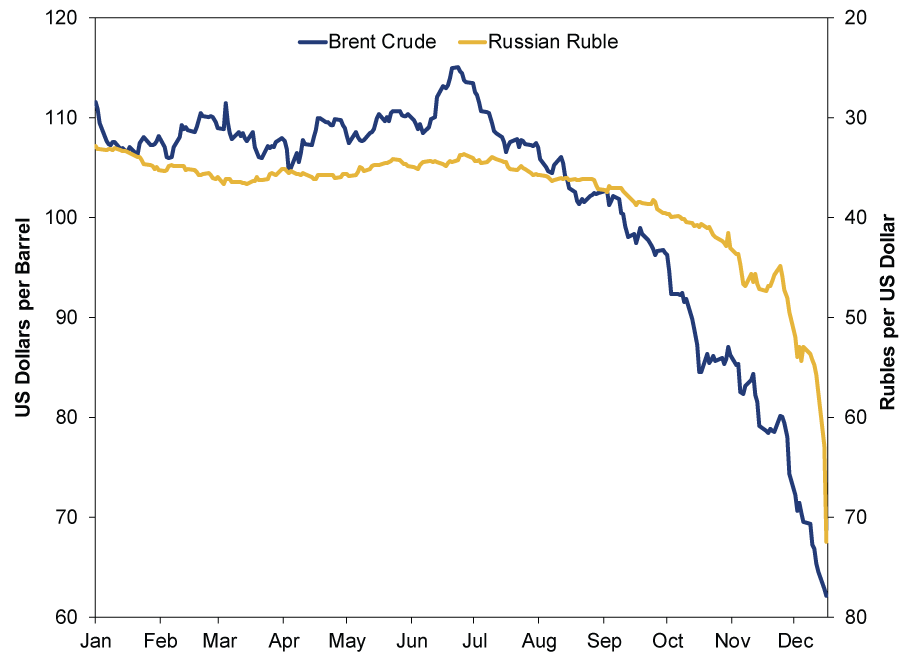

Here is the Reader's Digest version of the ruble's woes. At 2014's start, one dollar would buy you 33 rubles, hovering around that mark until late June-not coincidentally at Brent Crude's high for the year. As oil prices began falling in late June, the ruble started weakening (Exhibit 1). Falling oil prices aren't good for an oil-dependent economy.

Exhibit 1: Brent Crude Price and Russian Ruble in 2014

Source: FactSet, as of 12/17/2014.

To stem the ruble's depreciation, the Central Bank of Russia (CBR) raised its key interest rate several times. Risk and reward-central banks seeking to shore up currencies often raise rates to attract yield-seeking speculators[i] and keep foreign capital from fleeing. After starting the year at 6.5%, the CBR raised the key rate to 9% in July (from 8.5%), 10.5% in November and 11.5% on December 12. Yet the ruble kept sliding.

Monday, things got really bumpy. The CBR revised its 2015 projection of flattish economic growth, admitting GDP could contract by as much as -4.7% if oil remains near $60 a barrel. Which seemed obvious to us, but the CBR's realism seemed to take currency markets by surprise-the ruble plummeted 9%.[ii] In response, the CBR raised its key rate to 17% after midnight Monday, a move designed to "shock and awe." Yet the ruble dropped again Tuesday-by a whopping 15%. One dollar now buys you 73 rubles-a 55% drop this year.[iii] Bankers report little demand for the currency, even with rates at 17%, and fears now range from capital controls (and the potential panic) to the crisis' fallout. But while Russia's situation isn't good, it also isn't a 1998 repeat either.

