Personal Wealth Management / Market Analysis

The Relationship Between Rates and Stocks Isn’t as Straightforward as Many Think

Long-term interest rates—whether rising or falling—don’t have a reliable impact on stock market direction.

In a week with monetary policy meetings scheduled in Norway, Switzerland, Sweden, Japan, the UK—oh, and the US—it was perhaps inevitable interest rates would feature prominently in financial commentary. Then, on Monday, the US 10-year Treasury yield hit 3.489%, its highest close since April 2011, triggering even more headlines. Many presume the rise in long-term yields is poison for stocks, and fear of rising rates seemingly has played a role in this year’s market decline. We don’t dismiss how challenging this market environment has been, as interest rate concerns have been one of at least eight stories weighing on sentiment over the past nine months. Yet in our view, it is an error to extrapolate forward this effect—chiefly a sentiment function—and presume rates simply must fall for a new bull market to begin.

Arguments positing the upturn in long rates undercuts stocks generally go like this: Low yields in the not-so-distant past presumably buoyed stocks. Proponents of this take said, “there is no alternative” (aka, TINA) to stocks providing a reasonable return. So, they argue, low rates lured more people out of bonds and into stocks. Still others carry this a bit further into theoretical territory, noting that, because rising interest rates reduce the current value of future revenues and profits, higher yields now weigh on stocks’ appeal.

Today, with most people projecting rates’ rise this year into ever-higher yields to come, many conclude there is more trouble ahead for stocks. There is an alternative now, they say, even if yields at 3.5% are far below inflation and further rises in yields would hit bond prices (which move inversely to yields).

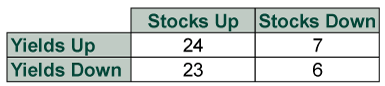

Yes, yields are up, and that has coincided with sliding stocks this year. But be careful about assuming this past is prelude. For one, the idea rates must fall for stocks to rise is at odds with historical data. Since 1962, the S&P 500 has a correlation of -0.05 to weekly changes in 10-year Treasury yields.[i] Considering 1.00 means identical movement and -1.00 exact opposite, that shows you there is next to no reliable relationship. Rates and stocks rise and fall concurrently quite often through history—about as often as they don’t. Exhibit 1 shows this another way, tallying the count of years that yields and stocks rose together, diverged and fell together. As you can see, there isn’t much of an identifiable relationship here—nothing to hang your hat on.

Exhibit 1: 10-Year Yields and Stocks—No Set Relationship

Source: Global Financial Data, Inc. and FactSet, as of 9/19/2022. Annual change in 10-year Constant-Maturity Treasury Yield and S&P 500 total return, 1962 – 2021.

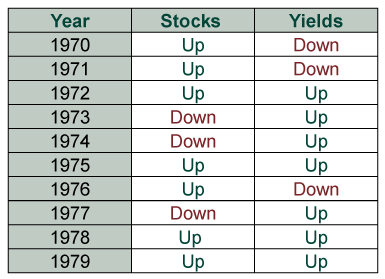

Even during the hotly inflationary 1970s, this lack of relationship exists. (Exhibit 2) The idea we must see rates fall for a recovery seems questionable.

Exhibit 2: Rates and Stocks in the 1970s by Year

Source: Global Financial Data, Inc. and FactSet, as of 9/19/2022. Annual change in 10-year Constant-Maturity Treasury Yield and S&P 500 total return, 1970 – 1979.

Why is this relationship so flimsy? We suspect it is because rates are just one of many things influencing stocks—a key blindspot for theories about rates reducing future profits’ and revenues’ values. That argument may or may not hold if all else is equal, but all else almost never is, undercutting the theory.

As for TINA, we have different quibbles. For one, the correlation between stocks and bond yields during the 2009 – 2020 bull market was positive 0.40.[ii] That means they moved together more often than not over this span. Beyond that, if there was a huge exodus from bonds to stocks when rates fell over the course of the 2009 – 2020 bull market, we should see this in fund flow data. A reversal should also feature prominently in more recent data. Neither holds. During the 2009 – 2020 bull market, net flows into bond mutual funds and exchange-traded funds (ETFs) dwarfed net flows into stock funds and ETFs.[iii] This year, while yields have climbed—theoretically giving investors a viable alternative to stocks—bond fund outflows have topped stocks. Fund flows are, of course, not a complete look at what investors are buying or selling. But we would expect to find some sign of TINA here if that theory were true. There isn’t.

Furthermore, there really isn’t anything that says rates must keep rising from here. While many point to that plethora of central banks hiking rates, they mostly move short rates, not long. (Quantitative Tightening, the Fed’s allowing bonds purchased under its past “stimulus” efforts to mature without reinvesting the proceeds, does, but it is largely a known quantity and markets likely reflect its influence to a great extent already.) Counterintuitively, rate hikes can drag down investors’ inflation expectations, which is a force potentially lowering interest rates. Inflation expectations have already begun cooling, which could spell lower long rates before long. But even if they don’t, we think it is a mistake to presume long rates climbing from here assures more downside for stocks.

[i] Source: FactSet, as of 9/19/2022. Weekly correlation coefficient between the S&P 500 index’s price returns and the change in 10-year Constant-Maturity Treasury yields, 1/5/1962 – 9/16/2022. Date range used is the full history of 10-year Constant-Maturity yield data.

[ii] Ibid. 3/6/2009 – 2/19/2020.

[iii] Source: FactSet, as of 9/19/2022. Cumulative ICI mutual fund and ETF flows, March 2009 – January 2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today