Personal Wealth Management / Market Volatility

The Young Bull’s First Correction?

How we think you should approach what may be this bull market’s first correction.

Stocks had another rocky day on Monday, with the S&P 500’s -1.2% drop bringing it -8.4% from its September 2 high—nearing correction territory.[i] (Corrections are sharp, sentiment-driven drops of around -10% to -20%.) But in a fresh twist, Tech and Tech-like stocks didn’t lead the way down. Instead, Financials took the reins as investors punished banks over allegations of money laundering published by a group of investigative journalists. Beyond that, news featured more of the same: jitters over oil prices, potential new lockdown restrictions and all things election-related. Our opinion of headline news items hasn’t changed: We think all are too widely known, too small or too sociological (meaning, disconnected from economics or markets) to impact much beyond investor sentiment. These are the kinds of stories you get in a correction, not at the beginning of a bear market, in our view. Corrections begin at any time, for any or no apparent reason. While they can be painful to endure, they are normal. In our view, reacting to one is probably more detrimental to your long-term goals than staying put.

Same goes for reacting to big stories like this week’s sweeping money laundering allegations, which ensnared dozens of banks globally. Investigative reporters obtained access to suspicious activity reports banks submit to regulators when they suspect a large transaction relates to illicit activity. In many cases, the banks reportedly executed the transactions anyway, fueling accusations that they are winking at money laundering instead of trying to curtail it. Headlines warn banks will eventually face regulatory fines because of this, but we think this is quite speculative. For one, these submissions aren't proven cases of fraudulent activity by bank customers. They are actions banks flag to regulators, who may or may not use them to open a broader investigation. In some cases, regulators may inform banks not to take action blocking illicit transfers as part of a follow the money operation. Media allegations of bank wrongdoing are also common, and many don't lead to regulatory action. In our view, it is wildly premature to presume this story leads to material action dinging banks’ profits or ability to transact globally.

As for broader volatility, it isn’t unusual for one or two (or three) big stories to collide in a correction—regardless of how young a bull market is. Considering we are just two days shy of this bull market’s 6-month anniversary, we suspect many investors—some who disbelieve in this bull market anyway—fear that this is too soon to be just volatility or a correction. But as Exhibit 1 shows, if this pullback does reach correction territory, it would not be the earliest one ever to arrive—despite its coming on the heels of the fastest-ever bear market and fastest-ever recovery. Three other corrections arrived sooner, less than two months after their respective bear market lows.

Exhibit 1: A Look at the First Correction in Every Post-War Bull Market

Source: Global Financial Data, Inc. and FactSet, as of 9/21/2020. S&P 500 price returns in the periods shown, with 30.5 calendar days used to approximate 1 month. Price returns used in lieu of total due to data availability.

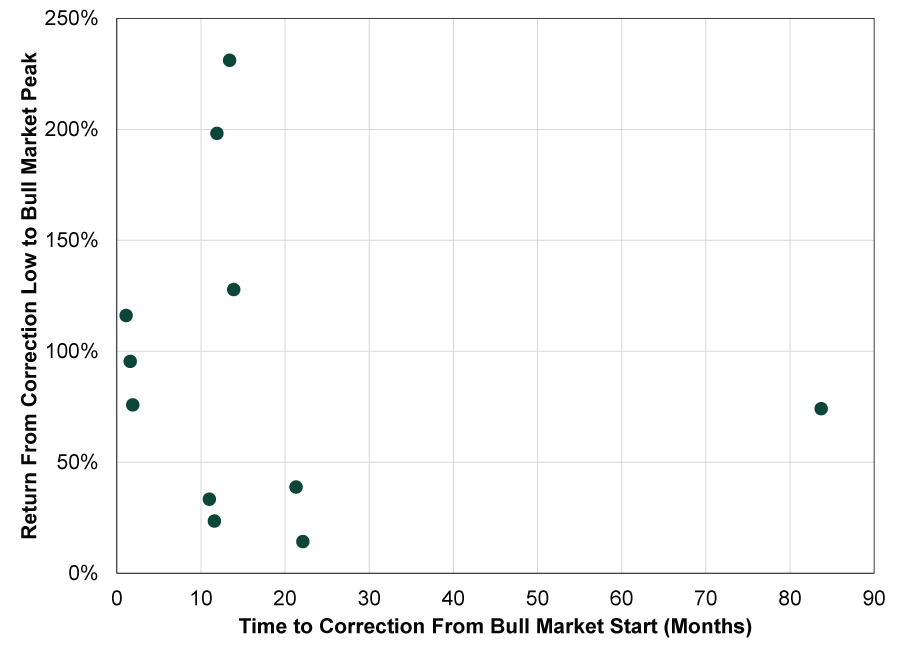

As the table also shows, the length of time it takes a bull market’s first correction to arrive isn’t telling. Not about the correction’s length, not about its magnitude and not about the returns over the rest of the bull market. Exhibit 2 shows this last item another way, using our least-favorite chart format ever: the dreaded scatterplot. We like scatterplots best when they show zero relationship, and that is the case here. Note how there were five corrections that began a year or so after the prior bear market ended. The returns from their low to the bull market’s eventual peak ran the gamut.

Exhibit 2: Nothing About Corrections Is Predictive

Source: Global Financial Data, Inc. and FactSet, as of 9/21/2020. Based on S&P 500 daily price returns, 6/13/1949 – 2/19/2020, with 30.5 calendar days used to approximate 1 month. Price returns used in lieu of total due to data availability.

About the only consistency is that, with one exception (1990), big returns loom after the correction’s end—sometimes really big returns. Reaping these returns is critical to earning stocks’ long-term returns, and reacting to a correction or near-correction is very often a path to missing gains. Because corrections start without warning, once you realize you are in one, it could very well be nearly over. Selling then would lock the declines in and leave you with a critical question: When do you get back in? Corrections usually end as suddenly and randomly as they begin. By the time you deem markets stable, stocks could be up 5%, 10% or more off the low. That basically amounts to selling low and buying higher. Those missed returns can add up over time, making your long-term goals that much harder to reach.

Therefore, in our view, the best course of action when sudden volatility strikes is to do nothing. Be patient, keep your long-term goals first in mind, steel your nerves, and don’t react. Remember corrections are normal and accepting their temporary declines goes hand in hand with reaping stocks’ long-term rewards.

H/T Fisher Investments Research Analyst Chase Arneson

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today