Personal Wealth Management / Financial Planning

Why Bonds Still Make Sense in a Low-Yield World

Fixed income can still do its job.

No matter where you look or how you cut it, bond yields are historically low. That has many asking: Why hold them at all? In our view, bonds’ primary purpose is to dampen portfolio volatility to mitigate swings for those needing to draw cash flow. Yes, yields today are miniscule, but we think bonds’ ability to cushion against short-term volatility endures—and makes a compelling case for them, should your goals and needs make smaller swings optimal.

On August 4, 10-year Treasury rates dropped to a record-low 0.5%, and they have hovered below 1% since.[i] Meanwhile, investment-grade corporate bond yields have fallen below 2% for the first time.[ii] Both are well below their averages during the 2009 – 2020 economic expansion (2.4% for 10-year US Treasurys, 3.5% for corporates), when people were also complaining about yields being too low.[iii] Yet even then, investors could assume a bit more credit risk, buy corporate bonds with still-low default probabilities and earn positive inflation-adjusted returns. Not hugely so, of course, but still positive. Now, this refuge is dwindling.

Contrary to what many yield-focused investors may think, record-low rates don’t mean bonds play no role in portfolios today for those who need cash flow. They tend to fluctuate less than stocks in the short term—a vitally important point for these investors to weigh. If your long-term financial goals require a relatively high rate of cash flow, a blend of stocks and bonds can be very beneficial. Yes, portfolio income—bond interest or dividends—can help fund withdrawals. But as we have written, selling slices of securities is often a better, more reliable means. With this in mind, the combination of price movement and income—total return—is what matters most.

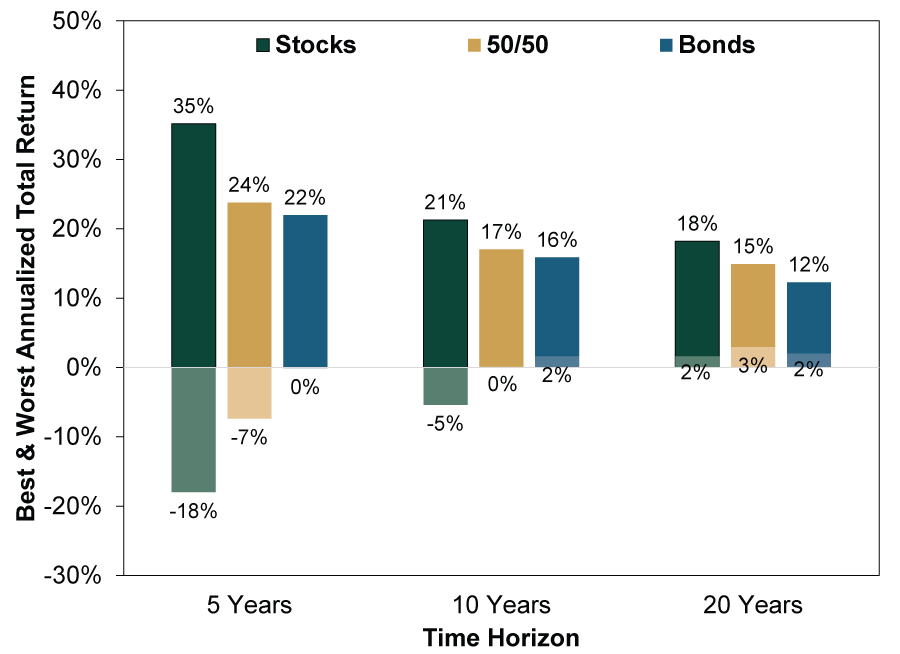

Because stocks’ short-term returns can vary greatly, regular withdrawals at relatively high rates from an all-stock portfolio could risk unwanted portfolio depletion if you hit a stretch of subpar returns or down years. Including bonds—regardless of their yield—helps mitigate this risk. Corporate bond returns’ standard deviation—measuring their degree of fluctuation—over rolling five-year periods since 1925 shows this stabilizing effect. 20-year investment-grade corporate bonds’ standard deviation is 3.8%, which means over any five-year timeframe, including the most extreme within the last century, their annualized total return was usually within plus or minus 3.8 percentage points of their 6.1% average.[iv] Moreover, there has never been a five-year stretch where their returns were negative. (Exhibit 1)

Exhibit 1: Bonds Can Dampen Volatility in the Short Term

Source: Global Financial Data, Inc., as of 12/11/2020. S&P 500 Index and 20-Year US AAA Corporate Bond Index annualized total returns, rolling 5-, 10- and 20-year periods, December 1925 – November 2020.

