Personal Wealth Management / Economics

Defusing Deglobalization Fears

The death of world trade is greatly exaggerated.

Are the world’s trade ties and supply chains set to unwind? For much of the past five years, “deglobalization” fears have murmured in the background as tariffs and trade restrictions stole headlines. In 2022, Russia’s invasion of Ukraine spurred sanctions and tough new US controls on advanced technology exports to China—fanning those fears further. Now many worry regional fragmentation could send world trade into reverse. But data suggest the fears are disconnected from reality—the evidence says world trade is in fine fettle.

Much of the concern here stems from the increased geopolitical chatter of late, which has taken on more of an economic bent in recent years. While the world has grown more and more interconnected over the decades—with companies investing and operating to take advantage—in the last five years we have increasingly seen political reactions to it. For one, politicians have talked up tariffs and protectionism globally since at least 2016’s presidential election—if not even earlier, involving things like Chinese steel and solar panels. But all this has garnered even more attention lately, given Russia’s invasion of Ukraine and increased trade tensions with China. The West’s response to the former was sanctions. The latter has brought forth a slew of tech export restrictions and responses from China. Many see this as the globalized world splintering, which could put supply chains at risk and threaten growth opportunities many businesses have targeted. In a worst-case scenario, a trade war could develop on par with the 1930s, which contributed to deepening the Great Depression.

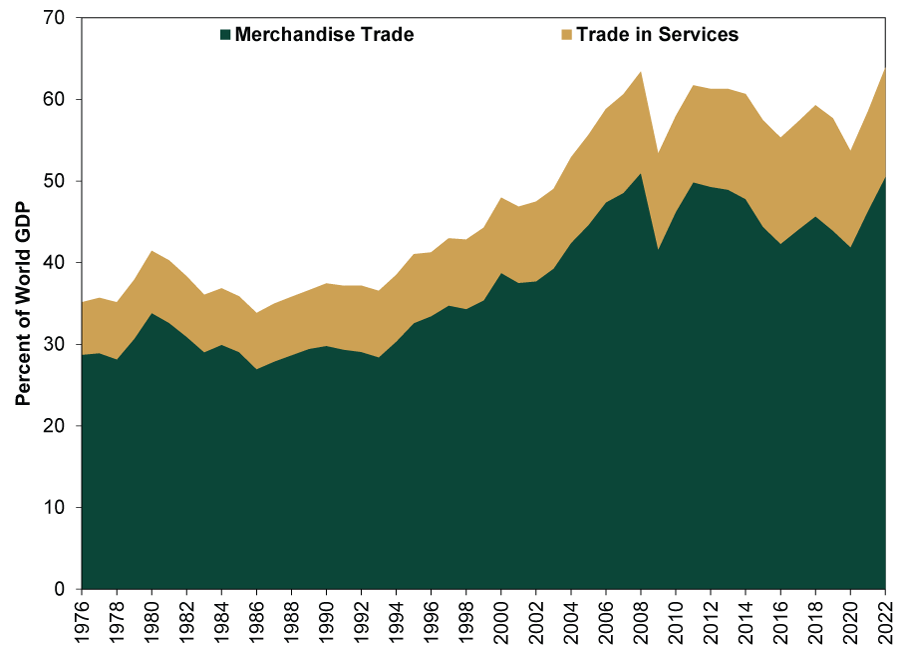

But the data don’t support the fear. Exhibit 1 shows the era of expanding globalization from the 1990s through the mid-2000s seemingly stalled after 2008. While international trade’s share of world GDP has mostly been range bound since, it remains historically high—it hasn’t reversed. Merchandise trade is at 50% of world GDP, just below 2008’s 51% record. Services trade—gaining share since 2008—is at 13%, just below 2019’s 14% prepandemic record. Together, they hit 64% of global GDP in 2022, eclipsing 2008’s previous highwater mark of 63%.

Exhibit 1: Merchandise and Services Trade Share of World GDP at Record High in 2022

Source: World Bank, as of 1/26/2024.

