Personal Wealth Management / Market Analysis

Three Backward-Looking, Not-So-Predictive Valuations Are High

The US Treasury makes a market forecast.

Evidently, Uncle Sam wants YOU ... to be worried stocks are overvalued. At least, that's the impression we get from a recent report by the US Treasury's Office of Financial Research, "Quicksilver Markets," which has trickled through mainstream financial publications since it was published March 17. Citing three ... ummm ... unconventional valuations, the report warns US stocks are "nearing extreme highs," so look out below. Folks, this warning and its supporting evidence are about as useful to investors as a whale's hip bone-bizarrely calculated backward-looking ratios do not predict stocks.

The report does point out that traditional valuations, like the 12-month forward price-to-earnings (P/E) ratio, aren't extreme-then dismisses that because they didn't signal trouble in 2007. Hence the focus on the oddballs, which were supposedly more prescient then and are higher still today. The measures in question are the cyclically adjusted P/E (CAPE), Q-ratio and the market value of all listed US equities as a percentage of all goods and services produced by US residents-or the ratio of US market cap to gross national product (GNP). In July 2001, Warren Buffett called this "the best single measure of where valuations stand at any given moment," so it is now known as the "Buffett Indicator."

No disrespect to any of the fine minds behind these indicators, but none tell you where stocks go. CAPE, created by John Campbell and Nobel Laureate Robert Shiller, compares stock prices to the last 10 years of inflation-adjusted earnings-the height of backward-looking. The intent is to even out market cycles' impacts on earnings, smoothing away the extreme highs and lows at peaks and troughs, but it actually adds skew. The 2007-2009 recession is still in CAPE's denominator. Does that have anything to do with how things go this year? Next year? 2017? There is little reason to think average earnings over the last decade predict anything, whether it's this year's earnings or the next decade's (CAPE is designed to "predict" 10-year returns). CFOs don't write business plans by slotting the last decade's earnings into the next 10 years. They try to assess the actual return on all their current and new investments, which generally have little to do with the last 10 years. They're at now now. Stocks look forward, too, not backward.

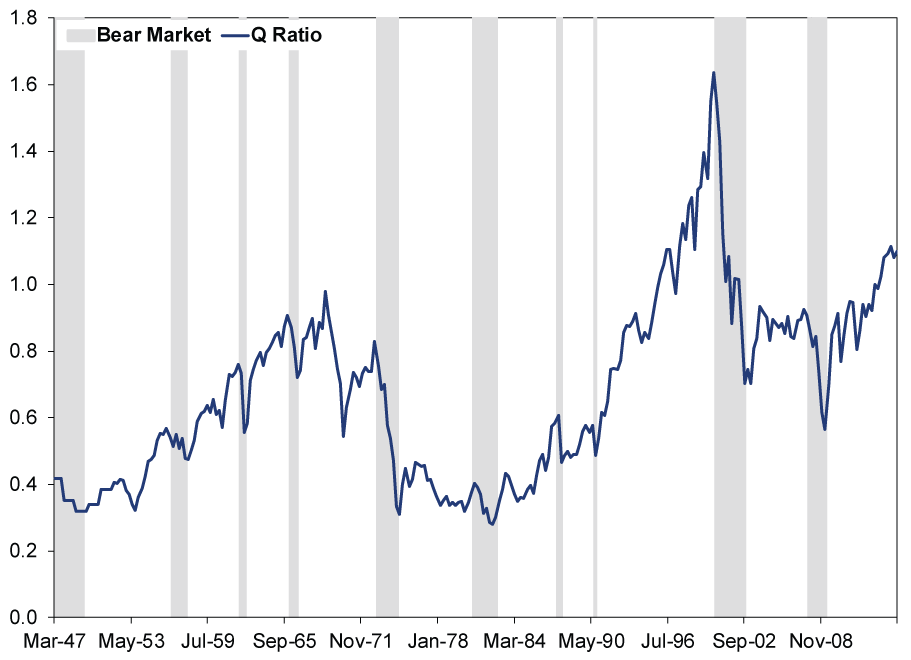

The Q-ratio, devised by another Nobel winner, James Tobin, divides market cap by the "replacement cost" of all included companies-the amount of money each would have to spend to replace all physical and intangible assets. There is a lot of accounting voodoo involved here, but most let the Fed do all the dirty work, using the conveniently replacement cost-adjusted measure of Corporate America's net worth from the quarterly "Financial Accounts of the United States." This appears to be what the Treasury folks did, ending up with a chart that looks like this:

Exhibit 1: Brought to You By the Letter Q

Source: FactSet and Federal Reserve, as of 3/30/2015. Net worth and market value of equities outstanding for all nonfinancial corporate businesses, 1947 - 2014.

