Personal Wealth Management / Market Analysis

On the Bond Bounce

Stocks aren’t the only rallying asset class.

As stocks rallied from June’s low, slowing inflation, modestly improving global economic forecasts and better-than-expected European energy supply captured most attention from commentators we follow.[i] But we also see another force quietly working in the background: the bond market. Not as a driver of the stock market, mind you, but a companion. Our research suggests both fell together on conjoined inflation and rate hike fears last year.[ii] But since autumn, both have flipped and rallied in tandem.[iii] As with stocks, bonds’ low will be clear only in hindsight. But we think the rally thus far looks consistent with the 2023 rebound we expect.

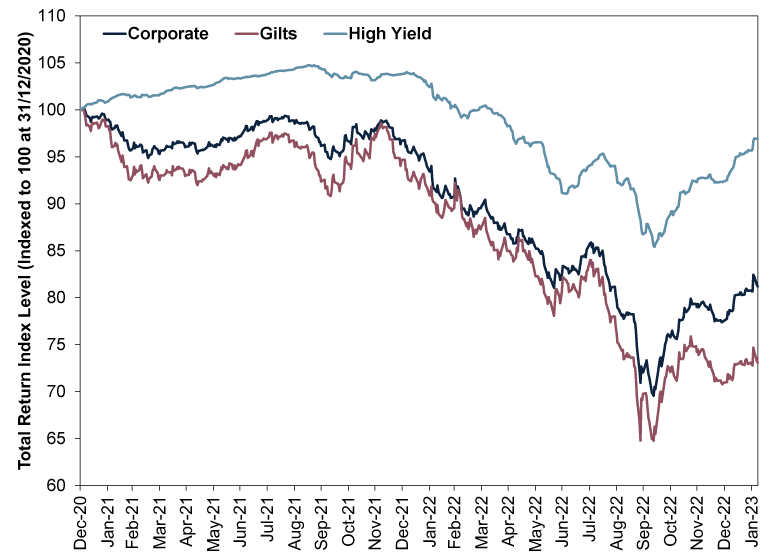

Exhibit 1 shows UK Gilts, investment-grade corporates and high-yield bonds in total return terms (price movement plus yield) since 2020’s end—capturing their full downturn. Gilts and investment-grade corporates endured a full bear market, falling more than -20% from their high.[iv] High yield bonds didn’t breach this threshold, but they came close. However, like stocks, all three have jumped from their respective lows, with corporates and high yield leading.

Exhibit 1: Bonds Are Bouncing, Too

Source: FactSet, as of 8/2/2023. ICE BofA Sterling Corporate, UK Gilt and Sterling High Yield total return indexes in GBP, 31/12/2020 – 7/2/2023.

Bond prices and interest rates move in opposite directions, so it is probably no surprise that as long-term interest rates fell from their autumn high, bonds rallied.[v] That is bond market mechanics 101. We don’t find corporates’ and high yields’ outperformance shocking, either. Whilst government rates exert strong influence over these categories, they also have higher perceived risk than Gilts tied to corporate financial health. So in our view, it is rather normal for them to fall more on the way down—and we have long held that what falls the most in a downturn usually bounces higher in a recovery.

To understand this, we find it helps to think more in terms of interest rates than price. Because corporate and high-yield bonds have higher default risk, we find they generally pay higher yields than Gilts do. When economic times get tough—or are feared to get tough—perceived default risk rises relative to Gilts, so their interest rates typically rise more than Gilt rates do, in our experience. Or, to use industry jargon, their credit spreads versus comparable maturity Gilts widen. When economic conditions improve, corporate and high-yield rates will typically fall more as their perceived risk improves to a greater degree, so credit spreads narrow and corporates and high yield outperform. Long-term securities, which tend to be more interest-rate sensitive than short-term bonds, also tend to do better.[vi]

This upturn isn’t so surprising, in our view. We find longer-term Gilt yields move primarily on inflation expectations, which have come down quite a bit as inflation has eased.[vii] That means investors need less interest to compensate for inflation over the bond’s maturity. As concerns around UK inflation continue easing this year, Gilt yields may keep falling—and bond prices keep rising—although we think the pace is likely to cool as inflation improvements become more widely appreciated.

In our experience, bonds’ downturn was one of 2022’s biggest frustrations for investors. Those owning a mix of stocks and bonds generally own the latter to reduce expected short-term volatility relative to an all-stock allocation. UK bonds still generally accomplished that, moving less than stocks during volatile stretches with the possible exception of Gilts during the political kerfuffle over former Prime Minister Liz Truss’s mini-budget.[viii] But that was still the coldest of comfort for many, given the overall decline. Yet over more meaningful timeframes, we find downturns don’t negate bonds’ purpose in portfolios or their ability to contribute to and help smooth overall returns. We think most would agree that periods like 2022 aren’t pleasant. And we can’t say with certainty the downturn is over. But there have been notable improvements in the bond market since last year, and we think that is worth noting.

[i] Source: FactSet and the UK Office for National Statistics, as of 9/2/2023. Statement based on MSCI World Index price level in GBP, 16/6/2022 – 9/2/2023 and UK consumer price inflation, October 2022 – December 2022. Inflation refers to broadly rising prices across the economy.

[ii] Ibid. Statement based on MSCI World Index returns with net dividends in GBP and ICE BofA Sterling Corporate, UK Gilt and Sterling High Yield index returns in GBP, 31/12/2021 – 30/12/2022.

[iii] Ibid. Statement based on MSCI World Index returns with net dividends in GBP and ICE BofA Sterling Corporate, UK Gilt and Sterling High Yield index returns in GBP, 1/9/2022 – 7/2/2023.

[iv] Ibid. Statement based on ICE BofA Sterling Corporate, UK Gilt and Sterling High Yield index returns in GBP, 30/12/2021 – 7/2/2023. A bear market is a prolonged, fundamentally driven broad equity market decline of -20% or worse.

[v] Source: FactSet, as of 9/2/2023. Statement based on 10-year UK Gilt yield, 26/9/2022 – 9/2/2023.

[vi] Source: FactSet, as of 15/2/2023. Statement based on duration, a measure of interest rate sensitivity hinging on time to maturity and yield.

[vii] Source: UK Office for National Statistics, as of 9/2/2023. UK consumer price inflation, October 2022 – December 2022.

[viii] Source: FactSet, as of 15/2/2023. Statement based on median daily percentage change in MSCI World Index returns with net dividends in GBP and ICE BofA Sterling Corporate, UK Gilt and Sterling High Yield index returns in GBP, 31/12/2021 – 30/12/2022, 29/3/2022 – 16/6/2022 and 19/8/2022 – 14/10/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis A Market Perspective on Iran Truce Talks2026-06-17

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-17

-

Macro Insights Japanese Equity Outperformance & Why It's Poised to Continue2026-06-15

-

Macro Insights Assessing Private Credit Risks and Exposures2026-06-09

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today