Personal Wealth Management / Economics

What the Pop in PMIs Says About Sentiment Today

Look beyond PMIs’ record highs for signs of where the bull market is today.

Some widely watched business surveys hit record highs in April, generating plenty of headlines. However, we think the more interesting takeaway was the overall optimistic reaction to the readings—rational, though a sign the bull market is a step closer to euphoria. That makes tracking sentiment’s evolution critical going forward—and one way investors can do that is through monitoring what pundits and analysts say (and don’t say) about economic data.

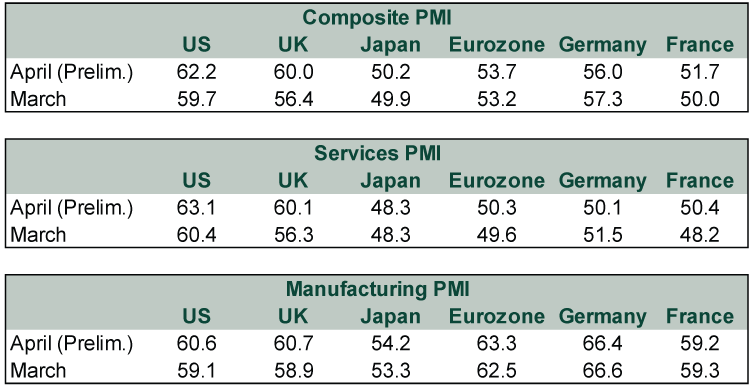

Purchasing managers’ indexes (PMIs) are monthly surveys measuring the percentage of businesses reporting increased activity, with readings above 50 implying expansion. Preliminary (or “flash”) readings represent about 80% - 90% of total responses and are the timeliest economic reading out there. IHS Markit’s April flash PMIs for several major developed economies broadly improved on March. (Exhibit 1)

Exhibit 1: Developed Economies’ Recent PMIs

Source: FactSet and IHS Markit, as of 4/27/2021. Composite PMI combines services and manufacturing output.

While PMIs don’t register the magnitude of growth, they provide a handy, timely snapshot of business conditions. One development headlines rationally noted: April’s PMIs reflect the return of business activity as COVID restrictions relaxed—particularly in people-facing services industries, which lockdowns hit hard. Thanks in part to their faster vaccine rollouts, the US and UK are leading the eurozone and Japan. But reopening-related pops aren’t surprising: We saw them last year as developed world economies eased their first COVID lockdown measures.

But not all interpretations were so rational. Some pundits said April’s PMIs signaled lasting, strong growth ahead. One typical rationale: Thanks to an excess of savings, consumer spending in developed economies will surge, powering a long economic boom. As one economist argued, “Households are ready and eager to spend as soon as we ease the remaining restrictions. We’re going to go on a big spending spree in the U.K.”[i] This argument features heavily in America, too. While we do expect some pop as economies continue reopening, we aren’t convinced it will persist further into the future in a new “roaring twenties”—or that it will be as big as many seem to think. As some recent US data suggest, there is no rule saying consumers must spend down all their savings.

On the flipside, some worry PMI readings show the seeds of inflation germinating. With global supply chains already strained, they fret shortages will drive prices higher, weighing on growth. We agree supply shortages can contribute to higher prices of certain goods, though this won’t necessarily spill across the entire economy. These disruptions are usually temporary, as rising prices tell producers to find ways to increase production. Strong consumer demand outpacing supply is a problem for prices only if there are material barriers to increasing supply, and there isn’t much evidence that is the case now.

That both these arguments are part of the general discourse indicates sentiment is heating up but not irrationally sunny yet—a few false fears linger. When investors are broadly optimistic—which seems to be the case today—rational cheer about the present and future is the prevalent mood. Investors treat good news as good and don’t overstate bad news. Maybe headlines extrapolate the odd negative development in an irrationally negative manner, but that doesn’t dominate. The effort to find a cloud in a silver lining doesn’t overshadow everything—rather, the silver shines (even as a cloud gets a few sentences). Most PMI coverage we have seen strikes this tone. While projections of a savings-driven boom are misplaced, we agree developed economies’ reopenings and a return to normal will drive growth this year.

Moreover, skeptics aren’t ignored when sentiment is optimistic, and pockets of worries still get attention—as they do now. Beside concerns over rising prices, some fear ongoing COVID issues will weigh on the global economic recovery—see forecasts for lagging eurozone growth and the struggles of major Emerging Markets such as India. That suggests euphoria hasn’t taken hold yet. When euphoria is widespread, rationality goes out the door, and investors and pundits alike find ways to justify their optimism about future economic conditions. They overlook or discard all negatives. If investors were euphoric, inflation concerns wouldn’t have such staying power.

Tracking sentiment’s evolution is crucial for investors, in our view, since stocks are behaving more like it is a late-cycle bull market than early-cycle. We think this distinction has investing implications, as it favors growth stocks over value going ahead. Today’s widespread optimism would be unusual early in a bull market. Pessimism and skepticism usually dominate in a bull market’s early stages, as the memory of the past bear market lingers and weighs on sentiment. This is typically when value stocks do best—after they take their drubbing in the downturn and only the steeliest investors have the guts to own them. That isn’t the case now. Value stocks have received lots of love over the past several months, especially after their recent outperformance—a short-term countertrend, in our view. We think growth stocks will regain the leadership baton as developed economies return to their slower, less exciting pre-COVID trends—a scenario many value proponents seem to overlook.

[i] “U.K. Economic Activity Surges at Fastest Pace in Seven Years,” Lucy Meakin and David Goodman, Bloomberg, 4/23/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, US Q2 GDP, Eurozone Inflation

2026-07-27

2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today