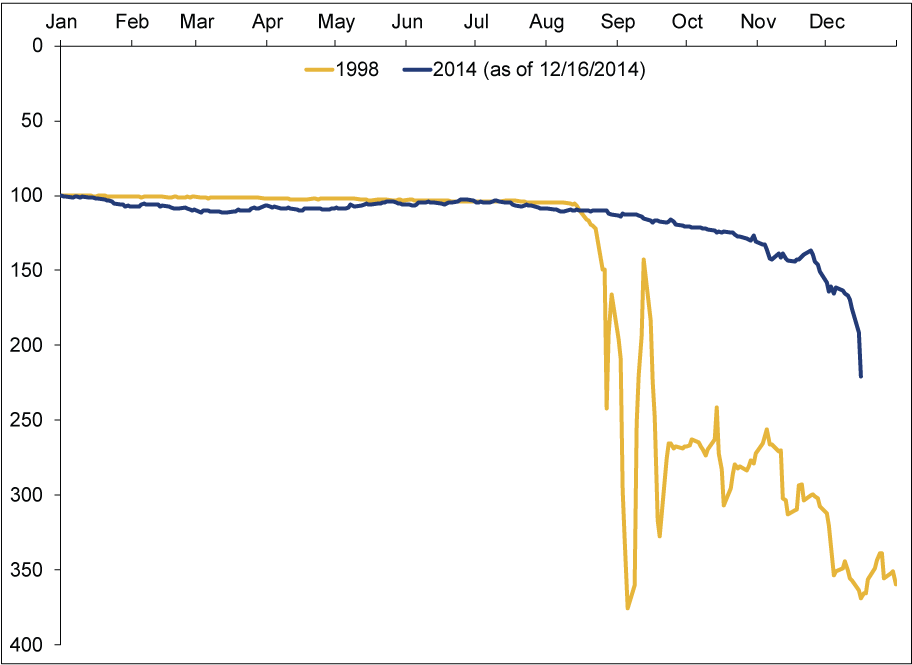

Here is a chart.

Exhibit 2: 1998 Ruble vs. 2014 Ruble (Indexed to 100)

Source: FactSet, as of 12/17/2014.

Like 1998's rollercoaster, the current drop has been sharp. (Though not quite as sharp as then, mind you.) In 1998, Brent Crude's price fell 42% from late January to late December.[iv] In 2014, it has dropped about 46% in about half the time.[v] In both cases, falling oil whacked Russia's economy.

Yet critical differences separate then and now. In the 1990s, many Emerging Markets (EM) economies (like Russia) pegged their currency to the dollar-hence the near flat line in Exhibit 2 before August 1998. While pegs seemed like a great idea-protecting economies from exchange rate fluctuations-they are inherently unstable. The dollar was ripping strong in the late 1990s, particularly against the Japanese yen-a major trading partner for Asian nations. Hence, the dollar pegs became difficult to maintain and led to the 1997-1998 "Asian Contagion," as one pegged nation after another came under pressure.

Russia was no exception. As currency began fleeing and the ruble started its precipitous drop, the CBR countered with rate hikes. In May 1998, the CBR hiked overnight rates from 30% to 150% in eight days. That's a far cry from Tuesday's 6.5 percentage point hike. It also burned through forex reserves in a futile attempt to bolster the ruble. But in August, Russia gave up and lifted the peg. The ruble collapsed. Russia defaulted. Global markets corrected.

Today's Russia doesn't face all those issues. For one, most EM nations-Russia included-don't peg to the dollar. Its debt isn't as onerous either. Back then, $45 billion in debt service requirements due by year-end 1999 dwarfed the $17.8 billion in international reserves. In addition, the government was running a budget deficit of roughly 8% of GDP. Russia needed to tap markets then. It doesn't now. Today, most estimates put Russia's public and private foreign debt due by the end of 2015 at $132 billion-a figure covered by the country's $419 billion[vi] in international reserves (built largely due to the 1998 experience). Given the country spent about $90 billion through November 2014 both servicing debt and defending the ruble,[vii] the likelihood of a default is low-unless Russia chooses to do so.

As for market impact, Russia's troubles contributed to a roughly 20% correction in US and global markets from July-October 1998. And it's possible Russian woes trigger still-more volatility in global markets today. Corrections are sentiment-driven, and they can happen for any reason or no reason. Yet just because one happened in 1998 doesn't mean one happens now. And! As massive as the 1998 global correction was, it didn't stop the decades-long 1990s bull. Global markets finished the year up 24% and the bull didn't peak until March 24, 2000.

Some fear Russia's problems may spill over to other countries-"contagion." While similarly politically dysfunctional and commodity-reliant nations like Argentina and Venezuela face pressures, outside this cabal of nations, the impact is likely limited. For one, it isn't like commodity-based Emerging Market countries have led the global expansion-or bull market-the last three years. They've largely floundered. But also, consider other EMs. China, Taiwan and South Korea, for example, export a ton of goods, like electronics. They, along with other EMs like India and Turkey, import a lot of commodities-so lower Energy input costs would theoretically be a benefit. There is a big difference between countries with dominant commodity-oriented sectors getting whacked and an EM-wide crisis.

At a smidge under 3% of global GDP, Russia's woes aren't much of a global economic drag, and we don't see this as a stumbling block for the global bull. Now, there are some ancillary concerns regarding how Putin reacts to the pressure from a geopolitical perspective. But that's all speculation at this point. And, as we've written, geopolitical events must be massive and surprising to have a lasting, material impact on stocks. Overall, we'd suggest this is an example of a very localized issue-a real one-but one unlikely to cause much lasting trouble globally.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors.

[i] We use this word without negative connotation.

[ii] FactSet, as of 12/16/2014.

[iii] Ibid.

[iv] Ibid. From 1/29/1998 - 12/21/1998.

[v] Ibid. From 6/23/2014 - 12/16/2014.

[vi] Central Bank of Russia, as of 12/5/2014.

[vii] Per the Central Bank of Russia, international reserves were approximately $510 billion as of 12/31/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today