Personal Wealth Management /

Why This Bull Market Has Room to Run

Widening yield spreads are a good predictor this bull market likely has plenty more gas in the tank.

With investors expecting the Fed to end quantitative easing soon, the yield spread is widening—fuel for stocks! Photo by Alex Wong/Getty Images.

Since 1932, the average S&P 500 bull market has lasted roughly four and a half years. With the present bull market a hair older than the average—and with domestic and global indexes setting new highs—some fret this bull market is long in the tooth. However, while bull markets die of many things, age and gravity aren’t among them. History argues the fundamentals underpinning this bull market are powerful enough to lift stocks higher from here, with economic growth likely to continue—and potentially even accelerate moving forward as bank lending increases.

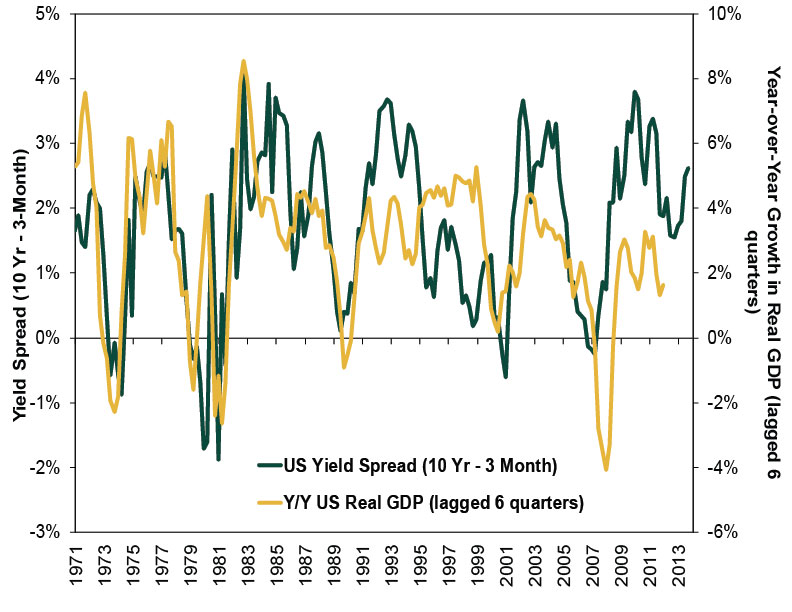

No single indicator is a perfect predictor of the future, but some are better than others. Among the best predictors of future economic growth is the spread between short- and long-term interest rates—the yield spread. As Exhibit 1 shows, the US yield spread has typically forecast real US economic growth by roughly 18 months. Recently, growing expectations the Fed will begin reducing its quantitative easing long-term bond buying have contributed to widening yield spreads—implying strengthening economic growth ahead.

Exhibit 1: Yield Spreads Typically Lead Real GDP Growth

Source: Thomson Reuters and Global Financial Data, as of 9/30/2013.

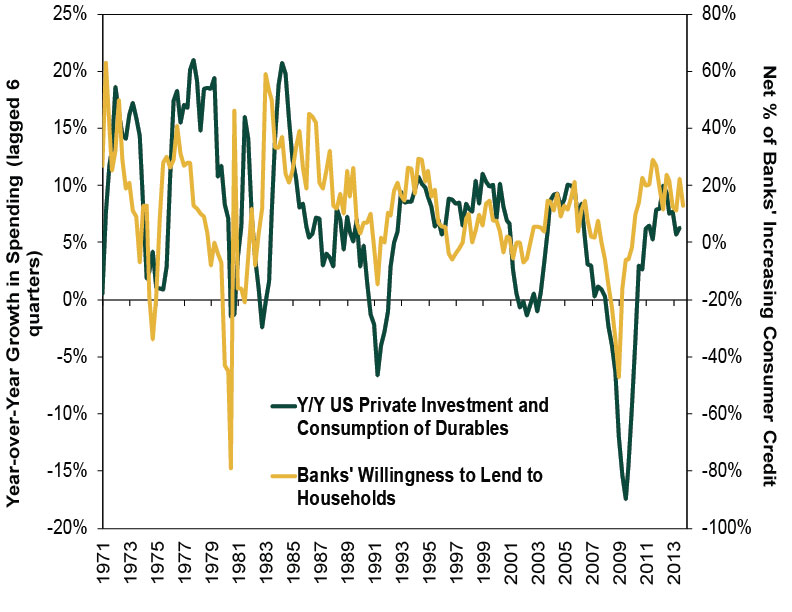

The reason wider yield spreads typically lead to stronger economic growth is related to banks’ incentives. Banks typically borrow at short-term rates (e.g., bank deposit rates) and lend at long-term rates (e.g., mortgage rates). Therefore, the yield spread is roughly a bank’s profit margin on loans. Banks—like humans in general—respond to incentives, so profit margins heavily influence a bank’s willingness to lend (Exhibit 2).