There are a couple problems here. One, the data are ancient by the time they're released. The Fed releases this thing at a two-and-a-half-month delay. Q4 2014's update came out on March 12, 2015. Q1 won't come out till mid-June. All stale, not forward-looking. Two, as the chart makes readily apparent, there is no magic Q-ratio-trigger for bear markets. Bears have started when Q ratios were higher and lower than today's. Based on historical levels alone, Q could have signaled a bear market as early as 1993, when history's longest bull market turned three. Moreover, Q is based on the assumption stocks have some inherent fair value to which they eventually revert. That isn't true-stocks are always worth whatever the market is willing to pay for them, and the concept of fair value ignores long stretches of expanding valuations as bull markets mature and investors gain confidence. Mean reversion is a myth.

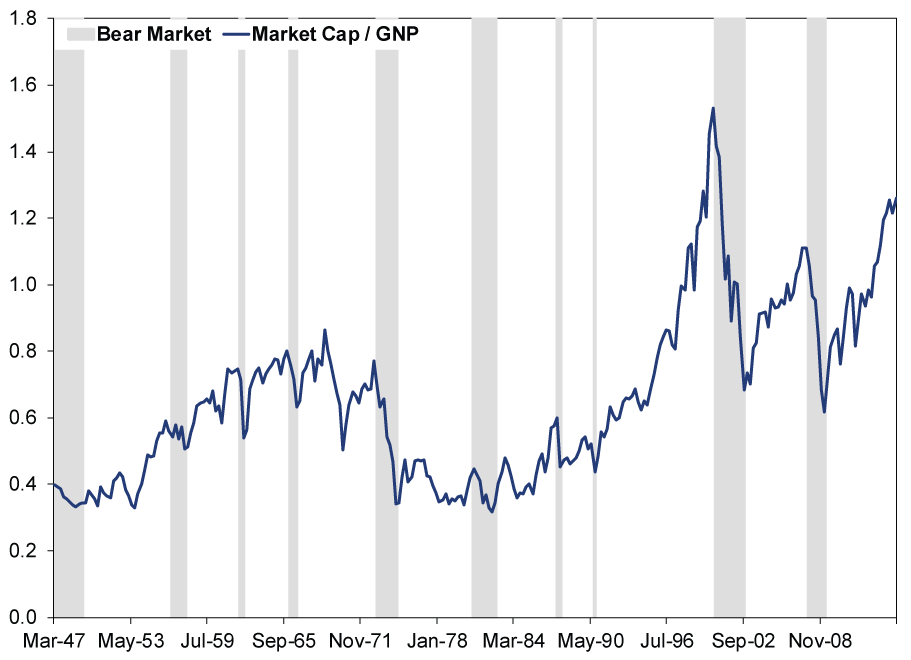

Finally, to the Buffett thingy. This thing has taken on a life of its own since Buffett mentioned it. The man himself says it's just a loose measure and useful only at the extreme-as he told Fortune last autumn, "It wasn't designed to be a fine-tuning type of valuation. It showed things had really changed in a big way [in the tech bubble]. A very high percentage of the time, stocks are in what I call a zone of reasonableness. ... There is a big zone of reasonableness. Anybody who thinks they can pinpoint it is crazy. It's not that precise." He went on to say stocks are currently in that zone of reasonableness, which sounds about right to us. But, that doesn't stop folks from trying to pinpoint. So here is a picture:

Exhibit 2: A Ratio Named After a Guy From Nebraska

Source: FactSet and Federal Reserve, as of 3/30/2015. US Gross National Product and market value of equities outstanding for all nonfinancial corporate businesses, 1947 - 2014.

Most, like the Treasury's report, interpret the latest upswing as a scary 2000-esque spike, which we have dubbed "The Omaha Omen." Whether they use GNP or GDP as the denominator[i], they assume this must be Very Bad News. Thing is, in addition to having all the above-mentioned standard valuation flaws (backward-looking, data stale by the time they're released, no repeatable bear market threshold), this indicator has construction issues. Stocks aren't a share of GDP or GNP. Stocks are ownership in the private sector's earnings, and market cap is a measure of wealth. GDP and GNP are rough calculations of the flow of economic activity in a given country.[ii] Those calculations include government spending and inventories and count imports as a negative-not an accurate measure of the private sector's health. Comparing stocks to GDP or GNP isn't even comparing apples to oranges, because at least both of those things are fruit.

Our advice: Flush all these valuations out of your brain and look forward, like stocks. Leading Economic Indexes are high and rising in much of the world, pointing to continued economic growth. Most Western nations are gridlocked and look set to stay that way looking ahead, minimizing legislative risk. Sentiment, as evidenced by the preponderance of bubble fears and popularity of these oddball valuations, isn't euphoric. Add it all up, and still-rising stocks look very reasonable indeed.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Buffett has used them interchangeably in his ratio, which is natural when you consider GNP was more widely used for much of the 20th century.

[ii] GNP and GDP are near-identical. GDP tries to capture the total goods and services produced in a country, while GNP tries to capture the total goods and services produced by a country's residents, including those living abroad. So GNP is GDP plus earnings on foreign investments minus foreigners' earnings on investments here. It too counts imports as negative and government spending as a positive.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today