Personal Wealth Management / Market Analysis

What the Fed’s Big Rate Cut Does and Doesn’t Do

Today’s move might not have been necessary, but it could bring a minor benefit.

The Fed made its first “emergency” rate cut since 2008’s financial crisis this morning, slashing 50 basis points off the fed-funds target range to bring it to 1.0% – 1.25%. In his accompanying press conference, Fed head Jay Powell deemed the coronavirus a “new risk” to the economic outlook and said the central bank decided to ease monetary policy in response. He also left the door open for another move at the Fed’s next meeting in two weeks. The public reaction seemed divided. Some cheered the move as a positive step in bolstering the economy. Others saw it as a fearful sign superhuman rate-setters saw big trouble ahead. Finally, some bemoaned the fact the Fed didn’t do or promise more. We won’t wade into that debate, as there is little the Fed can do to combat coronavirus-related headwinds. However, Tuesday’s move does address one key factor getting less attention—America’s inverted yield curve—which may be a minor benefit.

On the bright side, the Fed’s move does shore up confidence that the bank is ready and willing to act when things get tough. It shows decisiveness and perhaps boosts credibility—both fine things, in general. However, an interest rate cut doesn’t directly address the potential damage from the coronavirus.

Usually, rate cuts aim to stimulate demand. But the coronavirus isn’t a headwind against demand alone—rather, it hits supply harder. A Fed rate cut cannot end quarantines in China, Korea, Japan and Europe. It cannot get folks back to work. It cannot replace the auto parts and consumer goods that aren’t flowing from China at the moment. It cannot stand in for sick workers. We guess it could help tourism-reliant businesses get over the hump if they were to encounter a short-term cash crunch, but industry estimates peg travel and tourism at around 8% of GDP annually.[i] A short-term, localized hit to an industry that small isn’t going to move the needle much. To the extent it helps smaller businesses stay afloat and keep workers, great. But that is probably a local, micro benefit, not a macroeconomic boost.

The real benefit of this move, in our view, is that it addresses the inverted yield curve. As we wrote last week, we didn’t think this small inversion was likely to derail the expansion. A slightly deeper inversion that persisted for several months last year didn’t hit banks’ profits or lending much. But cutting rates now at least gives the impression that the Fed isn’t asleep at the wheel. We don’t think it is a coincidence that the Fed chose a 50-basis-point cut the day after the 10-year US Treasury yield closed at 1.08% and the effective fed-funds rate closed at 1.59%.[ii] A 50-basis-point cut would effectively erase that, depending on how long-term bond markets respond—something we won’t know until Wednesday’s close.

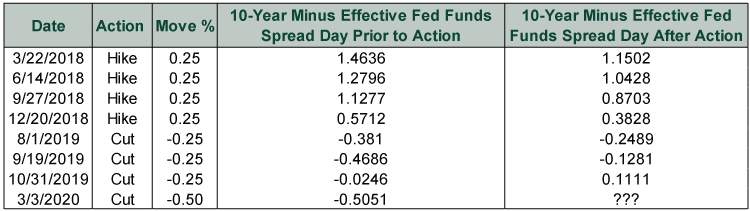

To us, this seems consistent with how the Fed has managed monetary policy in recent years. They appear to be aiming for neutral, rather than stimulus or tightening. Powell and other FOMC members have basically said as much on a number of occasions. Unlike his immediate predecessors, he also seems to be paying particular attention to the yield curve. October 2018’s Senior Loan Officer Opinion Survey included special questions asking loan officers to consider how a prolonged flat or slightly inverted yield curve would affect credit conditions. Would they be more or less likely to lend to borrowers at various credit scores? The answer: “Significant shares of banks indicated that they would tighten their standards or price terms across every major loan category if the yield curve were to invert.” It is likely no accident that the last Fed rate hike occurred weeks later, when the yield curve was still modestly positive. Nor does it seem insignificant that 2019’s cuts seemingly aimed to gradually undo the modest inversion, as Exhibit 1 shows.

Exhibit 1: Fed Rate Moves and the Yield Curve

Source: FactSet, as of 3/3/2020. 10-year US Treasury yield, constant maturity, and effective fed-funds rate, as of market close on the days before and after the date referenced. FactSet reflects interest rate moves the date they are effective, not the day of the announcement.

We guess one could quibble over whether it is logical for the Fed to cut rates in reaction to short-term volatility in Treasury markets, but that seems rather academic at this point. We are quite sure the Fed is well aware that a panicky flight to safety deserves at least some credit for 10-year Treasury yields’ journey toward, and potentially south of, 1.0%. But what better way to shore up confidence than to respond with an effective “deep inversion? Heck no, not on my watch!” To the extent that helps assuage sentiment and long rates, steepening the yield curve, so much the better.

So no, today’s move probably wasn’t necessary when you assess the facts objectively. But necessity doesn’t matter as much as whether a move is a net benefit, negative or neutral. In this case, we think it is likely neutral to a minor benefit.

[i] Source: FactSet and National Travel and Tourism Office, as of 3/3/2020. Based on 2017 nominal GDP and travel and tourism output.

[ii] Source: FactSet, as of 3/3/2020. 10-year US Treasury yield, constant maturity, and effective fed-funds rate on 3/2/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today