Of course, capital availability can also factor into banks’ ability to lend. A primary reason the Fed was established in 1913 was to act as a last resort lender should banks temporarily lack the capital to lend. Arguably, banks lacked capital to lend in the 2008 financial crisis and required assistance. However, following major recapitalizations and round after round of quantitative easing, banks now have plenty of capital to function. Therefore a widening interest spread should increase the profitability and, as a consequence, availability of loans moving forward.

Exhibit 2: Yield Spreads Typically Lead Banks’ Willingness to Lend

Source: Thomson Reuters and Global Financial Data, as of 9/30/2013.

As credit availability rises, it tends to drive higher private investment and durable goods consumption—typically, credit-dependent items (Exhibit 3). Fundamentally, bank lending also increases the quantity (via the multiplier effect) and velocity of money (frequency it changes hands), greasing the economic engine. Economists have long known rising money supply and velocity typically result in higher nominal GDP growth. (Money Supply * Velocity = Price * Quantity = Nominal GDP.) This is the quantity theory of money—more than 100-years-old.

Exhibit 3: Private Investment and Durable Consumption Tracks Banks’ Willingness to Lend

Source: Thomson Reuters, as of 9/30/2013.

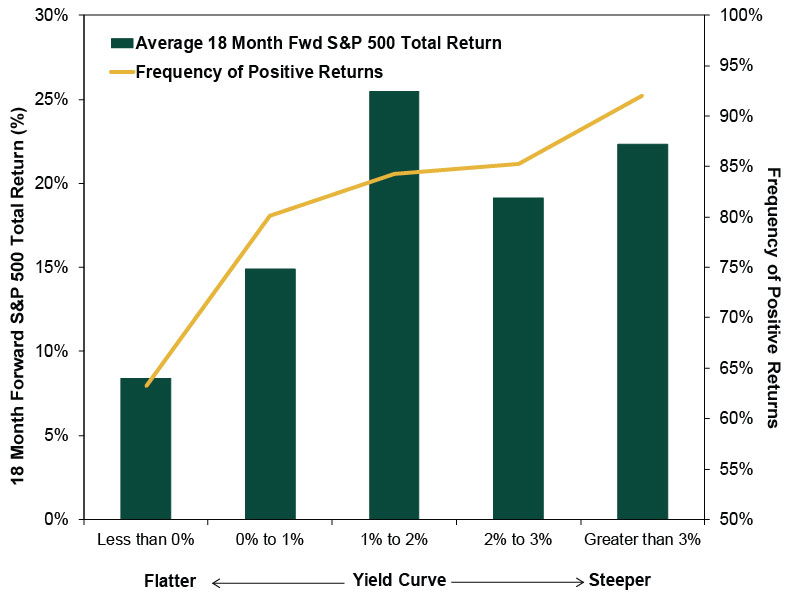

Of course, economies and equity markets are not the same thing. Stock prices are determined by the supply and demand of equities. They are also typically forward looking, moving ahead of fundamental events. However, tied to its influence on corporate profits, future economic growth is one of the larger determinants of equity demand. Since wider yield spreads typically lead to strong future economic growth, it is unsurprising they are also generally associated with strong equity returns. As Exhibit 4 shows, widening yield spreads are generally associated with both a higher frequency of positive stock returns and higher average stock returns.

Exhibit 4: Forward Equity Returns Improve with Wider Yield Spreads

Source: Global Financial Data, as of 9/30/2013. Data is monthly since 1950, to roughly coincide with the 1951 Federal Reserve Treasury Accord, which re-established the Federal Reserve’s independence and reduced the Treasury’s influence over interest rates.

The future is always uncertain, and a major event or policy mistake could derail the current bull market at any time. As my boss, Ken Fisher, puts it, ”If aliens land tomorrow, all bets are off.” Negative possibilities always exist. Investing is about probabilities. And the historical record argues the current widening of yield spreads tied to Fed tapering put the odds heavily in favor of this bull market continuing.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today