In contrast, stocks’ standard deviation over rolling five-year periods is more than twice bonds’: 8.6%.[v] Stocks’ average annualized total return is higher—10.0%—but the greater variability around that means five-year time periods have been negative 12% of the time.[vi] (Notably, most of those occurred during the Great Depression and WWII. Post-war, their frequency of negativity has been about half that.) So while bonds can fall a bit, it has happened less often, and by smaller magnitudes, than stocks. Hence, a fixed income allocation’s principal role is to smooth out returns, raising the likelihood your portfolio can provide cash flow throughout your time horizon even under historically bad circumstances.

Naysayers argue now is different, presuming record-low rates are an anomaly that must reverse quickly as the economy moves on from the pandemic. Since bond yields move inversely to prices, rising rates mean falling bond prices. This is true to an extent, but we think careful management of your bond positioning can mitigate this risk, which is where managing for total return comes in handy. Bonds come in different maturities. Although rates are low across the board, shorter maturity bonds still aren’t as susceptible to rising rates. If you expect rates to rise (and your reasoning isn’t widely shared), you can mitigate the impact on your total return by reducing your bond portfolio’s duration. Also, shorter-term corporate bonds yield a bit more than similar-maturity Treasurys, providing some insulation from rising rates. Corporate bonds also have other drivers beyond government interest rates. If the economy heals and that drives Treasury rates up, rising profitability may mean corporate rates rise by a smaller amount.

Note, we aren’t saying the time to brace for trouble is now. In our view, it isn’t clear big rate increases are around the corner. Interest rates are sensitive to inflation expectations, so it is worth considering what might cause inflation to surge. The consumer price index appears set to rise somewhat in early 2021 from November’s 1.2% y/y.[vii] But this is tied mostly to base effects from plunging prices in March and April 2020, which skew the denominator in the year-over-year calculation. Markets are generally good at seeing through such calculation quirks. Beyond that, whether price acceleration lasts is an open question. As the economy recovers and commerce speeds up, some further rise wouldn’t be shocking.

The question for bond positioning is the degree. Thus far, there is no sign the Fed and other central banks are letting up on their quantitative easing bond purchases. Around the world, they have been hoovering up long bonds, keeping their yields low, which flattens yield curves—a disinflationary force, in our view. Then too, even if materially higher inflation is coming, it is unlikely to be overnight—enough time to adjust how your fixed-income allocation is invested.

Overall, bond returns may not be great, but they can still mitigate volatility, which can be critical for meeting your anticipated funding needs.

[i] Source: Federal Reserve Bank of St. Louis, as of 12/11/2020. 10-year Treasury yield, 8/4/2020.

[ii] “Demand for Corporate Bonds Drives Inflation-Adjusted Yields to Zero,” Sam Goldfarb, The Wall Street Journal, 12/7/2020.

[iii] Source: Federal Reserve Bank of St. Louis, as of 12/11/2020. 10-year Treasury and ICE BofA US Corporate Index yield averages, June 2009 – February 2020.

[iv] Source: Global Financial Data, Inc., as of 12/11/2020. 20-Year US AAA Corporate Bond Index annualized total returns, rolling 5-year periods, December 1925 – November 2020.

[v] Ibid. S&P 500 Index annualized total returns, rolling 5-year periods, December 1925 – November 2020.

[vi] Ibid.

[vii] Source: Federal Reserve Bank of St. Louis, as of 12/11/2020. CPI, November 2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today