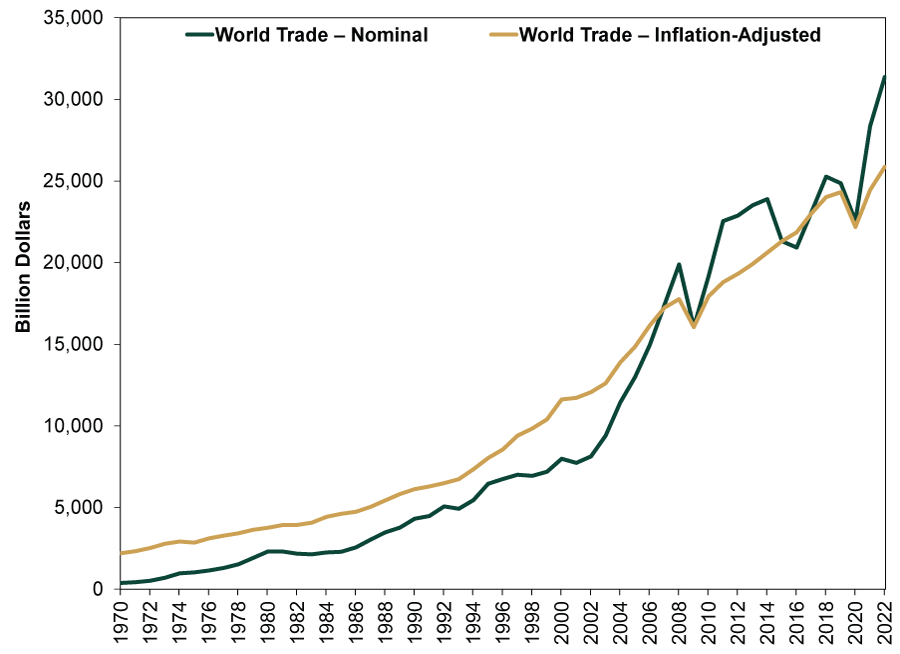

Exhibit 2 shows this another way. Although world trade has seemingly plateaued as a percentage of global GDP in recent years, its total value has climbed—in both nominal and inflation-adjusted terms. We think it is helpful to look at both measures. Nominal dollar trade values (green line) reflect people’s everyday experience: the price tag of what we—or countries—exchange. While inflation has skewed this upward the last few years, sometimes it skews downward, like in 2014 – 2015 when oil prices collapsed. Inflation-adjusted trade (yellow line), though, shows a long-term rise up and to the right, with dips occasionally tied to the cyclical effects of recession—not something structural reflecting deglobalization.

Exhibit 2: Value and Volume of World Trade Continues Rising

Source: World Bank, as of 1/26/2024.

Why haven’t tariffs, sanctions and export restrictions hammered trade? Consider Russia, where Western sanctions have proven ineffective. Although they mostly halted direct Russian energy sales to the West, that just led to China and India importing record amounts, leaving more room for Europe to buy from the Middle East and Americas. Furthermore, India then refined much of that oil and sold it to other nations—including those in the West. Sanctions diverted trade. They didn’t delete it.

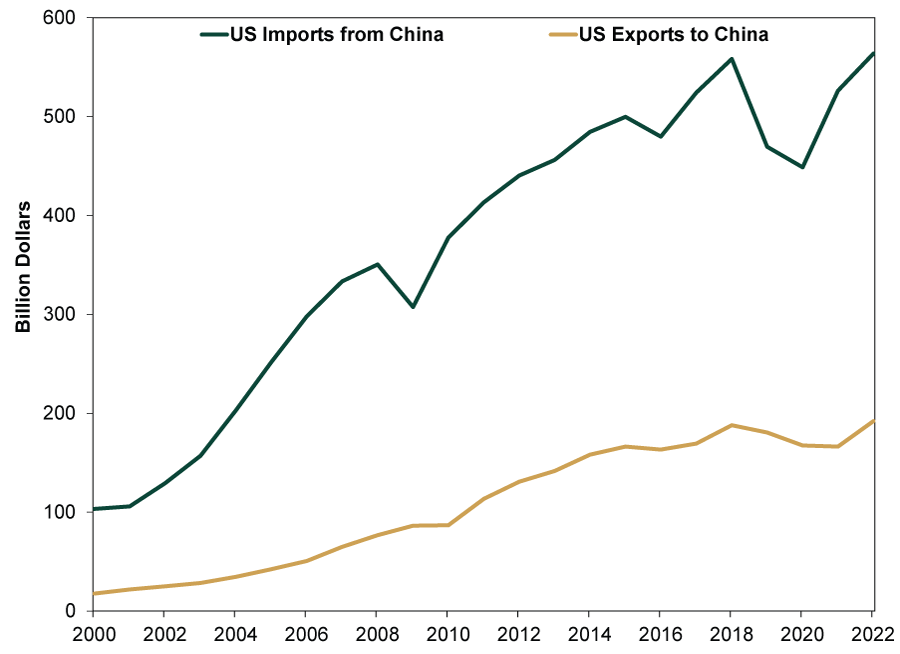

The same held with tariffs on China. US-China trade stands at record highs. (Exhibit 3) And this bilateral snapshot doesn’t account for “transshipping,” reexporting from third-party countries to dodge barriers to trade. Shipments from Vietnam, for example, more than doubled since 2018—when the US-China tariff tiff allegedly began raging—to $128 billion in 2022, vaulting US imports from the country to the seventh largest (just behind South Korea).[i] Now, it is impossible to say how much of that is transshipments. But one study notes, “Vietnam captured more than 60 percent of China’s loss in textiles and apparel and electric equipment exports to the United States” during the so-called trade war.[ii]

Exhibit 3: US Goods and Services Trade With China Still Rising

Source: US Bureau of Economic Analysis (BEA), as of 1/26/2024.

