Personal Wealth Management /

What to Make of the March Jobs Report

With weaker labor data likely to come, remember jobs numbers lag both economic growth and stocks.

The US Bureau of Labor Statistics announced March jobs numbers today, and as expected, they were bad. Yet after two weeks in which about 10 million Americans filed for unemployment assistance, many were likely also shocked nonfarm payrolls fell by just 701,000 jobs in March, pushing the unemployment rate up to 4.4%. There are some technical reasons for this, and those reasons are why many pundits expect the worst data are yet to come—and that general sentiment is almost certainly correct. In our view, though, the March jobs figures also highlight how late-lagging unemployment data are and why they shouldn’t guide your views about forward-looking stocks—especially now.

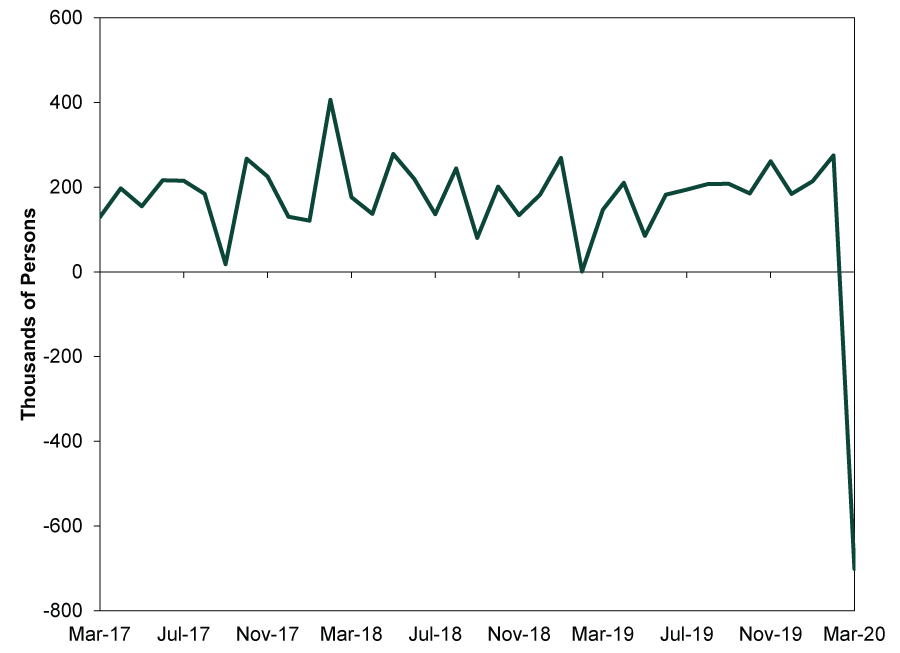

Wherever you want to start, the numbers were bad. Payrolls’ 701,000 drop was the biggest monthly decline since March 2009, ending the US’s record-long streak of 113 straight months of job growth.

Exhibit 1: Total Nonfarm Employees, Month-Over-Month Change

Source: St. Louis Federal Reserve, as of 4/3/2020. Month-over-month change in total nonfarm employees, March 2017 – March 2020.

