Personal Wealth Management / Market Analysis

Weak UK GDP Isn’t Sneaking Up on Stocks

Recession chatter has swirled for months.

UK GDP fell -0.2% q/q in Q3—the first major nation to announce a contraction last quarter—and most commentary agrees this is just the start of a long-grueling recession.[i] After all, while September’s monthly GDP may have some artificial downward skew from the late Queen’s funeral bank holiday, cost-of-living pressures ramped up in October. Many presume Chancellor of the Exchequer Jeremy Hunt will dial up the pain with tax hikes and spending cuts at next week’s Autumn Statement, where he will present a raft of fiscal policy proposals. In our view, the UK economy is pretty clearly weakening, and obstacles lie ahead. Yet from an investing standpoint, we see more cause for optimism than gloom. UK recession chatter isn’t new, and its power over stocks seems to be waning. Moreover, with sentiment so low, the potential for positive surprise seems high—reality has a very low bar to clear.

There isn’t much to cheer in either the Q3 or September GDP releases, both of which hit Friday. September’s -0.6% m/m decline may have been milder without the extra bank holiday, which shut most retail and services, but the Office for National Statistics (ONS) warned this explains only half of the service sector’s -0.8% monthly contraction.[ii] The rest stems largely from cost-of-living pressures, which knocked consumer-facing services hard, extending August’s -1.6% m/m drop.[iii] Heavy industry eked out slight monthly growth, but that stemmed primarily from power and other utilities and mining, which includes oil production. Manufacturing, meanwhile, was flat overall, but that was because growth in pharmaceutical products and transport equipment offset declines in high-tech and commodity-heavy industries—more evidence of pressure from rising costs. Meanwhile, for Q3 overall, most positivity came from government spending and investment, while household spending and business investment declined. Net trade added a solid contribution, but imports’ -3.2% q/q drop played a big role in this.[iv] While this adds to GDP, it could represent weakening demand as the weak pound raised costs.

Mind you, we think it is a mistake to extrapolate any of the above forward. GDP reports tell you what just happened in the broad economy, not what will happen. They aren’t predictive, and some variability is normal. Moreover, the ONS initially reported a -0.1% q/q contraction in Q2 GDP before revising their estimate to 0.2% growth.[v] Q3 results could get a similar boost as more data come in. They could also be revised downward, but we are highlighting possibilities here, not assigning probabilities. Fiscal policy is a wildcard for now, but even the rumored “austerity” isn’t necessarily a huge negative. The last time the UK launched an austerity program, total public spending grew by less than originally planned but didn’t contract outright, and much of the effort focused on transfer payments, which aren’t part of the government components of GDP. More tax hikes could squeeze households, but the aspects of former Prime Minister Liz Truss’s mini-budget that have so far survived—including the reversal of a small national insurance tax hike and some assistance for household energy costs—could be a partial offset. This is all very much wait-and-see.

But for stocks, a lot of this is probably just too far in the weeds. Markets don’t sit around trying to calculate the impact of every fiscal policy tweak. Rather, notwithstanding short-term volatility, they assess a simple question: What does the likely path of corporate earnings look like over the next 3 – 30 months compared to what everyone expects? It is the gap between these two—reality and expectations—that determines stock prices in the mid-to-longer term. So for stocks, the crucial question isn’t whether the UK has entered recession or not, but whether a weakening economy is a big shock.

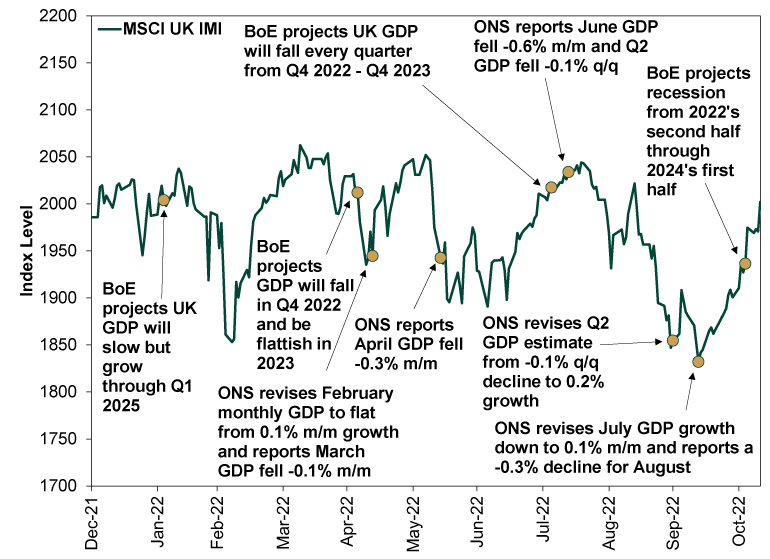

We don’t think it is. Exhibit 1 overlays the MSCI UK Investable Market Index (IMI) in pounds (to avoid skew from the strong dollar) and this year’s major economic news and forecasts. As you will see, markets have been dealing with worsening data and forecasts all year. The Bank of England (BoE) has projected a late-year recession since early August. Yet UK stocks are up markedly from October 12’s low and closed Thursday slightly positive year to date, making Britain one of the best-performing countries in the developed world. Even in dollars, the UK is the fourth-best performing country in the MSCI World Index this year, despite having had one of the worst economic outlooks for months. Overall, it sure seems to us like UK stocks are dealing with a lot of the recession talk in advance and moving on.

Exhibit 1: UK Stocks Have Dealt With Recession Chatter for Months

Source: FactSet, Bank of England and Office for National Statistics, as of 11/11/2022. MSCI UK IMI return in GBP with net dividends, 12/31/2021 – 11/10/2022.

This, by the way, isn’t unusual. When a stock market downturn accompanies a recession, stocks usually move first. They are typically down considerably by the time the recession becomes apparent. Sometimes they begin recovering before the recession even becomes official. Other times, the downturn lasts a bit longer, then rebounds before the economy does. When the eurozone endured its 2011 – 2013 debt crisis and recession, eurozone stocks retested their low in euros for the last time in June 2012, but GDP continued falling through Q1 2013, nearly nine months into a new regional bull market.

It is all impossible to time with precision—and all turning points are clear only in hindsight—but stocks don’t wait for the economy. Therefore, we think it would be mistaken to see negative GDP as a reason to turn bearish on UK stocks now.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today