Meanwhile, it seems where US-China trade may be slacking, India and Mexico are picking it up. US imports from India have surged 41% from 2018 to 2022, hitting almost $119 billion, while Mexico’s is up 33% to just over half a trillion dollars—overtaking the value of America’s Chinese imports in Q4 2022.[iii] The latter is often dubbed “nearshoring,” with some citing it as evidence globalization is unravelling. But helping drive burgeoning US-Mexican trade? China, which is investing heavily in Mexico.

According to the Dallas Fed: “China FDI [foreign direct investment] flows into Mexico grew on a nominal basis from $38 million in 2011 to $386 million in 2021 before slipping last year to $282 million—still well above its historical average. While China represents only about 1 percent of Mexico’s FDI, the country has significantly expanded its investments and is the fastest-growing source of foreign investment in Mexico. This FDI investment is mostly directed toward manufacturing plants and regions that export to the U.S.”[iv] More recently, China’s FDI into Mexico looks set to hit billions, as Chinese auto suppliers, battery makers and solar panel producers locate and expand operations there, too.[v]

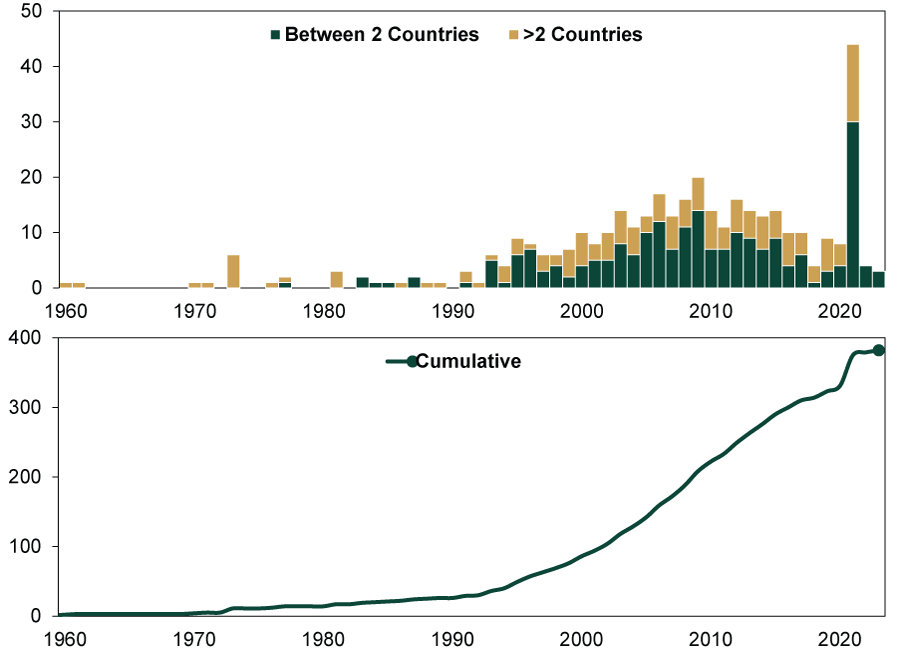

Another aspect of deglobalization supposedly fracturing the multilateral system along geopolitical fault lines: regional trade pacts, which the world has shifted to over the last 30 years. Many worry they will upend the World Trade Organization’s global rules. Exhibit 4 shows regional trade agreements’ proliferation in recent years. (Note: 2021’s spike is mostly the UK replacing its trade deals through the EU with bilateral ones after it left the trade bloc.) But this doesn’t point to a wholesale abandonment of the multilateral system. WTO non-discriminatory rules still serve as the baseline for most of these trade pacts. While some do include rules of origin requirements—which are protectionist—this is far from a new trend or something that would undermine globalization broadly.

Exhibit 4: Number of New Regional Trade Agreements in Force

Source: World Trade Organization – Regional Trade Agreements Database, as of 1/26/2024. Number of Regional Trade Agreements currently in force.