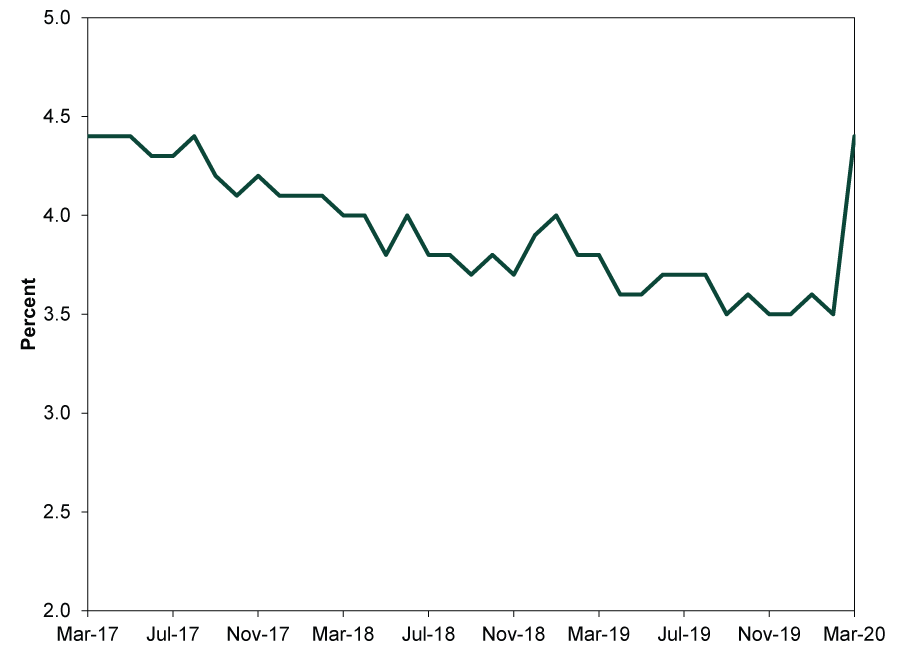

The unemployment rate jumped from its generational low of 3.5% in February to 4.4% in March—the biggest one-month increase since January 1975.

Exhibit 2: Unemployment Rate

Source: St. Louis Federal Reserve Bank, as of 4/3/2020. Unemployment rate, monthly, March 2017 – March 2020.

Industry-wise, leisure and hospitality led the downturn with 459,000 job losses, with restaurants and bars (417,000) comprising the vast majority. This isn’t surprising considering these were among the first to close as social distancing escalated. However, just about every industry suffered losses, from health care (e.g., dentist, physician and other health care practitioner offices) to professional services (e.g., travel arrangement and reservation services employees). As bad as the numbers look, they don’t reflect the human costs. Lost jobs inflict personal hardships on all those impacted and their families. For many, it can be a personal tragedy.

Experts expect worse to come, and they are likely right. This report’s reference period ended March 12—before many states enacted more restrictive shelter-in-place orders. As the latest jobless claims reports show, about 10 million people filed in the last two weeks of March. With layoffs ongoing as well as logistical delays due to swamped processing systems, jobless claims are likely to continue rising—and will show up in April’s jobs report. Based on some economists’ models, the unemployment rate will soar next month. For example, economist Justin Wolfers, writing for The New York Times, estimates that with 16 million more people likely without work, April’s unemployment rate will be 13%—about three times March’s rate and above the peak 10% rate stemming from the financial crisis a decade ago.[i] He isn’t alone in penciling in huge jumps.

As investors digest these daunting figures, it is critical to decipher what they do—and, notably, don’t—tell us. The jobs report details the extent of the damage to the labor market, but it doesn’t reveal anything that isn’t widely known already. We know April’s jobs report will likely be bad since the last two weeks’ initial jobless claims gave us a preview. So did the flash purchasing managers’ indexes (PMIs) out a week and a half ago and today’s final PMIs, which not only signaled the economic conditions that brought these job losses, but also included employment subindexes. Stocks, as always, began signaling a deep economic contraction before all of these figures arrived.

Some pundits warn unemployment will remain elevated for the foreseeable future, bringing severe economic consequences. Some argue the labor market will take years to recover from the COVID-19 shock—and that the surviving businesses will have to become much more conservative. This takeaway strikes us as a bit hasty given the range of possible outcomes. For example, should developments improve—e.g., if the virus’s outbreak slows and governments relax their COVID-19-related restrictions earlier than many think—the sharp economic downturn may be fleeting, followed by a swift recovery. The situation is too fluid to definitively say either way.

