Personal Wealth Management / Market Analysis

The Spring Swoon’s Swan Song?

April’s unemployment report should quell some skeptics’ spring swoon fears.

It’s perilous to hinge your market outlook on any one statistic, much less any one data point in any single series.

Last month, March’s Bureau of Labor Statistics (BLS) Employment Situation report led some to fear the US economy was headed for a slowdown—what some termed, a spring swoon. But those who latched on to the data point as justification for a skeptical view of stocks and the economy may be a bit befuddled now.

As we reported, March’s report was initially a flub—nonfarm payrolls grew by only 88,000, far fewer than the 190,000 expected. And the unemployment rate fell by 0.1 percentage point to 7.6%—but the decline was mostly attributable to folks leaving the workforce, not employers hiring.

In April, however, the report was noticeably better. On a monthly basis, total nonfarm payrolls grew 165,000—easily topping analysts’ estimates of 145,000. All of the gain was from the private sector (excluding government cuts, payrolls grew by 176,000). Comparing April 2013’s initial report to April 2012 shows 2,077,000 more folks are on nonfarm payrolls today. The gain is an even bigger 2,166,000 when government cuts are excluded. The unemployment rate fell slightly, by 0.1 percentage point to 7.5%. Finally, March 2013’s figures were revised up from that 88,000 initial report to 138,000—not gangbusters, of course, but not quite so slow. In addition, February’s 268,000 hires were upwardly revised to a solid 332,000 monthly hires (319,000 private sector hires—the second best month in the current expansion).

Also in April, retailers, whose March job cuts had led some to speculate the payroll tax cut was wreaking havoc on Main Street, rebounded sharply—recouping March’s cuts plus some. The civilian labor force increased incrementally—suggesting April’s slight dip in the unemployment rate was not caused by folks leaving the workforce. It was likely caused by hiring.

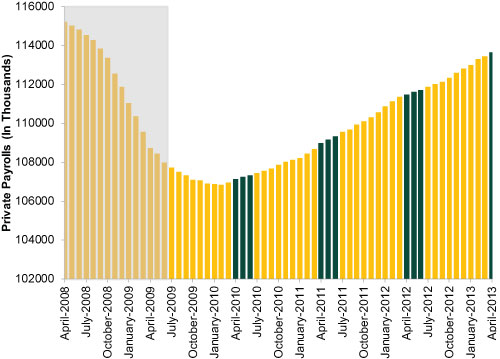

All in all, it’s a decent report and has some suggesting this year’s spring swoon is off. But also, what many may miss is that two of the prior three years haven’t had much of a swoon at all. As the Wall Street Journal noted in advance of today’s report, many fears of slowing hiring are underpinned by the notion we’ve seen a slowdown in the past few years. But, after revision, it’s only happened once. Moreover, all this talk is about a slowing rate of private payroll growth, as illustrated in Exhibit 1. (Spring months in the expansion are, appropriately, shaded green.)

Exhibit 1: Private Nonfarm Payrolls (In Thousands)

Source: US Bureau of Labor Statistics, April 2008 – April 2012 (first estimate). US recession shaded gray, green bars are spring months (April-June) during the present economic expansion.

It’s a bit out of place to fear the forward-looking market or economic ramifications of unemployment, since it’s a late lagging economic data series. It makes equally little sense to upwardly adjust your economic or market outlook today based on it. But spring-swoon skeptics citing March as supporting evidence can’t have it both ways. That April’s initial report was better than March’s doesn’t really tell you much, except that this lagging indicator has a volatile growth rate—tautology, to an extent. Perhaps that volatility means slowing growth is ahead. Perhaps there’s even a correction—a short, sharp down move amid a broader bull market—lurking. But we believe the broader trend for the economy, markets and payrolls is higher for the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today