Of course, not all trade pacts are created equal. Take the 11-country Comprehensive and Progressive Agreement for Trans-Pacific Partnership, which seeks to lower trade barriers among its signatories—and the UK is set to join—versus Asia’s 15-member Regional Comprehensive Economic Partnership. The latter largely aims to codify China’s rules as the basis—which could raise barriers.

For investors, trade data usually publish very late, given data collection complexity—especially on the services side. The latest World Bank data, which Exhibits 1 and 2 feature, are from 2022. Exhibit 3 uses the US’s most recent “Trade in Goods and Services” report released January 9—for November. For a sense of global commerce in 2023, though, we can look at the Netherlands’ CPB World Trade Monitor, which measures world merchandise trade volumes—but not services. Its latest reading is also through November.

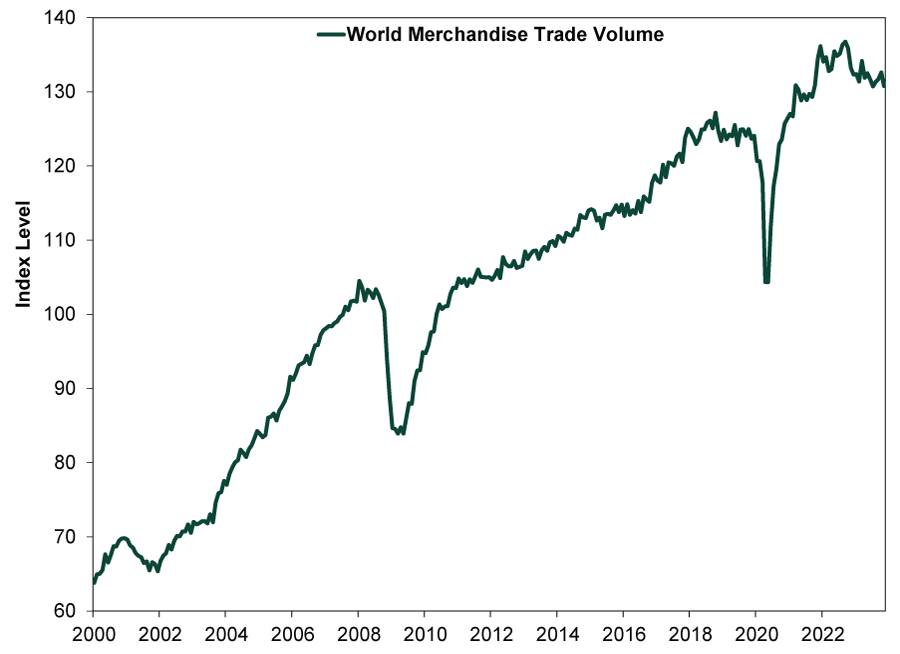

As Exhibit 5 shows, merchandise trade volumes are down from 2022, likely consistent with weak manufacturing and goods consumption over the last year. Regardless, though, it is generally holding steady well above prepandemic levels. There is little here that suggests world trade relationships are meaningfully disrupted.

Exhibit 5: Trade Holding Steady Above Prepandemic Levels

Source: CPB Netherlands Bureau of Economic Policy Analysis, as of 1/26/2024.

Furthermore, much of the deglobalization discussion is long-term in nature—not within the cyclical, 3 – 30-month outlook stocks focus on most. If there were some regionalization or shift away from world trade, it would likely occur at a glacial pace and fade into the background. To influence stocks, trade developments would likely have to be more sudden, akin to 1930’s Smoot-Hawley, which abruptly raised tariffs to high levels on most American trade partners—and engendered a similar response from them. That tanked trade and hampered corporate profits. Despite gloomy sentiment toward trade today, we see little real sign of that.

[i] “US International Trade in Goods and Services, November 2023,” Staff, BEA, 1/9/2024.

[ii] “The US–China Trade War: Vietnam Emerges as the Greatest Winner,” Euihyun Kwon, Journal of Indo-Pacific Affairs, July – August 2022.

[iii] See note i.

[iv] “Mexico Awaits ‘Nearshoring’ Shift as China Boosts Its Direct Investment,” Luis Torres and Aparna Jayashankar, Federal Reserve Bank of Dallas, 4/14/2023.

[v] “Mexico’s Nuevo Leon State Says China’s Trina Solar to Invest up to $1 Bln,” Staff, Reuters, 10/16/2023. “Chinese Firms to Invest Nearly $1 Bln in Northern Mexico -State Officials,” Staff, Reuters, 10/25/2023. “China to Set up Shop in Mexico, and the US Isn’t Happy,” Jennifer Mossalgue, Electrek, 12/20/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today