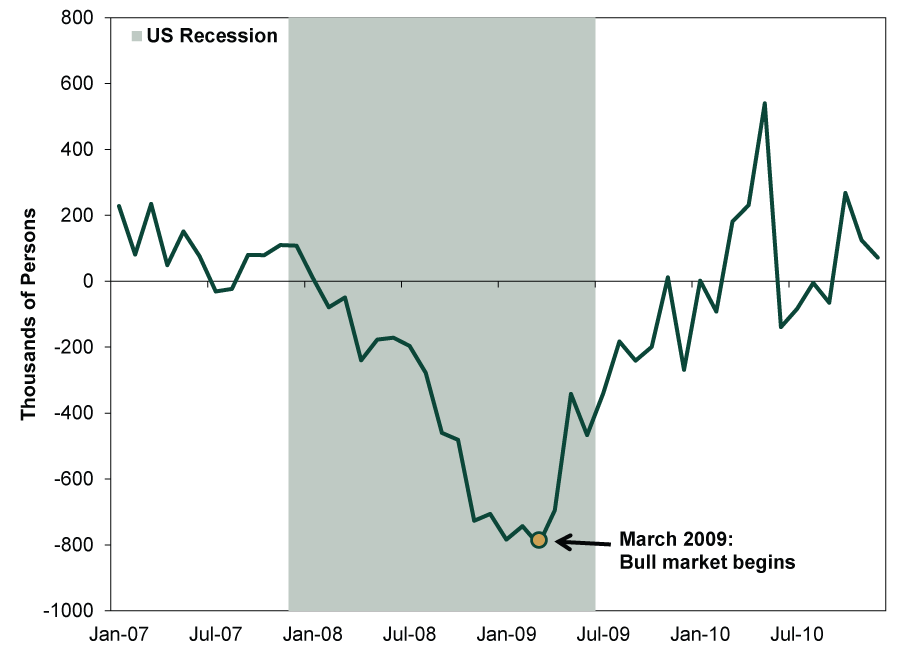

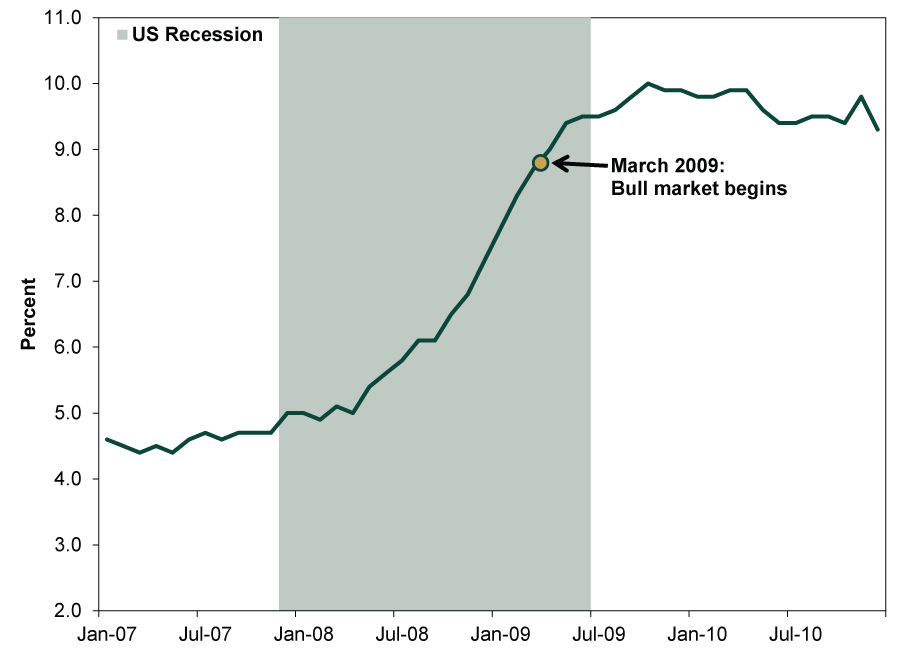

From an investing perspective, though, the most important takeaway is that whenever jobs data begin improving, stocks will probably have already begun recovering. Jobs are a lagging economic indicator. They reflect decisions businesses made in the past. Economic growth and contraction drive hiring or firing decisions—not the other way around. The past recession and bear market illustrate how stocks lead economic growth—and growth leads jobs.

Exhibit 3: Total Nonfarm Employees, Month-Over-Month Change

Source: St. Louis Federal Reserve Bank, as of 4/3/2020. Month-over-month change in total nonfarm employees, January 2007 – December 2010.

Exhibit 4: Unemployment Rate

Source: St. Louis Federal Reserve Bank, as of 4/3/2020. Unemployment rate, monthly, January 2007 – December 2010.

As more data detail COVID-19-related economic damage, we think it is important for investors to think like stocks and look ahead. Jobs numbers won’t tell you anything about where markets are headed next.

[i] Source: Federal Reserve Bank of St. Louis, as of 4/2/2020. Unemployment rate was 10.0% in October 2009.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today