Personal Wealth Management / Economics

What China’s April Data May Show Global Investors

While the specifics will vary from nation to nation, China’s April data help set expectations for what awaits reopening economies.

China released several widely watched economic reports last Friday, providing more insight about the country’s performance since lifting its most severe COVID-containment policies in early March. Some doubt China’s numbers will shed much light about post-COVID life elsewhere—mostly citing unique features of the country’s lockdown and rebound. There is some sense in that. China’s experience won’t look exactly like Continental Europe’s, which won’t look perfectly like America’s (etc., etc. and so forth). Still, in our view, China’s nascent economic recovery offers an instructive preview of life following a virus-driven shutdown—and should help set investors’ expectations.

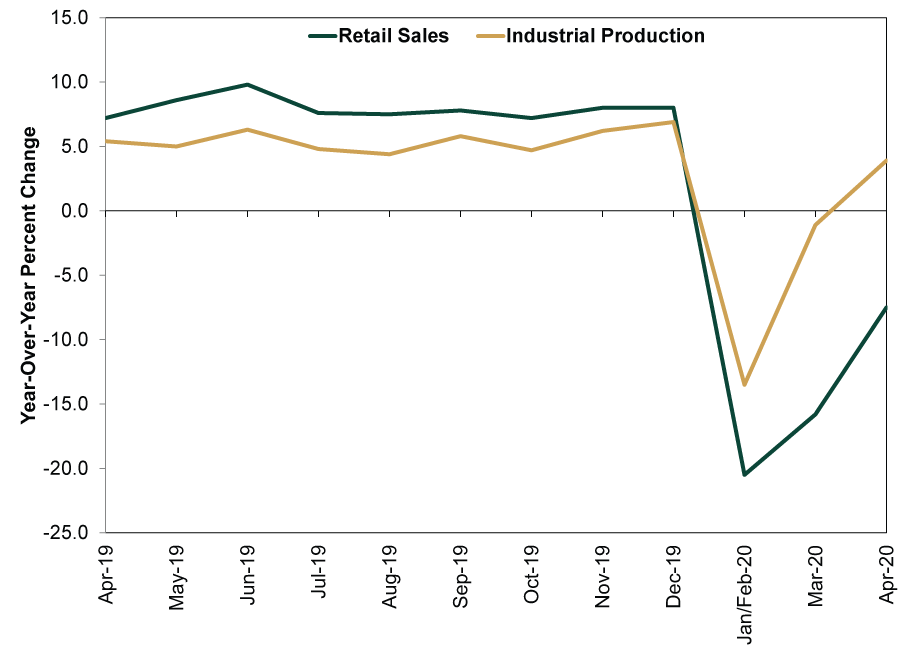

In China’s first full month without national COVID restrictions, April industrial production rose 3.9% y/y, returning to positive territory after March’s -1.1% slip and January – February -13.5% decline (China typically consolidates January and February economic data to account for the monthly skew from the shifting Lunar New Year holiday). Retail sales fell -7.5% y/y—the second straight month showing slower declines. Both these measures have improved markedly from the start of the year, when authorities extended the Lunar New Year holiday as part of China’s COVID-19 containment effort.

Exhibit 1: China Retail Sales and Industrial Production, April 2019 – April 2020

Source: National Bureau of Statistics of China, as of 5/18/2020.

