Personal Wealth Management / Economics

With Q2 Data Coming Soon, Expect Awful

Analysts have expected dismal Q2 data for months.

Q2 draws to a close today, and with it, perhaps the ugliest quarter in modern US economic history. Since most shelter-in-place orders didn’t take effect until late March, Q2 data will bear the brunt of the national lockdown. Soon earnings season will kick off, showing how the institutional response to the pandemic hurt corporate profits. Then, toward July’s end, the first reading of GDP will display the broad economic damage that narrower monthly indicators, especially April’s, have hinted at for months. In our view, this makes now an excellent time to remember that when these numbers come out, they will be old news to stocks—not a new shock or catalyst for lasting market weakness.

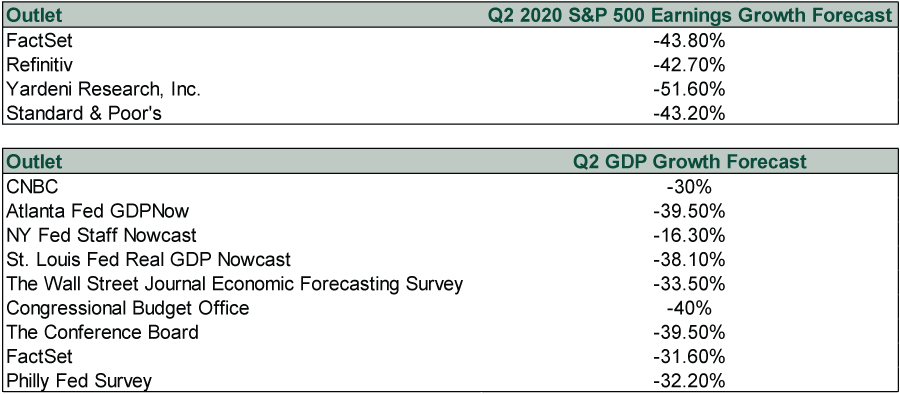

Exhibit 1 rounds up several headline-making earnings and GDP forecasts. As you will see, they range from ugly to awful.

Exhibit 1: Major Q2 Earnings and GDP Forecasts

Source: Outlets listed above, as of 6/26/2020. Forecasts cited are the latest available at time of writing. Earnings forecasts are for the year-over-year growth rate. GDP forecasts are for the seasonally adjusted annualized growth rate. That is essentially the rate the economy would decline at if contraction persisted at Q2’s pace for four quarters.

The oldest of these forecasts—the CBO’s—dates to April. The Philly Fed’s was released in May. The rest are from June, but that doesn’t make them brand-spanking new. The St. Louis, New York and Atlanta Fed update their GDP nowcasts weekly, so these bad numbers have been circulating for a while. (While these don’t constitute official Fed branch forecasts, they are widely watched by pundits and analysts.) Ditto for FactSet and Refinitiv’s earnings forecasts, which are also released and updated regularly. So investors have known for months that the results will be very bad indeed.

Yet stocks are recovering. Bad forecasts haven’t derailed the rebound, and we doubt the actual releases will either. Stocks are forward-looking. They discounted the high likelihood of awful earnings results as they plunged into bear market territory in record time in February and March. Anticipation of a terrible reality fueled the bear. Then, in our view, anticipation of an economic recovery as signs of reopening emerged in early spring helped foment a market rebound. Monthly data are already starting to show those green shoots, but it will be months before they register in GDP and earnings.

So when the actual numbers come out and look awful, don’t let the inevitable handwringing get to you. Remember that any apparent disaster is no surprise to markets, which are already looking further into the future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today