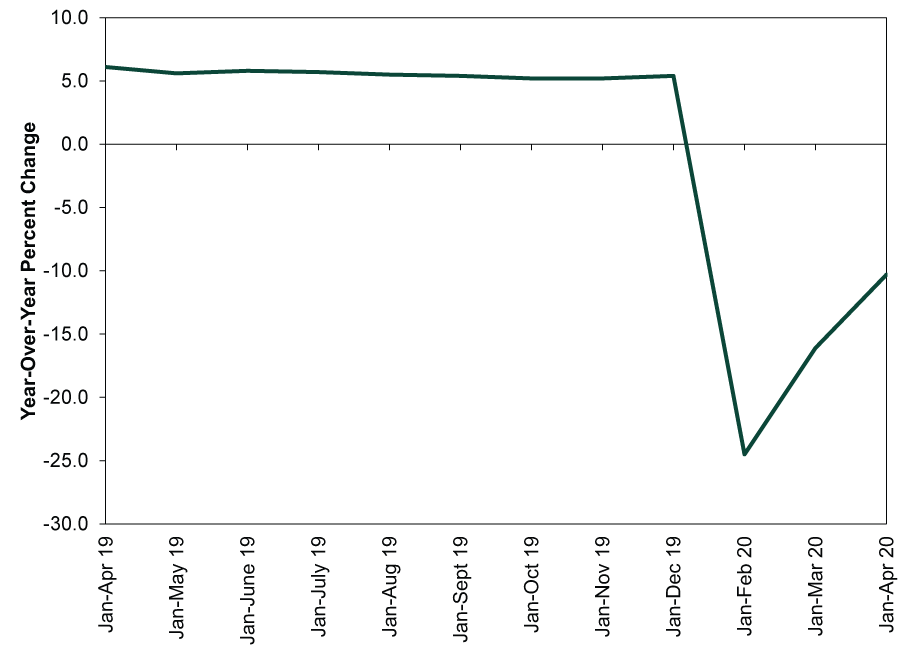

Another widely watched measure—fixed asset investment (FAI), a gauge for construction and development—fell -10.3% year to date (YTD) through April compared to the same period in 2019. (Here, too, most analysts look to measures comparing this cumulative year-to-date change versus last year to account for the lack of seasonal adjustment.) This is also a slower pace of decline than FAI’s -16.1% drop in the January – March period versus 2019’s first three months, suggesting domestic economic activity is coming back online post-lockdown.

Exhibit 2: China Fixed Asset Investment, April 2019 – April 2020

Source: National Bureau of Statistics of China, as of 5/18/2020.

While acknowledging the improvement, many observers doubt its sustainability. Some noted the recent rebound is concentrated in heavy industry. Investment in power, gas and water-supply infrastructure grew its fastest since 2016, which coincides with China’s last big stimulus push.[i] Hence, they conclude April’s uptick is all about targeted stimulus efforts, as spending on local infrastructure projects is a common way for the government to support growth. Similarly, others worry about the disconnect between production and demand as factories churn out goods for domestic and overseas customers who aren’t yet spending.[ii] The upshot: Many see April’s relative improvement as a short-term mirage, detached from a weaker longer-term reality.

In our view, extrapolating one month of data, positive or negative, as the new normal seems a bit myopic. We aren’t saying April economic data are robust or signal an inflection point, and these measures may even weaken in the near term. With other major economies either still locked down or early in their reopening plans, flagging foreign demand will likely be a short-term headwind for Chinese growth—April purchasing managers’ indexes show falling export orders.[iii] However, the reaction to April data is telling about sentiment, in our view. The rampant doubts, questions and skepticism seem like examples of the “pessimism of disbelief,” in which people are hyper-focused on the dreary present, dismissing signs of improvement as phony or fleeting.

Rather than get bogged down in details or project longer-term implications, we think April data best highlight a basic, high-level development: China is in the midst of a nascent recovery following a sudden, institutionally induced economic coma. Doubts about the sustainability are understandable. From here, recoveries in China and elsewhere depend largely on economies reopening and staying reopened. Myriad unknowable factors could impede that progress. China’s recovery also isn’t a perfect blueprint for developed world economies since flagging external demand will likely weigh quite heavily on Chinese output. Yet as other major economies gradually return to business, demand likely recovers, too. Hence, to the extent China’s bounce is early, it may also simply be a precursor of the broader emergence yet to come when the world returns to work more fully.

Despite their differences, both China and other major economies face similar expectations: Few believe a recovery will be quick. Many think an extended “W”-shaped recovery is China’s best-case outcome. That echoes forecasts for the US and Europe, where typical projections anticipate long, halting recoveries dependent on government spending. We aren’t saying every country will recover in the same exact manner and timeframe. But that so many broadly apply a uniformly dour outlook about the global economy’s prospects indicates how pessimistic sentiment has become. That dour outlook—and the quick willingness to discount any hopeful sign—helps depress expectations and form the next bull market’s foundation, whether that is already underway or still to come.

[i] “China Is Powering Up Again. That Might Not Be a Good Thing,” Nathaniel Taplin, The Wall Street Journal, May 15, 2020.

[ii] “Coronavirus Seemingly Tamed, Chinese Economy Starts to Recover,” Keith Bradsher, The New York Times, May 15, 2020.

[iii] Source: IHS Markit, as of 5/19/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today